Insights

Q1 2026 Market Commentary: Investing Through Crosscurrents

by Sequoia Financial Group

by Sequoia Financial Group

The first quarter of the year has offered an early reminder that markets rarely move in straight lines. After the extraordinary enthusiasm that carried investors through 2025, much of it centered on the promise of artificial intelligence, the new year has quickly reintroduced elements of uncertainty. The pace of AI adoption has left many wondering not just how transformative the technology may be, but also how disruptive its ripple effects might prove across industries and, perhaps, the labor market.

Meanwhile, private credit, one of the brightest stars of recent years, has begun to attract more critical attention. Rapid growth and abundant capital have a way of dulling discipline, and emerging signs of weaker underwriting are forcing investors to reassess both risk and reward in the space.

Then came a new geopolitical shock. The outbreak of hostilities in Iran shifted markets from rotation to retreat, igniting a sharp rise in oil prices and rekindling inflation concerns that had only recently subsided. The result has been a more cautious tone—one in which interest rates and energy prices have resumed their outsized influence over sentiment, and investors have adopted a distinctly risk-averse posture while waiting for the uncertainty to clear. Oil has spiked, reflecting one of the largest supply shocks on record; long-term U.S. Treasury rates are now flirting with 4.5% amid the inflationary impulse of war; and equities have sold off in a natural reaction to the uncertain economic backdrop.

Looking ahead, the environment seems likely to remain unsettled until there’s a clearer sense of both the geopolitical and macroeconomic paths. Elevated energy prices and the accompanying drift higher in interest rates may continue to test the resilience of markets and valuations that, by many measures, still assume a relatively benign backdrop. At the same time, innovation—including the undeniable momentum behind AI—continues to unlock productivity potential and new business models that could redefine the cycle’s contours.

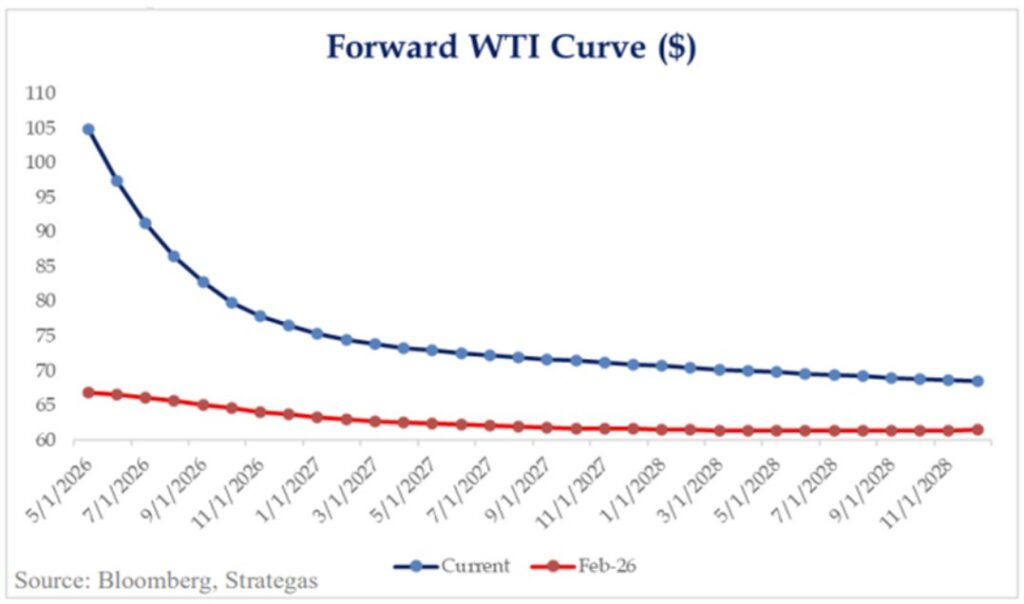

Oil and gas prices have surged as supply routes through the Strait of Hormuz remain constrained, and those shocks are understandably casting a shadow over the outlook for global growth. How much damage is ultimately done will depend less on the initial spike than on its duration—a variable that, for now, remains unknowable. What we can observe is that while the expected price level of oil has moved higher in the near-term, the market is still discounting a meaningful decline as the year progresses. If that path holds, the episode may come to be seen as a sharp but temporary shock rather than the trigger for a global recession.

The forward curves tell a similar story for corporate input costs, particularly in energy‑intensive sectors such as transportation. The West Texas Intermediate (WTI) curve for 2027 and 2028 has shifted higher by roughly $10, implying a more expensive backdrop than investors expected just a short time ago. Even so, those levels remain within a range that the U.S. economy has historically been able to absorb; growth has persisted in past cycles with oil prices well above $70. The more immediate challenge is not the absolute level, but the speed of the move—businesses and markets adjust better to gradual change than to sudden repricing.

The challenge for investors lies in balancing those crosscurrents: recognizing the durability of long-term trends without being swept away by near-term enthusiasm or fear. Our focus, therefore, remains on fundamentals: underwriting that withstands stress, businesses with enduring advantages, and portfolios built to outlast headlines rather than chase them. In times like these, patience and selectivity aren’t just virtues; they’re competitive advantages.

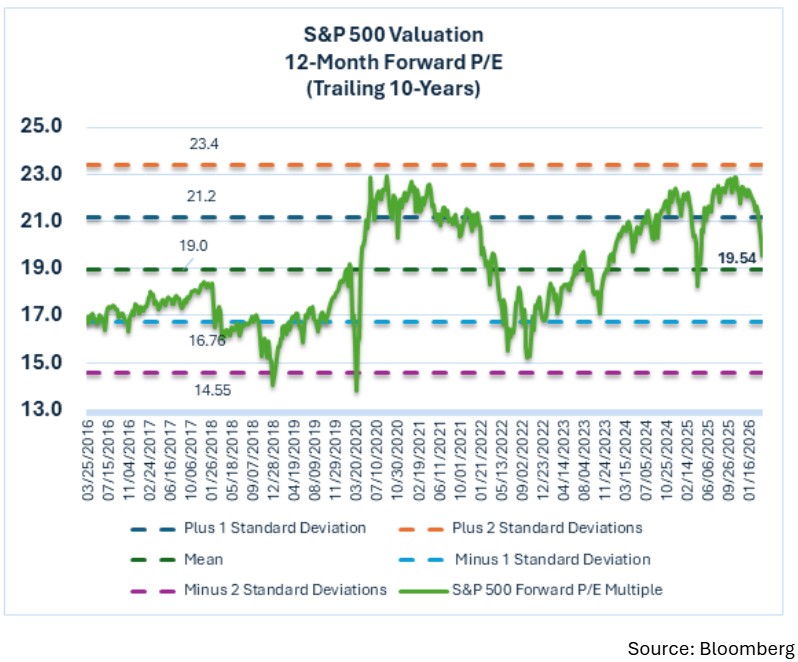

The S&P 500 has retreated about 9% from its January highs, marking a healthy recalibration rather than a collapse. As rising oil prices, interest rates, and geopolitical uncertainty weighed on sentiment, valuations have compressed meaningfully, with the market’s P/E multiple sliding from 22x to 19x in just a month. Yet beneath the surface, fundamentals continue to improve with analysts raising 2026 earnings forecasts by roughly 3%. In other words, while prices have adjusted lower, expected profits have inched higher, narrowing the gap between perception and reality and potentially setting up a more attractive entry point for disciplined investors.

Earnings: The Quiet Strength Beneath the Surface

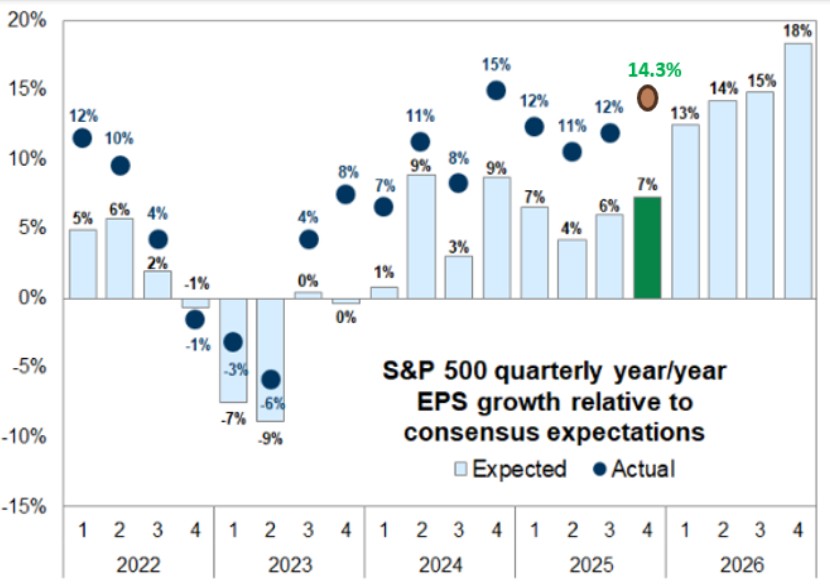

Let’s pause to recognize the continued strength of corporate earnings, the bedrock upon which equity markets ultimately rest. Despite recent market volatility, earnings expectations have improved. Once again, corporate America has delivered. Fourth-quarter results showed earnings growth of roughly 14% year over year, doubling the consensus forecasts that preceded the reporting season.

This strength isn’t the result of accounting wizardry or one-off factors. It reflects genuine improvement in both sales and margins, with margins now at record highs. To borrow an old saying, companies are not just growing—they’re growing more profitably.

Perhaps most importantly, forward earnings estimates continue to grind higher, offering a durable fundamental anchor for equity valuations at a time when sentiment remains uncertain. Markets may rise and fall for any number of reasons in the short run, but over time they tend to gravitate toward intrinsic value—and right now, that intrinsic value is being quietly reinforced by strong corporate performance.

The Broadening Thesis, Interrupted

Earnings have come in better than expected, and forward estimates have inched higher, even as the markets have grown more unsettled. Yet many of those forecasts were made for a very different world, before oil pushed through $100, before the risk of rekindled inflation returned to the front burner, and before investors began to doubt that interest rates were on a one-way path lower. None of this makes an earnings collapse the most likely outcome. It does, however, suggest that the margin of safety in today’s valuations is slimmer than it appears, particularly in corners of the market where multiples still assume a benign, cooperative macro backdrop.

That brings us to what may be the key structural question for investors today. The rotation story was never simply an anti-“Magnificent Seven” trade. It was rooted in a broader idea: that the opportunity set for growth was widening—away from a narrow group of U.S. mega-cap technology companies and toward geographies, sectors, and market caps that had been left behind during years of concentrated leadership. The outbreak of war did not overturn the valuation case; it merely interrupted the process, as capital flowed back to what felt safest and most familiar.

The conflict dealt a blow to the narrative of synchronized global growth, especially for economies more directly exposed to energy shocks and with less policy flexibility than the United States, and pulled investors back toward the U.S. large-cap complex. In periods of genuine uncertainty, investors have a long history of favoring liquidity, scale, and perceived safety—all attributes that U.S. large-cap technology companies possess in ample supply. That instinct is understandable; though, it is not likely to be permanent. When the fog eventually lifts, there is good reason to think the case for a broader rotation will reemerge rather than vanish.

The chart above shows that market performance has already become meaningfully less concentrated than in recent years, and even somewhat less concentrated than the average of the last three decades. For that process to resume with conviction, however, a few things probably have to go right: some meaningful easing of tensions in the Middle East that allows energy prices to retreat; a labor market that steadies instead of deteriorating; a Federal Reserve that can credibly sketch a path toward eventual easing; and earnings reports that prove the rest of the market can grow on its own merits, without depending on the brief, almost perfect alignment of macro tailwinds seen in January.

Immigration, Labor, and the Shifting Foundations of Growth

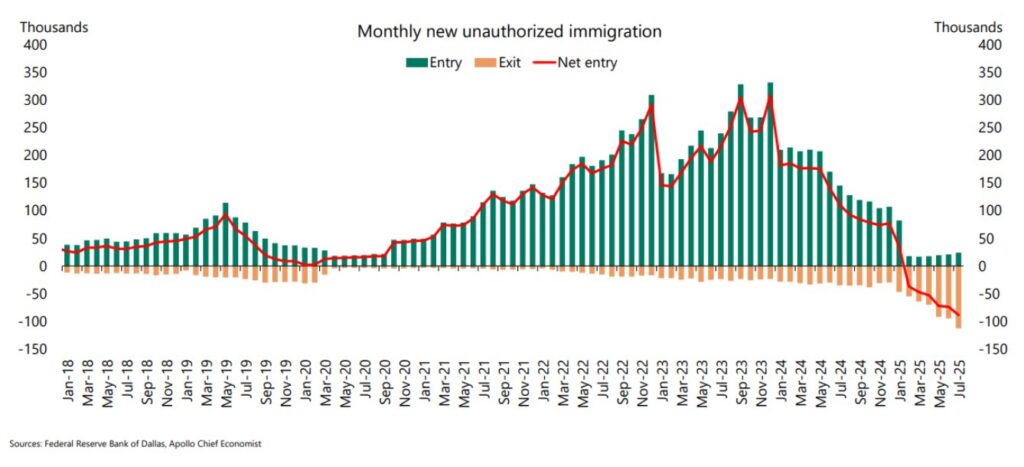

Over the past several decades, immigration has played a quiet but powerful role in shaping U.S. economic growth. It’s often portrayed as a social or political issue, but for investors and business leaders, it’s first and foremost an economic one. When population growth slows—or worse, turns negative—the effects ripple across nearly every corner of the economy.

The most visible and immediate consequence of net negative immigration is its impact on labor supply. A smaller inflow of working-age individuals constrains the pool of available labor, particularly in sectors that rely on steady streams of new workers—construction, healthcare, logistics, and hospitality among them. Over time, that shortage exerts upward pressure on wages, compresses margins for labor-intensive businesses, and can limit the pace of expansion in the broader economy. In short, when labor force growth stalls, productivity and output often follow suit.

The effects extend beyond the workplace. Housing, especially multi-family housing, is another area where immigration has been a key demand driver. Fewer new entrants mean slower household formation, weaker rent growth, and potentially excess supply in markets that built aggressively over the past decade to meet previous population trends. For developers, landlords, and REIT investors, this shift bears close watching. What once looked like a structural shortage could, in some regions, tilt toward surplus more quickly than expected.

None of this is to say the U.S. economy is destined for stagnation; there are always countervailing forces, from technological innovation to rising productivity. But it’s worth remembering that growth ultimately rests on two ingredients: how many people are working and how much each produces. A reversal in one of those variables alters the long-term equation in ways that may not be easily offset.

As investors, we often focus on cyclical drivers, such as the Fed, inflation, and valuations. Yet structural shifts, such as demographics and immigration, hold equal power in shaping the trajectory of opportunity. They deserve a place in our thinking, not because they move markets tomorrow, but because they rewrite the backdrop against which markets evolve.

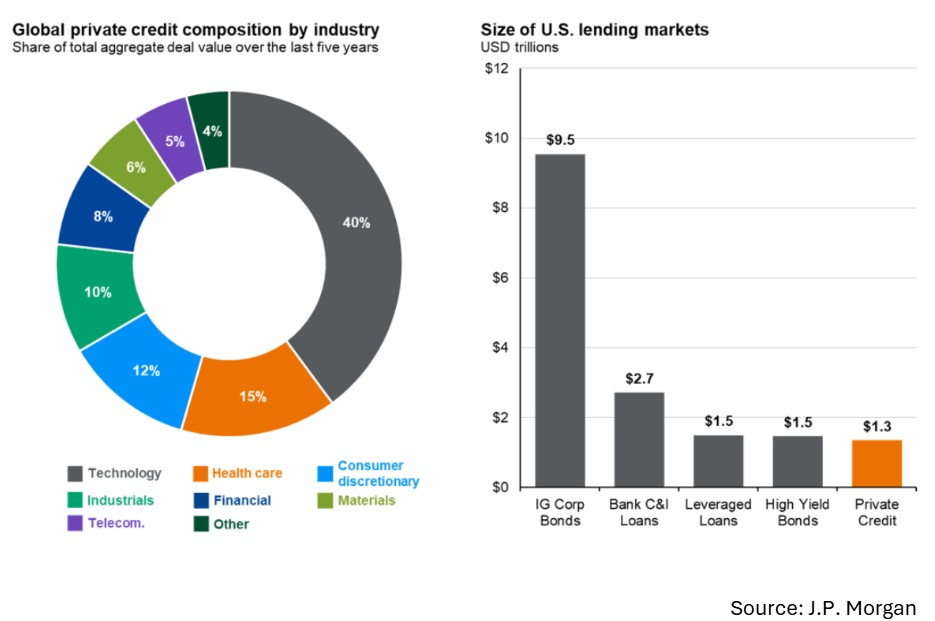

The Rise of Private Credit and the Question of Liquidity

The rise of private credit in recent years stems largely from the post-Global Financial Crisis (GFC) retrenchment of traditional banks, especially in middle market direct lending. As banks pulled back under the weight of new regulations and heightened scrutiny, asset managers stepped into the breach, offering capital to borrowers who once would have gone to their local bank and providing investors with access to corporate credit that doesn’t trade on public markets. In other words, an old activity migrated from one home (the banks) to another (the asset management world).

This shift occurred at a time when floating rate credit looked particularly appealing. Reference rates such as SOFR rose in response to the post-COVID inflation surge, and investors, understandably, were drawn to instruments that promised higher coupons as short-term rates reset. The combination of attractive yields, a compelling story, and an ample distribution apparatus led to explosive growth in private credit, particularly as the product was funneled into the retail wealth channel under the banner of “alternative income.”

As so often happens in our business, strong demand and rapid growth brought side effects. When capital is plentiful and deals are easy to place, underwriting discipline has a way of eroding at the margin. That has left some investors today asking a basic but important question: “What exactly do I own?”

There is a specific wrinkle here. A meaningful slice of private credit was extended to businesses built on subscription or SaaS-like models, underwritten on the assumption of durable revenue and low churn. The rapid advance of AI has led some investors to question the persistence of certain software business models and the durability of the cash flows once thought almost annuity-like.

Beyond credit quality, however, lies an issue that may be more consequential in the near term: liquidity. Much of the recent product was designed to offer “semi-liquid” access for retail investors—periodic subscriptions and redemptions, with the promise of limited, but real, access to cash. The underlying assets, however, remain private loans that cannot be sold in size overnight without affecting price. That’s a classic liquidity mismatch. The structures typically include gates and other tools meant to protect the manager from being forced to liquidate illiquid holdings to meet outflows. These mechanisms are sensible from a portfolio management perspective, but they can come as an unpleasant surprise to investors who thought they were buying something close to daily liquidity.

In our view, this liquidity mismatch is the more pressing concern today. A credit cycle will come—sooner or later it always does—and when it does, some managers will prove to have underwritten more carefully than others. Defaults will rise, recoveries will vary, and dispersion of outcomes across managers and strategies will likely be wide. That is the normal functioning of credit markets, not necessarily a sign of systemic fragility.

Crucially, even assumptions that strike us as quite conservative—for example, a 15% default rate within private credit, with associated losses—do not appear to pose a systemic threat to the broader economy. The sector has grown rapidly and deserves respect and scrutiny, but it is not levered in the same way the banking system was in 2006–07, nor is it as tightly interconnected. The pain, if and when it comes, is more likely to be borne by specific funds and their investors than to require a rescue of the financial architecture.

That doesn’t mean investors should be complacent. It does mean the questions should be framed correctly. The key issues in private credit today center on the quality of underwriting done during the boom, the resilience of the underlying business models (particularly in parts of software), and the degree to which the liquidity features investors expect are consistent with the liquidity of the assets they own. As always in credit, success is less about finding the most exciting opportunity and more about understanding the risks being taken and ensuring you’re being adequately compensated for bearing them.

Geopolitics Abroad, Politics at Home

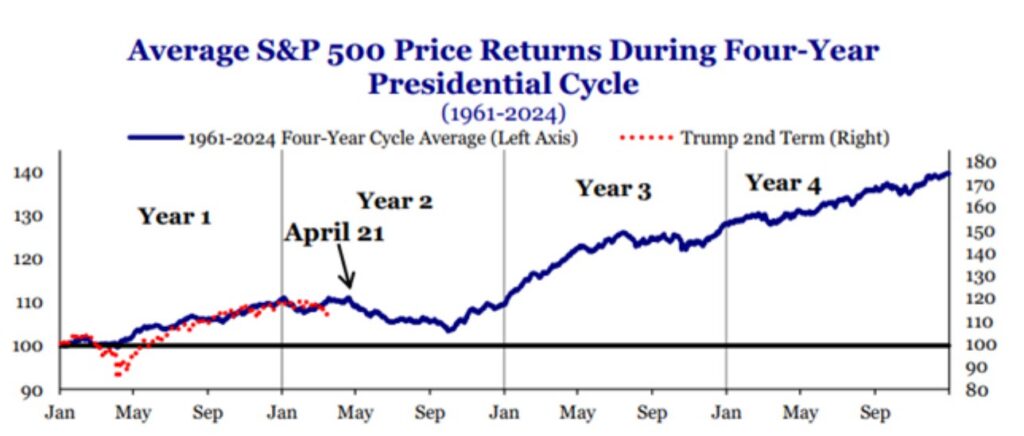

We’re also navigating another familiar but consequential force: the seasonality of domestic politics. History shows that markets often grow uneasy during midterm election years, when policy direction is in question and uncertainty weighs on sentiment. The data, shown in the accompanying chart, illustrate this pattern clearly—periods of strain in the second year of the presidential cycle have been a recurring feature since 1961.

Source: Strategas

The reason isn’t hard to see. Midterm elections often challenge incumbents’ ability to maintain control, creating ambiguity about the policy environment and prompting investors to hesitate. That’s the difficult part. The encouraging piece, however, lies just beyond it: once political visibility improves—when election outcomes clarify the path forward—markets have historically responded with renewed strength. As ever, it’s the transition from uncertainty to understanding that seems to restore confidence.

Conclusion: The Case for Diversification in a World of Crosscurrents

The first quarter has reminded investors that markets are driven by crosscurrents rather than a single, tidy narrative. On one side stands the quiet strength of fundamentals: earnings have surprised to the upside, forward estimates continue to rise, and equity valuations have moved from stretched to more reasonable without any sign of a collapse in profitability. On the other side are the forces that understandably unsettle investors—a major geopolitical shock that has driven oil sharply higher, pushed interest rates back up, and interrupted the broadening of market leadership beyond a narrow group of mega-cap growth companies. When you add in the rapid pace of technological change and uncertainty about how AI will reshape business models and labor markets, it becomes clear that the range of possible outcomes has widened, not narrowed.

At the same time, slower-moving structural shifts are quietly reshaping the backdrop for investors. Changes in immigration and labor dynamics have implications for long-term growth, inflation, and the industries that will thrive or struggle in the years ahead. The rise of private credit offers another example: What began as a rational migration of lending activity from banks to asset managers has, in places, morphed into an arena where underwriting quality and liquidity design deserve close scrutiny. None of this appears likely to trigger a systemic crisis, but it does mean the difference between strong and weak managers and between solid and fragile structures may be more pronounced than in calmer periods.

In such an environment, diversification is not a box to be checked but a principle to be elevated. No one knows which path geopolitics will take, how quickly inflation will recede, or exactly how technological and demographic forces will play out. What investors can control is the robustness of their portfolios: emphasizing businesses with durable earnings power, being highly discriminating against the risks taken in areas like private credit, and resisting the temptation to concentrate exposures in whatever has worked most recently. When the world grows more uncertain, and the old playbook feels less dependable, spreading risk thoughtfully—across asset classes, regions, sectors, and styles—is not a concession; it is a source of strength. In that sense, diversification is more important today than at any point in this cycle.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory