Market Commentary

Stocks Hit New Highs on AI Optimism and Iran Optimism

by Sequoia Financial Group

by Sequoia Financial Group

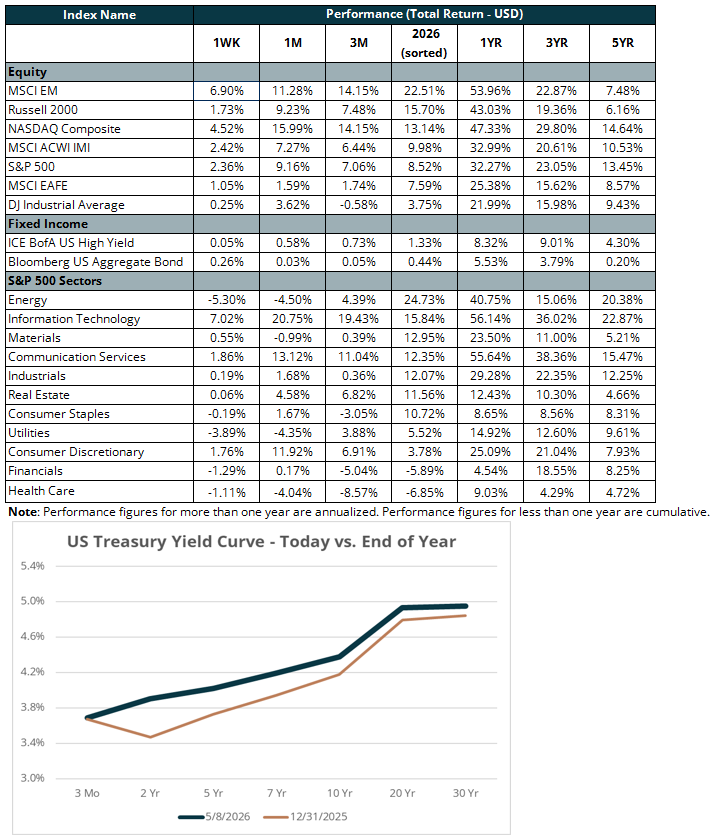

U.S. equities posted strong gains in a week that delivered fresh record highs for two of the three major indices, but also revealed striking dispersion beneath the surface. The tech-heavy NASDAQ jumped roughly 4.5 per cent, the S&P 500 rose over two per cent, and the Dow Jones Industrial Average was in essence unchanged. That gap reflects how heavily the rally was concentrated in semiconductors and other artificial intelligence (AI) beneficiaries. Both the S&P 500 and the NASDAQ closed at new all-time highs on Wednesday and again on Friday.

The week’s headline catalyst was reignited enthusiasm for AI, sparked Wednesday by chipmaker Advanced Micro Devices (ticker: AMD). AMD posted a sizable beat, raised guidance, and roughly doubled its long-term forecast for AI server chip demand. The stock jumped roughly 19 percent and pulled peers Nvidia (NVDA) and Super Micro along with it. Reports through the week reinforced the broader message – Anthropic, the maker of the Claude AI model, agreed to spend $200 billion on Alphabet’s (GOOGL) Google Cloud computing power over the next five years; Akamai signed a $1.8 billion seven-year capacity deal with an unnamed AI lab; and Friday brought news that Intel (INTC) had reached a preliminary chip-manufacturing agreement with Apple (AAPL), sending Intel shares up nearly 14 percent.

The other major driver was apparent diplomatic progress in the Iran war. Stocks fell on Monday as flare-ups in the Strait of Hormuz – the narrow waterway through which roughly 20 percent of the world’s oil flows – sent crude prices up more than four percent and pushed the 30-year Treasury yield briefly above five percent. By Wednesday, optimism around a 14-point U.S.-Iran peace framework reversed those moves: West Texas Intermediate crude finished the week down more than six percent, and Treasury yields ended little changed. Gold rose roughly two percent – a sign that investors continue to hedge against both inflation and geopolitical risk despite the relief in the price of oil.

Two yellow flags warrant attention. First, market breadth (the share of stocks participating in the rally) remains historically narrow; the gap between the S&P 500 and the median stock recently approached its widest in 25 years. Second, the University of Michigan Consumer Sentiment Index dropped to a series low going back to 1952, even as Friday’s April jobs report came in well ahead of expectations.

This week, the focus shifts to Tuesday’s April Consumer Price Index (CPI) report (the Fed’s most-watched inflation gauge) and Thursday’s April Retail Sales report. Earnings highlights include Alibaba (BABA), Cisco (CSCO), and Applied Materials (AMAT). Last week, several Fed officials pushed back firmly on rate-cut expectations, with futures now pricing modest rate hikes through year-end versus none just a week ago.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory