Market Commentary

Earnings Season off to a Strong Start

by Sequoia Financial Group

by Sequoia Financial Group

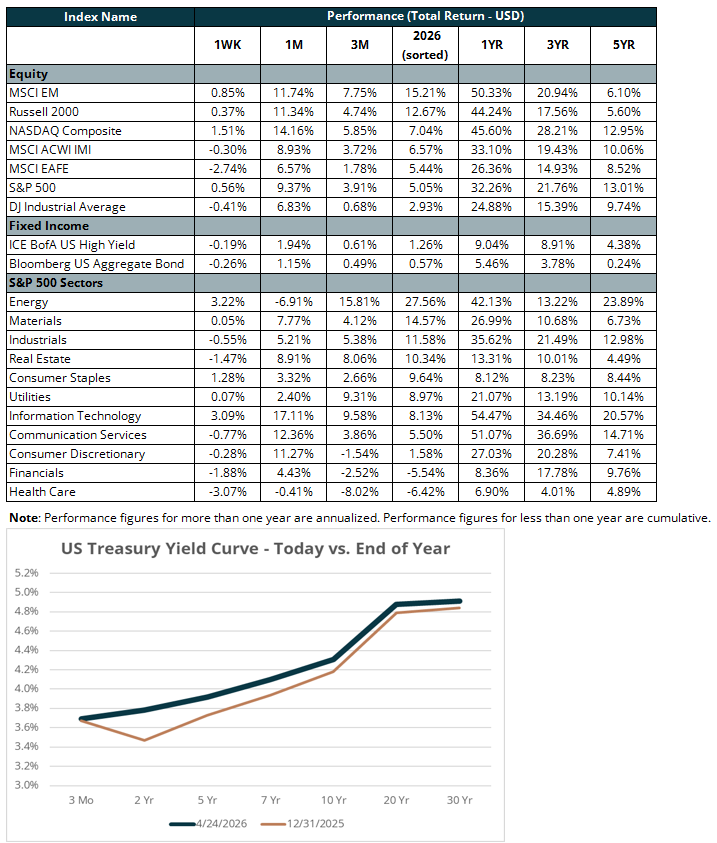

U.S. equity markets posted modest but meaningful gains last week. The S&P 500 rose 0.6 percent and the NASDAQ gained 1.5 percent, and both closed at record highs for the fourth consecutive week. The Dow slipped 0.4 percent on healthcare and financial sector weakness, while the Russell 2000, an index of small company stocks, edged up 0.4 percent for its fifth straight positive week. Market performance was narrow, however, as less than 40 percent of S&P 500 constituents outperformed the overall index.

Fixed income offered little support as the 10-year Treasury yield climbed roughly eight basis points to end near 4.31 percent, dragging the Bloomberg U.S. Aggregate Bond Index down approximately 0.3 percent. Firmer-than-expected economic data reinforced the Fed’s patient stance and kept rate-cut hopes at bay. Gold retreated 2.8 percent as geopolitical urgency around the US-Iran conflict appeared to ease somewhat. Despite the continued ceasefire, WTI crude oil surged 14.3 percent on Strait of Hormuz supply disruption fears, closing the week near $95/barrel.

The dominant market story was an exceptional Q1 earnings season turbocharged by the AI infrastructure theme. The S&P 500’s blended earnings growth rate reached just over 15 percent, with more than 82 percent of companies reporting beating estimates by an average of >12 percent. Semiconductors led the charge: the PHLX Semiconductor Sector (SOX) Index gained 10 percent on the week and notched an unprecedented eighteenth consecutive daily advance. Texas Instruments (ticker: TXN) surged 21 percent on data center and industrial strength with gross margins roughly 200 bps above expectations. Intel (ticker: INTC) jumped 20.5 percent on AI-driven CPU demand and improving computer chip yields. GE Vernova (ticker: GEV) gained 14.6 percent after reporting that Q1 data center electrification deals surpassed the entirety of 2025. The message from corporate America was unambiguous — AI spending is persistent and flowing through to earnings.

Not all sectors participated. Healthcare fell over three percent as pharma and medtech weakness overwhelmed managed care gains. Financials declined 1.9 percent on the week, leaving them roughly 4.5 percent in the red year to date. Software stumbled mid-week after ServiceNow (ticker: NOW) dropped nearly 18 percent on Middle East-driven deal slippage. This was a cautionary reminder that the AI tailwind is not uniformly distributed. The S&P 500’s forward P/E of 21.3x remains above its 10-year average of 19.2x, and large-cap growth is even more extended at 26.7x versus a 24.4x historical norm. The market is priced for continued execution.

The stakes will be raised considerably this week. The April FOMC decision will be announced on Wednesday, but the Committee’s wait-and-see approach could continue. Markets are not fully pricing in a rate cut until September 2027. Amazon, Alphabet, Meta, Microsoft, and Apple will report earnings. Capex guidance from the hyperscalers will face intense scrutiny after Tesla’s surprise $5 billion capex increase this week ignited debate about AI spending discipline. With market breadth narrow and valuations stretched, the bulls need corporate fundamentals to continue delivering.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory