Stocks Continued Their Winning Streak

by Sequoia Financial Group

by Sequoia Financial Group

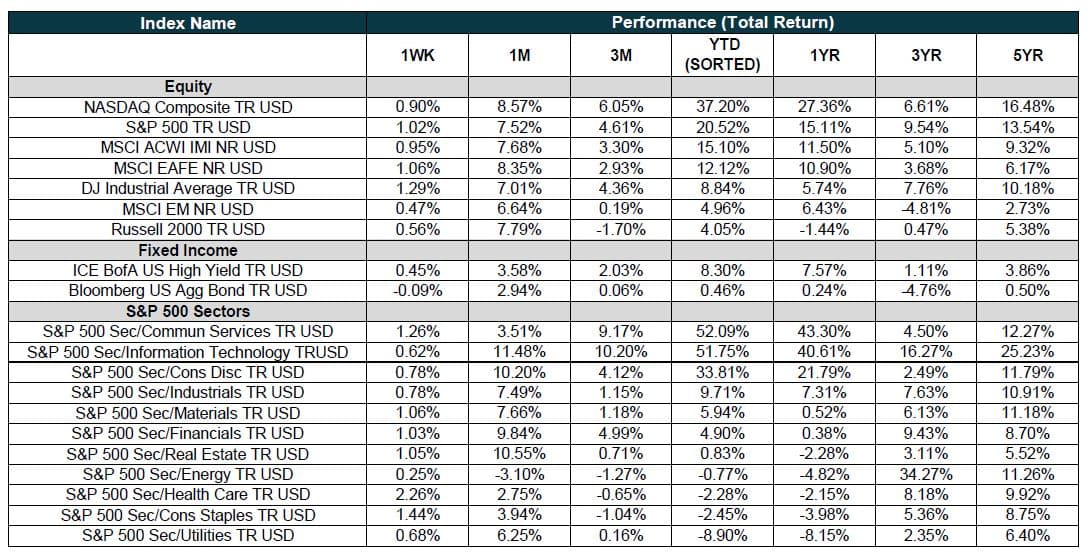

Thanksgiving week has historically been a productive one for US equity markets. Since 1961, the S&P 500 has delivered positive returns two-thirds of the time[1]. And that pattern held true in 2023, with the S&P 500 ending the week with a return of 1%, moving higher for the fourth week in a row[2].

Microsoft got the week off to a strong start, hitting an all-time high on Monday[3]. Market participants cheered the company’s quick hiring of ex-OpenAI CEO Sam Altman, who had been stunningly fired the Friday prior. Altman had led OpenAI since 2019 and was an initial investor in the company in 2015. His sacking caused a furor at OpenAI, which saw over 500 employees sign a letter demanding his reinstatement[4]. They didn’t need to wait long, as OpenAI and Altman came to an agreement on Tuesday night that brought him back into the fold. Though Microsoft ended up losing Altman, having him at Open AI – where Microsoft has invested $13 billion – is better than losing Altman to a competitor.

NVIDIA was the other big newsmaker last week. The company blew away earnings estimates with its latest quarterly report, delivering outstanding results on both the top and bottom lines. The company posted revenue of $18.1 billion versus expectations of $16.1 billion, and earnings of $4.02/share versus expectations of $3.36/share[5]. Market reaction was muted, however, as export restrictions on China dampened expectations for the fourth quarter.

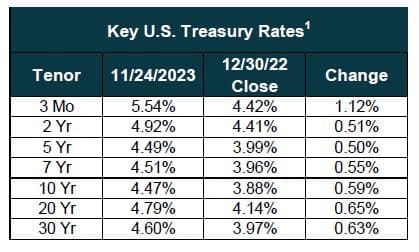

With little new economic data coming in during the holiday-shortened week, bond market participants looked to the minutes from the Federal Reserve’s October 31/November 1 meeting for hints on the future direction of interest rates. The minutes supported the market consensus that the Fed is done raising rates[6]. However, that doesn’t mean rates will be cut any time soon. The CME FedWatch Tool, which uses Fed Funds futures pricing data to generate probabilities for different levels of interest rates, shows the odds of a rate cut no better than 50% until May 2024[7].

This week brings new readings on home sales, jobless claims, and PCE inflation – the Fed’s favored inflation metric. We’ll also get a reading on the consumer, as numbers come in for Black Friday, Cyber Monday, and Travel Tuesday.

[1] https://finance.yahoo.com/news/why-thanksgiving-week-is-typically-bullish-for-stocks-110047943.html

[2] https://www.cnbc.com/2023/11/24/stock-market-today-live-updates.html

[3] https://www.reuters.com/markets/us/futures-edge-higher-microsoft-shines-2023-11-20/

[4] https://www.cnn.com/2023/11/20/tech/openai-employees-quit-mira-murati-sam-altman/index.html

[5] https://finance.yahoo.com/news/nvidia-earnings-crush-wall-street-estimates-again-company-tempers-china-outlook-212952215.html

[6] https://www.reuters.com/markets/us/fed-minutes-likely-anchor-careful-approach-policy-2023-11-21/

[7] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets