Record-Setting Rally Continues

by Sequoia Financial Group

by Sequoia Financial Group

Consumer prices, producer prices, a Federal Reserve meeting, and manufacturing and service reports made last week an action-packed one for the financial markets. Benign inflation reports would support a continued pause in the Fed’s string of interest-rate hikes, while an upside inflation surprise would signal a risk of even higher interest rates heading into 2024.

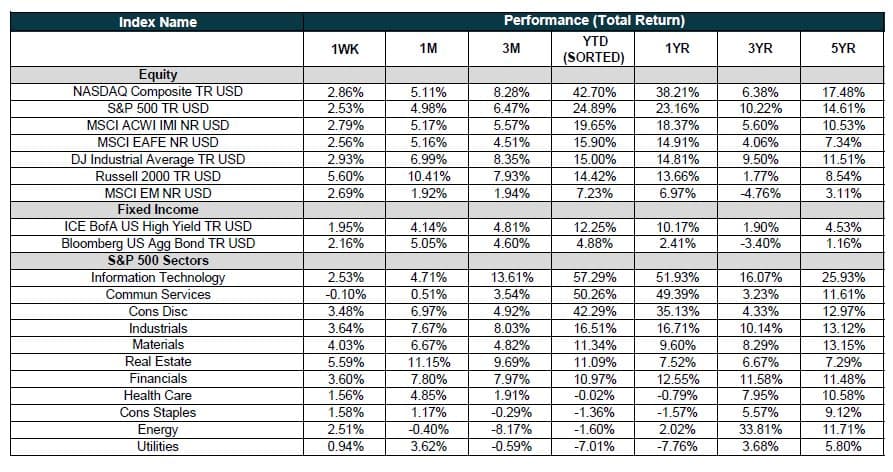

The Consumer Price Index (CPI) hit the tape on Tuesday and stocks surged higher as November inflation creeped ahead by just 0.1%. Year-over-year inflation climbed just 3.1%[1]. The report pushed all three major stock indices to 52-week highs[2]. The energy sector was the lone sore spot in market performance. Continued production gains in the US pushed oil prices to their lowest level since July. US oil production set a new annual record in 2023, besting the mark set in 2019[3]. Oil’s not dead yet, despite record sales of electric cars, and efforts to shift power from fossil fuels to renewables.

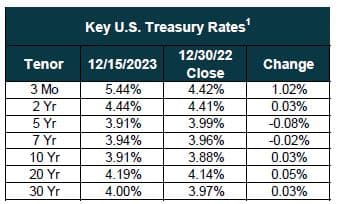

Producer prices set the tone for another good day on Wednesday, coming in unchanged from October[4]. But the Federal Reserve was the big newsmaker, as Chairman Powell leaned into the benign inflation reports and held interest rates steady. Even more important, Powell surprisingly forecast three rate cuts in 2024, signaling to the financial markets that the rate-hiking cycle is, in essence, over. Stock and bond prices soared following the report, with the Dow Jones Industrial Average reaching a record high and closing above 37,000 for the first time[5]. Bond prices also rallied, pushing the 10-year Treasury yield down to 4.03%, its lowest level since August.

The broad rally spilled into Thursday, with the 10-year Treasury yield slipping below 4% and stocks continuing to move higher[6]. Small-cap stocks were the biggest winners, surging more than 5% for the week and a whopping 10% for the month. But despite the ferocious rally, small-cap stocks remain on pace to underperform their large-cap peers for the third year in a row. The equity markets took a breather on Friday but ended with their seventh consecutive winning week[7].

Will large caps continue their dominance in 2024? Will bonds continue to recover? Will the Fed actually cut rates three times? Will the economy have the soft landing that is now priced into the market? Answers to those questions will become clearer as the new year progresses. For now, we’ll enjoy the market’s recent gains, and wish everyone a safe and enjoyable holiday season. Look for our next update the first week in January.

[2] https://www.cnbc.com/2023/12/11/stock-market-today-live-updates.html

[3] https://www.forbes.com/sites/rrapier/2023/12/15/us-producers-have-broken-the-annual-oil-production-record/

[5] https://www.cnbc.com/2023/12/12/stock-market-today-live-updates.html

[6] https://www.cnbc.com/2023/12/13/stock-market-today-live-updates.html

[7] https://www.cnbc.com/2023/12/14/stock-market-today-live-updates.html#:~:text=Dow%20closes%20higher%20for%20seventh,%25%2C%20to%20close%20at%2037%2C305.16.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets