October Data Offers More Support for Goldilocks Scenario

by Sequoia Financial Group

by Sequoia Financial Group

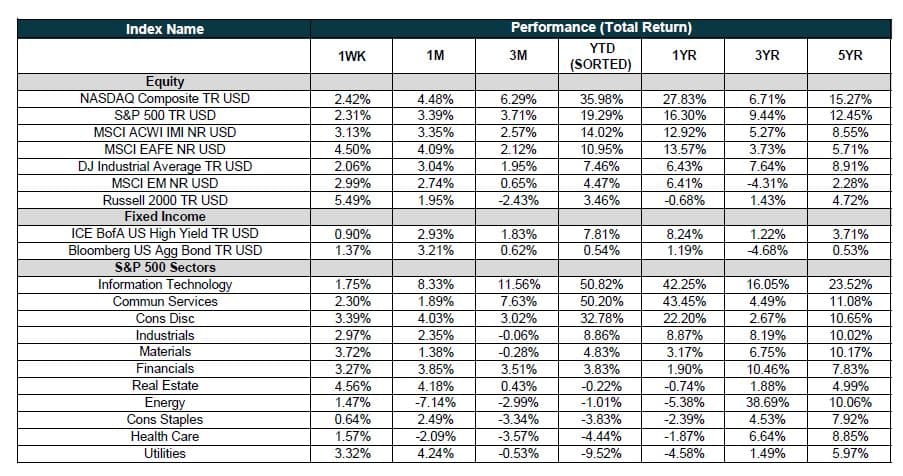

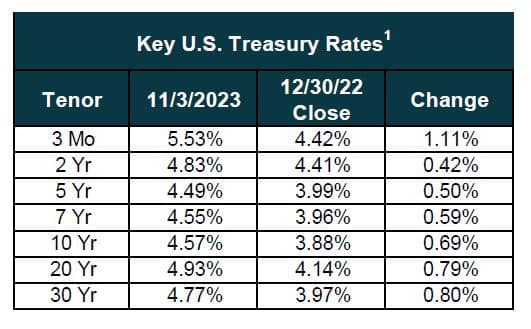

Equity markets rallied sharply last week as macroeconomic data supported the current Fed peak and soft-landing narratives. All sectors were higher, led by real estate, materials, and utilities. Breadth was strong, led by the Russell 2000 rising nearly 5.5%, marking its second-best weekly performance of the year. The S&P 500 and NASDAQ Composite rose 2.31% and 2.42%, respectively, and posted their third straight week of gains. Treasury yields trended lower driven by softer-than-expected inflation numbers.

US markets started the week quietly on Monday and traded in a narrow range throughout the day. Markets opened lower partially driven by late Friday’s news that Moody’s cut its outlook on US debt to negative from stable.1 Odds of a government shutdown fell as House Speaker Johnson pushed forward a clean stopgap funding bill that extends funding for several departments and excludes some demands from House conservatives.2

Markets jumped higher on Tuesday’s softer-than-expected CPI report. CPI was flat in October and increased 3.2% yoy but both measures were below consensus.3 Core CPI rose 4% yoy, the smallest increase since September 2021.3 These numbers were driven by declines in hotels, used vehicles, and airline fares.3 Shelter costs rose 0.3% for the month, finally showing some signs of relief after representing nearly half of September’s increase.3 Breadth was strong and Big Tech, REITs, and utilities were some of the day’s strongest performers. Energy stocks struggled on the day as the IEA reported the oil market is set to return to a surplus in 2024.4

On Wednesday, equity markets extended Tuesday’s rally as macroeconomic data continued to support slowing inflation and a surprisingly strong US consumer. For the first time since March, retail sales fell 0.1% and retail ex-auto rose 0.1% in October, but results were better than expected.5 Online sales were higher but notable declines were seen in auto sales, furniture, department stores, and sporting goods/hobbies.5 Treasury yields were weaker across the curve as the soft-landing narrative gained support driven by cooling inflation and resilient consumer spending. PPI fell 0.5% in October, beating estimates of a 0.1% increase and the biggest monthly drop since April 2020.6 The declines were driven primarily by gasoline prices, which fell 15.3%.6

Equity markets were quiet on Thursday and Friday as investors continued to digest recent macroeconomic developments. Initial jobless claims were 231K, higher than consensus of 220K, but still remain at historically low levels.7 October housing starts were 1372K (+1.9%) while building permits rose 1487K (+1.1%), both metrics surprising on the upside.8 Despite the rise, housing starts and permits may remain constrained by high rates and affordability.

Sources

- https://www.cnbc.com/2023/11/10/moodys-cuts-usa-outlook-to-negative-citing-higher-interest-rates-and-deficits.html

- https://www.cnbc.com/2023/11/13/government-shutdown-house-funding.html

- https://www.bls.gov/news.release/pdf/cpi.pdf

- https://www.reuters.com/markets/commodities/iea-raises-oil-demand-growth-forecasts-despite-economic-gloom-ahead-2023-11-14/#:~:text=The%20Paris%2Dbased%20IEA%20said,until%20the%20end%20of%20December

- https://www.census.gov/retail/marts/www/marts_current.pdf

- https://www.cnbc.com/2023/11/15/wholesale-prices-fell-0point5percent-in-october-for-biggest-monthly-drop-since-april-2020.html

- https://www.dol.gov/ui/data.pdf

- https://www.census.gov/construction/nrc/pdf/newresconst.pdf

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets