Is the “Goldilocks” Scenario Starting to Play Out?

by Sequoia Financial Group

by Sequoia Financial Group

A busy week with continuing 3Q earnings, a Fed meeting, and economic data started with a bang, as the Dow Jones Industrials Index soared more than 500 points Monday[1]. The stock market had closed the prior week at its lowest level since May, and bargain hunters finally found prices to their liking. Stocks were bid higher in hopes that the Fed would hold rates steady on Wednesday, Apple would announce good earnings on Thursday, and the jobs report would show an economy growing neither too fast nor too slow Friday.

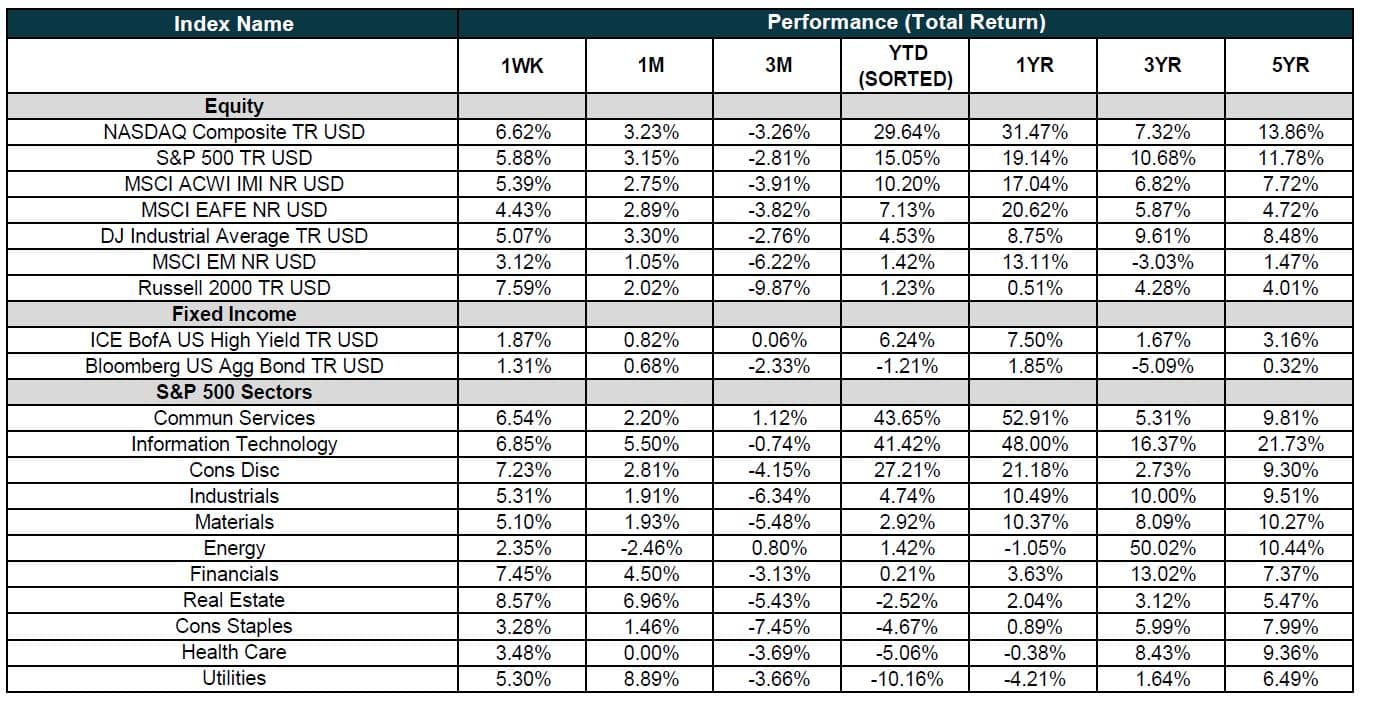

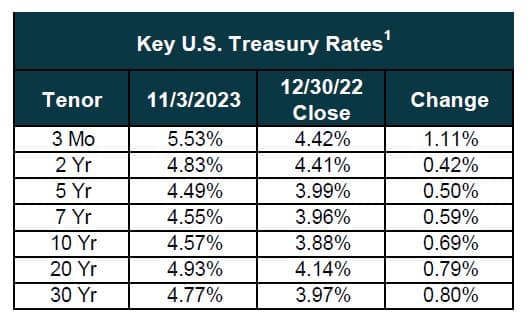

The market went three for three. After closing out its third losing month in row, the stock market started November strong. The Federal Reserve kept rates unchanged[2], and a weaker-than-expected manufacturing report[3] showed that the Fed’s efforts to cool the economy were having the desired effect, and that additional rate hikes might not be needed. Stocks and bonds rallied Wednesday, with the NASDAQ jumping more than 1.5% and the 10-year Treasury yield pulling back to 4.79%.

The rally continued on Thursday. The S&P 500 had its best day since April, on news that labor costs had unexpectedly dropped in the third quarter[4]. The data provided even more evidence that the Fed’s string of rate hikes continues to slow inflation. The report also showed a surprising increase in productivity, with the largest quarterly gain in productivity since 3Q/20. Apple rallied more than two per cent prior to its after-the-bell earnings report[5]. Earnings beat analyst estimates, but Apple forecast flat sales for the holidays and the stock gave back some of its gains. But overall, it was considered a solid report and did little to dampen market’s positive mood.

The week closed strong thanks to a “Goldilocks” jobs report for October, which showed the economy added 150,000 new jobs, slightly lower than the 180,000 expected[6]. This indicates the economy is still growing at a decent clip, but not so fast as to encourage the Fed to continue raising interest rates. The odds of a December rate hike dropped to less than 5% at week’s end from close to 20% a week ago and near 30% a month ago[7]. Overall, the financial markets enjoyed their best week of the year, with the S&P 500 rallying more than 5% and the Bloomberg Aggregate Bond Index climbing more than 1%[8].

[1] https://www.cnbc.com/2023/10/29/stock-market-today-live-updates.html

[2] https://www.federalreserve.gov/newsevents/pressreleases/monetary20231101a.htm

[3] https://www.cnbc.com/2023/10/31/stock-market-today-live-updates.html

[4] https://www.cnbc.com/2023/11/02/labor-costs-show-surprise-decline-in-the-third-quarter.html

[5] https://www.cnbc.com/2023/11/01/stock-market-today-live-updates.html

[6] https://www.msn.com/en-us/money/markets/dovish-fed-goldilocks-jobs-report-drives-s-p-to-best-week-of-2023-nasdaq-dow-also-rip/ar-AA1jl30o

[7] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

[8] Bloomberg

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets