Is the Federal Reserve really done?

by Sequoia Financial Group

by Sequoia Financial Group

With the Federal Reserve having voted to leave interest rate unchanged at their September and November meetings, and the federal funds futures markets assigning just a 1% probability of a rate increase at the upcoming December meeting1., financial markets have rallied in November as both traders and investors believe the Fed was done raising rates and that the central bank may even start cutting them in the first half of next year.

However, on Friday, Federal Reserve Chair Jerome Powell pushed back against the market’s expectations for interest rate cuts ahead, saying it is “premature to conclude with confidence” that monetary policy is “sufficiently restrictive.”2.

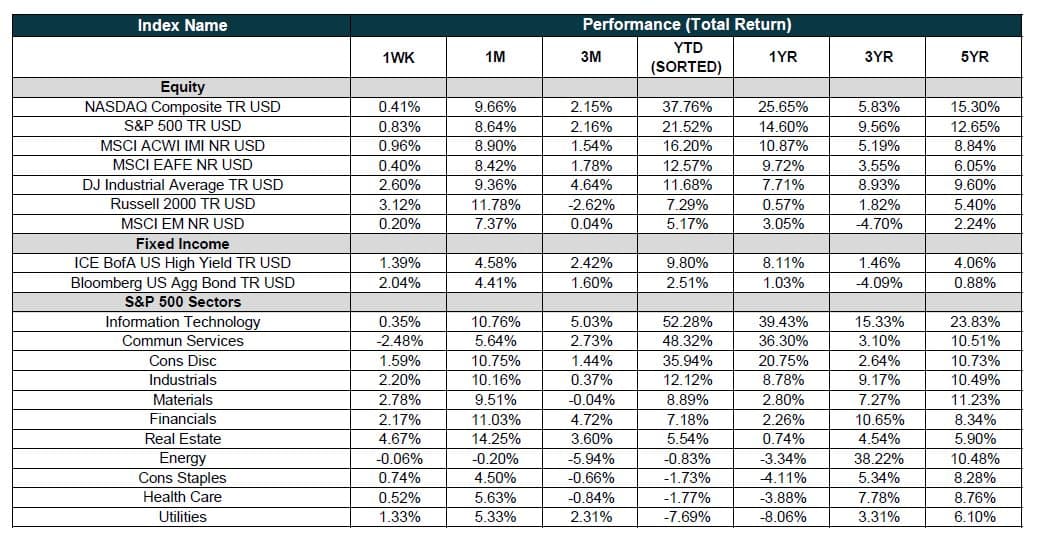

Last week the Nasdaq advanced 0.41%, the S&P 500 added 0.83%, while the Dow rallied 2.6%.3. It marked the fifth consecutive week of gains for the major averages. Within the Dow index, Salesforce led the index higher as investors cheered the software company’s earnings report. With a jump of 15.87%, the stock notched its best week since August 2020. Boeing and American Express also saw large gains, adding more than 6.30% and 5.68%, respectively. Disney posted the largest loss this week with a drop of 3.62%. The Bloomberg US Agg bond index rose 2.04%.

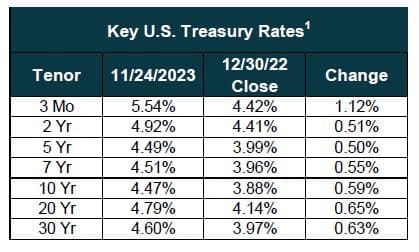

November’s gains snapped a three-month losing streak. The S&P rose 9.13% and the Nasdaq rallied 10.83%, respectively, solidifying their best monthly performances since July 2022. The Dow surged 9.15% for its best month since October 2022.4. In the fixed income markets, the Bloomberg US Agg bond index rose 4.53% during the month as the benchmark 10-year Treasury yield declined from 4.88% to 4.37% over the same period.5.

In economic news, data released on Friday showed that U.S. manufacturing remained at low levels in November, according to the Institute for Supply Management, which said that its manufacturing PMI was unchanged at 46.7 last month. November was the 13th straight month during which the PMI came out below 50, which is an indicator of a slowdown in manufacturing.6.

On Wednesday, the Bureau of Economic Analysis reported that Real gross domestic product (GDP) increased at an annual rate of 5.2 percent in the third quarter of 2023, according to the “second” estimate. The increase in the third quarter primarily reflected increases in consumer spending and inventory investment. Imports, which are a subtraction in the calculation of GDP, increased.7.

However, one of the most closely followed economic data points released last week was the Personal Consumption Expenditures (”PCE”) report, the Federal Reserve’s preferred measure of inflation. Inflation as measured by personal spending increased in line with expectations in October, possibly giving the Federal Reserve more incentive to hold rates steady, according to a data release Thursday. The personal consumption expenditures price index, excluding food and energy prices, rose 0.2% for the month and 3.5% on a year-over-year basis, the Commerce Department reported.8. Both numbers aligned with the Dow Jones consensus and were down from respective readings of 0.3% and 3.7% in September.

A decline in energy prices was cited as a positive factor in last month’s inflation report, a direct result of the recent weakness in oil prices. After peaking in late September at $94, West Texas Intermediate (“WTI”) continued to fall in November to end the month at $75. The decline in oil prices and concerns over slower economic growth in 2024, prompted OPEC+ members, who met last week, to agree to remove around 2.2 million barrels per day (bpd) of oil from the global market in the first quarter of next year, which included a rolling over of Saudi Arabia and Russia’s current 1.3 million bpd of voluntary cuts.9.

Sources:

- https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- https://www.cnbc.com/2023/11/30/stock-market-today-live-update.html

- Morningstar Direct

- Morningstar Direct

- https://home.treasury.gov/resource-center/data-chart-center/interest-rates

- https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/pmi/november

- https://www.bea.gov/data/gdp/gross-domestic-product

- https://www.bea.gov/news/2023/personal-income-and-outlays-october-2023

- https://www.cnbc.com/2023/12/01/oil-prices-fall-extend-slide-after-opec-cuts-underwhelm.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets