Market Commentary

Markets Rebound as Tariff Ruling, Slowing Growth, Sticky Inflation Shape Outlook

by Sequoia Financial Group

by Sequoia Financial Group

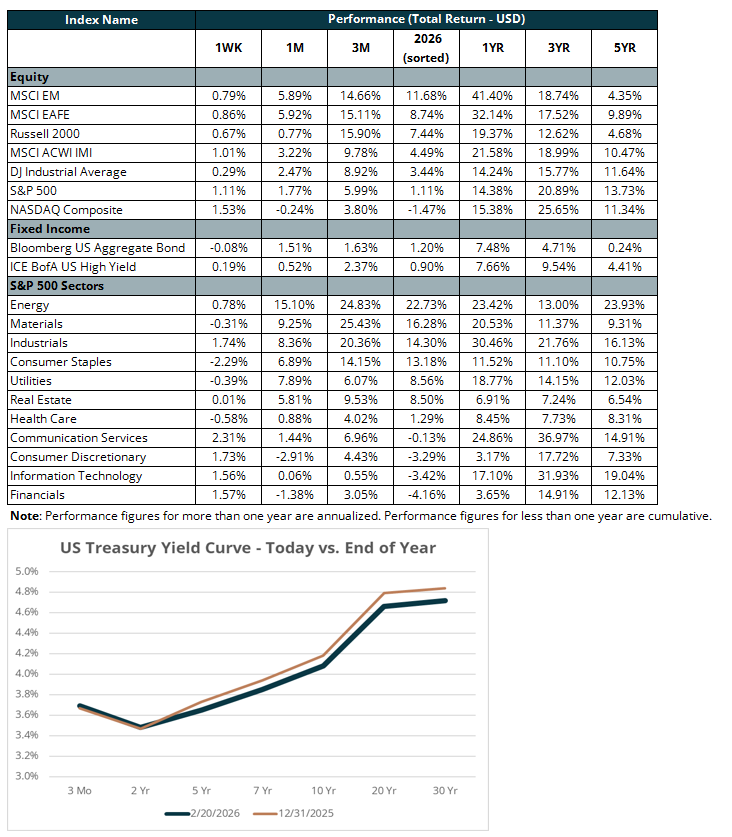

U.S. stocks recouped much of the prior week’s losses, extending a volatile start to 2026. The NASDAQ led the rebound, rising 1.5 percent for the week and ending a five-week losing streak, while the S&P 500 gained 1.1 percent to snap a two-week decline, and the Dow Jones Industrial Average added 0.3 percent; the Russell 2000 was little changed, up 0.1 percent. On Friday, equities moved higher, with the S&P 500 up 0.7 percent, the Dow up 0.5 percent, and the NASDAQ up 0.9 percent, as markets reacted to the Supreme Court’s decision on tariffs. Trading remained measured amid data pointing to slower growth and firmer inflation, and Treasury yields were largely steady.

In a 6-to-3 ruling, the U.S. Supreme Court held that the President exceeded his authority by imposing sweeping tariffs under the 1977 International Emergency Economic Powers Act, ruling that the statute did not grant authority to levy such tariffs, while affirming that the President retains tariff authority under other statutory measures enacted by Congress. The decision invalidated a substantial portion of the administration’s trade measures and left unresolved whether the government must refund the roughly $130 billion in duties already collected under the statute. Although the outcome had been widely anticipated, uncertainty persists around the longer-term economic and market effects. The President sharply criticized the ruling and quickly moved to pursue alternative authority, initially announcing a 10 percent global tariff on imports under Section 122 of the Trade Act of 1974, with implementation slated for late February. He subsequently indicated the rate could rise to 15 percent, the maximum permitted under that provision, which allows tariffs to remain in place for about five months before requiring congressional approval. The potential increase has raised new questions for key trading partners and keeps trade policy risks firmly in focus.

On the economic front, growth cooled more than expected in the fourth quarter. GDP expanded at a 1.4 percent annualized pace, down sharply from 4.4 percent in the third quarter and below consensus expectations near 2.5 percent. The deceleration was driven in part by the prolonged government shutdown, which the Commerce Department estimated reduced growth by about one percentage point, alongside softer consumer spending and a pullback in exports. While underlying private demand remained relatively steady and investment improved, the headline slowdown marked a loss of momentum as 2025 closed, with full-year growth of 2.2 percent, down from 2.8 percent in 2024. The slowdown has reinforced expectations that the Fed will maintain a cautious stance after cutting rates late last year.

Inflation, meanwhile, showed little sign of easing. The Federal Reserve’s preferred measure, the Personal Consumption Expenditures index, rose 2.9 percent year over year in December, the fastest pace in nearly a year, while core PCE increased 3 percent. Both headline and core prices have advanced 0.4 percent each month, suggesting price pressures remain broad-based and above the Fed’s 2 percent target.

Against this backdrop, Treasury yields moved higher but remained below recent highs. The 10-year U.S. Treasury yield ended the week near 4.08 percent, up slightly from the prior week’s 4.05 percent, yet still well below the mid-January peak of roughly 4.3 percent, which had marked its highest point since last August.

Looking ahead, markets enter a consequential week shaped by earnings and macro crosscurrents. NVIDIA reports on Wednesday, with its outlook and CEO commentary seen as key for AI sentiment amid high expectations and hyperscaled capex plans. Software results from Salesforce and Snowflake will test AI disruption concerns, while retailers Home Depot and Lowe’s offer a read on consumer demand. Markets are also digesting the Supreme Court’s decision on tariffs alongside soft Q4 GDP and sticky inflation, with the S&P 500 only modestly higher year to date amid sharp sector rotation.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Hopes of Peace Lift Markets, but Caution Still Warranted