Equities on Six-Week Winning Streak

by Sequoia Financial Group

by Sequoia Financial Group

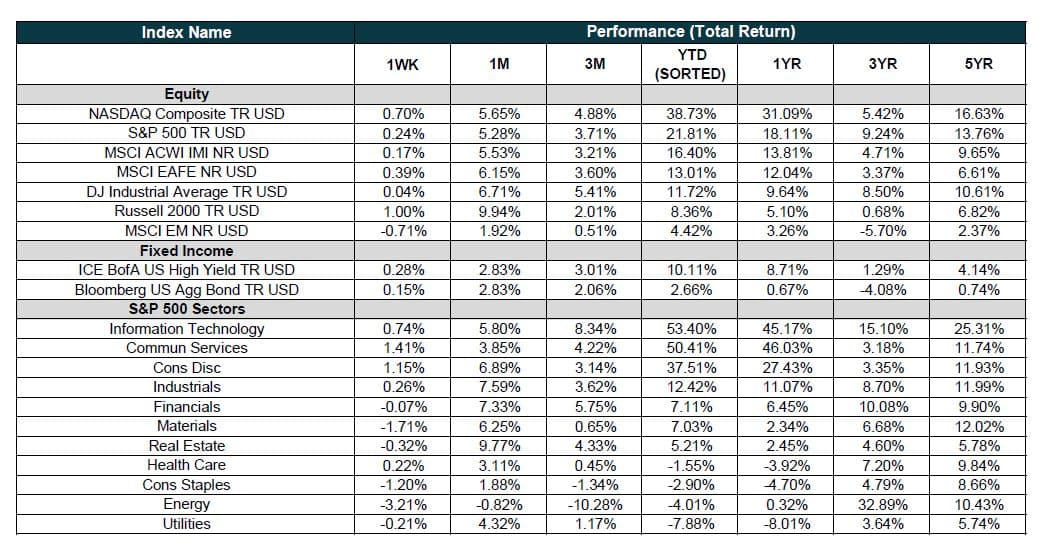

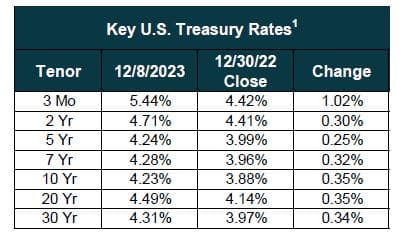

Equity markets rose last week as the US labor market continues to show resiliency. Small caps continued their leadership with the Russell 2000 higher by 1%. The NASDAQ and S&P 500 advanced by 0.70% and 0.24%, respectively. In contrast to previous weeks, Treasury yields were up on the week.

Markets started the week looking for a direction and traded within a narrow range on Monday. Small caps added to the previous week’s gains with the Russell 2000 higher by 1.04% for the day. Overall, it was a quiet session with continued rotation out of the Magnificent Seven and year-to-date winners and strength in the broader market.

US equities were mixed on Tuesday, with NASDAQ outperforming other market indices. October Job Openings and Labor Turnover Survey (JOLTS) came in at 8.773 million, well below consensus expectations of 9.3 million and last month’s 9.553 million.1 The report marked the third straight month of declines and the lowest level since March 2021. 1 ISM Services PMI came in at 52.7, better than the consensus estimate of 52.4.2 Respondents mentioned generally stable conditions but still see inflationary pressure and a tight labor market.2 Both reports strengthened the soft-landing narrative driven by a strong labor market and consumer spending.

Markets took a breather on Wednesday and most major indices were lower. Oil prices declined nearly 4.2% and ended below $70/barrel for the first time since July. Similarly, natural gas futures continue to struggle and are lower by nearly 74% since their August 2022 peak. We continued to see evidence of a cooling labor market, with the latest ADP employment survey showed a gain of 103,000 net new jobs, below estimates of 127,000.3

Initial jobless claims came in at 220,000, slightly below estimates of 223,000.4 Jobless claims have ticked up over the last several weeks but still indicate a strong labor market. 4 The prevailing AI narrative continues to show strength with positive reactions to AMD’s new AI chip and GOOG’s AI event. Overall, equity markets climbed higher on Thursday in an uneventful trading session as investors awaited Friday’s jobs report.

Nonfarm payrolls added 199,000 jobs, beating estimates of 175,000.5 The unemployment rate fell to 3.7% vs expectations of 3.9% and the labor participation rate ticked higher to 62.8%, the highest level since February 2020. 5 Reports of a still-resilient US labor market were well-received. US markets were higher on Friday and ended near the YTD highs set back in July. Both the S&P and NASDAQ locked in a sixth consecutive week of gains. University of Michigan Consumer Sentiment came in at 69.2, well ahead of expectations of 61.9, as one-year inflation expectations fell to 3.1%, their lowest level since March 2021.6

Sources

- https://www.bls.gov/news.release/jolts.nr0.htm

- https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/services/november/

- https://adp-ri-nrip-static.adp.com/artifacts/us_ner/20231206/ADP_NATIONAL_EMPLOYMENT_REPORT_Press_Release_2023_11%20FINAL.pdf

- https://www.dol.gov/ui/data.pdf

- https://www.bls.gov/news.release/empsit.nr0.htm

- https://www.cnbc.com/2023/12/08/inflation-expectations-plunge-in-closely-watched-university-of-michigan-survey.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Strong Earnings and Inflation-friendly Data Boost Markets