Market Commentary

U.S. Equities Extend Winning Streak on Strong Earnings and Iran Peace Deal Hopes

by Sequoia Financial Group

by Sequoia Financial Group

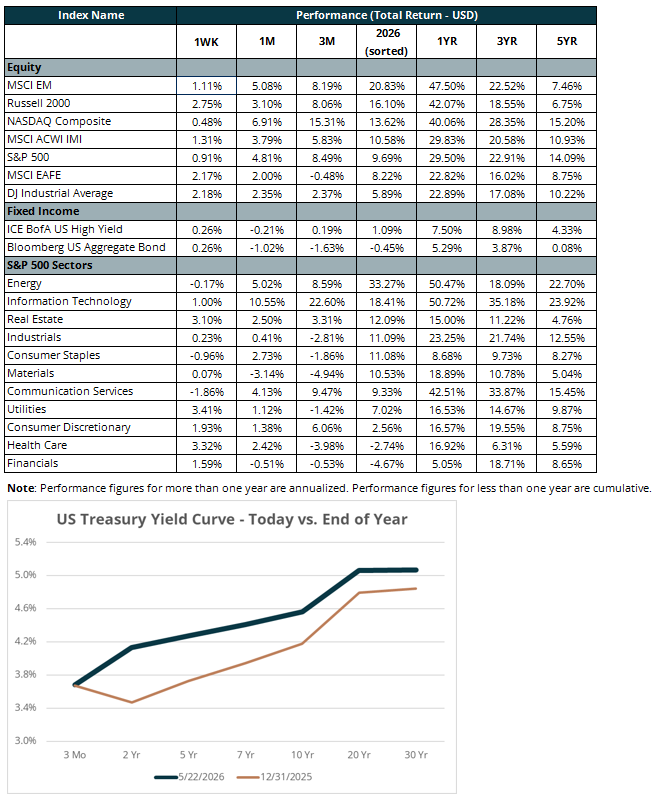

U.S. equities moved higher last week, with the S&P 500 advancing 0.9 percent – its eighth consecutive weekly gain and the longest such streak since 2023. The Russell 2000 fared even better, rising 2.7 percent. Yields were largely unchanged on the week, allowing U.S. bonds to return 0.3 percent, with the 10-Year Treasury continuing to hover above 4.5 percent as concerns about sustained inflation and higher fiscal deficits offset the downward pressure from falling oil prices. The week’s gains were fueled by two complementary tailwinds: growing optimism that a framework to end the U.S.-Iran conflict may be within reach, and a Q1 earnings season that has meaningfully exceeded expectations.

Developments in the Iran conflict continued to be the dominant driver of market sentiment. WTI crude fell sharply on the week, down roughly eight percent, as diplomatic headlines sparked optimism about a potential resolution. The U.S. administration indicated that a framework for ending the war and reopening the Strait of Hormuz has been largely negotiated, with a proposed three-stage process involving a formal end to hostilities, resolution of the Strait, and a broader 30-to-60 day negotiating window. Under the proposed terms, the Strait would reopen without tolls and Iran would clear mines; in return, the U.S. would lift its blockade and allow Iran to sell oil freely. Key sticking points remain, however, including the disposition of Iran’s highly enriched uranium stockpile and the timing of sanctions relief. The White House indicated that final approval from Iran’s senior leadership would likely extend into this week, and Iran has not yet committed to handing over its nuclear material. Ships in the Persian Gulf have begun repositioning in anticipation of a deal, though market participants will watch closely for confirmation of a finalized agreement.

The market continued to be bolstered by the strong Q1 earnings season. With 94 percent of S&P 500 companies having reported, the year-over-year blended earnings growth rate (which combines actual results with consensus estimates for firms that have yet to report) stands at 28 percent, well above the 13 percent expected at the start of the quarter. At that rate, the quarter would represent the strongest earnings growth the S&P has seen since Q4 2021. NVIDIA (NVDA) provided the week’s most closely watched result, reporting another beat-and-raise quarter driven by continued AI demand, with Data Center revenue up 92 percent year over year. Separately, the April FOMC minutes released during the week carried a hawkish tone, with many participants pushing to remove the statement’s easing bias. Kevin Warsh was sworn in as Fed Chair on Friday, inheriting a deeply divided committee. Futures markets now assign nearly equal probability to rates remaining unchanged and at least one hike through the end of the year.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory