Market Commentary

Megacap Weakness, AI Momentum, and Hawkish Fed Repricing Drive Markets

by Sequoia Financial Group

by Sequoia Financial Group

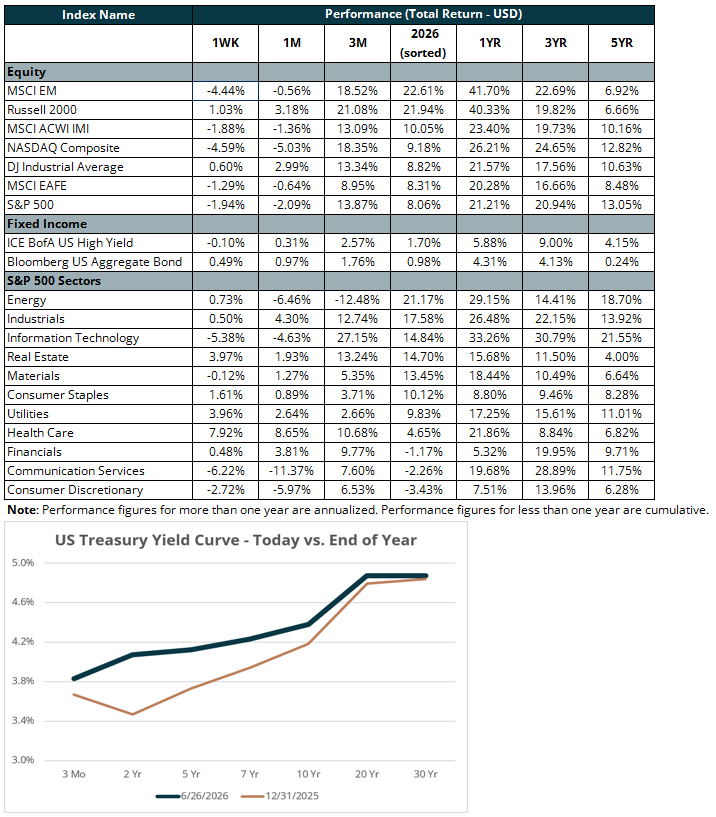

Geopolitics, artificial intelligence, and inflation each took their turn commanding market attention last week. U.S. equities were mixed, as a pullback in technology names masked broadening performance beneath the surface. The S&P 500, an index of the largest U.S. companies, fell 1.9%, and the technology-heavy Nasdaq Composite dropped 4.6%, weighed down by weakness in megacap and semiconductor names. The Dow Jones Industrial Average and small-cap Russell 2000 fared better, rising 0.6% and 1.0%, respectively.

The divergence extended the broadening-out theme that has characterized 2026, as investors rotated beyond the largest growth names. Yields fell across the Treasury curve, helping the Bloomberg U.S. Aggregate Bond Index (the “Agg”), a broad measure of investment-grade fixed income, return 0.5%.

Artificial intelligence was the dominant market theme last week. Early-week softness in semiconductor and memory names appeared more driven by concentration concerns than by any deterioration in fundamentals, as evidenced by Micron’s blowout earnings results. Micron (MU), a leading manufacturer of memory and storage chips, reported revenue growth of 74% from the prior quarter and over 4x year-over-year.

Management noted they expect tightness in memory supply through 2027, reinforcing the durability of elevated margins for memory companies. The average selling prices of Micron’s two most prominent chips increased 63% and 87% sequentially. Those steep price increases point to the AI buildout proving inflationary in the near term, as seen in Apple’s recent 15–25% price increase for Macs and iPads driven by soaring memory costs. Much now rests on the productivity gains the technology is expected to deliver, which would prove disinflationary over time.

Geopolitics faded as a market driver, with WTI crude settling roughly 9% lower on the week, back near its pre-war level, as flows through the Strait of Hormuz accelerated. Headlines out of the Middle East continued, but the market largely looked through them. With the energy shock easing, attention returned to inflation and the path of Fed policy.

The May core PCE reading, the Fed’s preferred inflation gauge, came in at 3.4% year-over-year, its highest level since 2023. Against that backdrop, markets have continued to reprice Fed expectations hawkishly. According to CME Group’s FedWatch tool, markets now assign a 41% probability to 25 basis points of rate hikes by year-end and a 28% probability to 50 basis points — a notable shift from one month ago, when the market placed a 52% probability on no hikes through year-end.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

Broken Iran Ceasefire Can’t Hold Back Equities