Market Commentary

Broken Iran Ceasefire Can’t Hold Back Equities

by Sequoia Financial Group

by Sequoia Financial Group

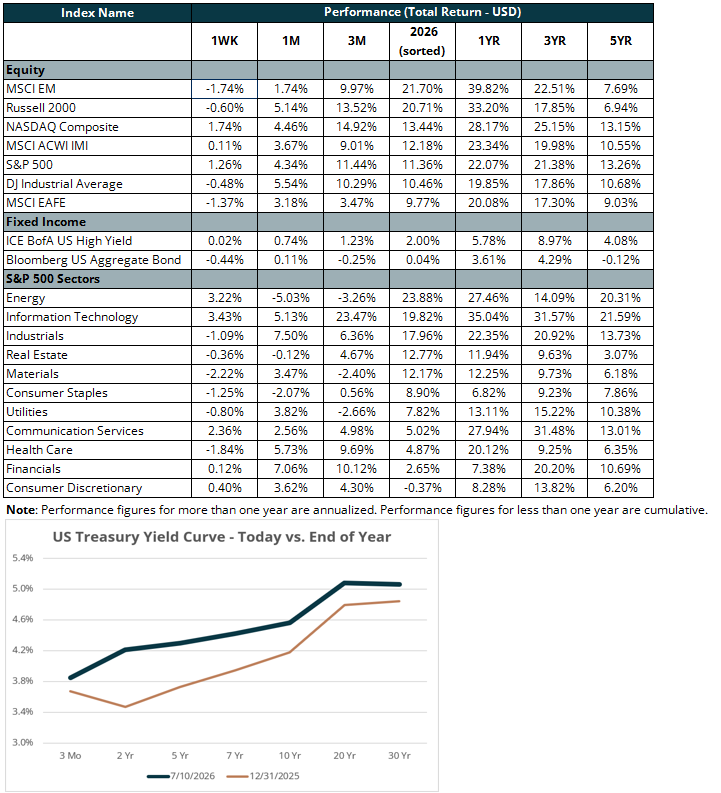

Equity markets finished the week mostly higher: the S&P 500 gained 1.3 per cent (up 11.4 per cent year to date [YTD]) and the NASDAQ climbed 1.7 per cent (up 13.4 per cent YTD), while the Dow Jones Industrial Average slipped 0.5 per cent (still up 10.5 per cent YTD). The tech-heavy NASDAQ benefited from a semiconductor rebound and renewed enthusiasm for AI infrastructure names. The Dow, weighted more toward “old economy” stocks than high-growth names, captured none of last week’s gains.

President Trump kicked off last week’s trading, ringing the opening bell from the Oval Office. Monday marked the launch of “Trump Accounts,” a new child savings program under the One Big Beautiful Bill Act that seeds a $1,000 Treasury-funded contribution for children born between 2025 and 2028. The launch underscores this administration’s particular emphasis on economic and market conditions. Following his Liberation Day in April 2025, Trump extended a tariff deadline following a nearly 10% single-day selloff. The president later admitting investors got too “yippy.” That awareness seems to be paying off. The S&P 500 is running well ahead of its historical pace through the first 1.5 years of a presidential term. The index finished 0.7% higher on Monday.

Sentiment shifted Tuesday despite Samsung Electronics’ blowout results. The South Korean company’s operating profit increased more than 1,800% year-over-year, triggering profit-taking rather than celebration. The pressure spilled into U.S. AI-infrastructure names. GE Vernova (ticker: GEV) fell roughly 8% on valuation concerns after a run that had left the stock trading at nearly 59 times trailing earnings. The same day, Iran’s Revolutionary Guard fired missiles at two commercial ships near the Strait of Hormuz, including an LNG tanker whose crew reported an engine-room fire. Oil spot prices advanced 3% as a result.

Speaking at the NATO summit the following day, President Trump said of the ceasefire, “To me, I think it’s over, I don’t want to deal with them anymore.”. Brent crude jumped more than 5% to roughly $78 a barrel, a sharp reversal after weeks of prices drifting back toward prewar levels. Treasury yields moved higher across the curve as the renewed oil spike revived inflation concerns: the 10-year rose more than 4 basis points to 4.571%, the 2-year climbed to 4.206%, and the 30-year added over 2 basis points to 5.069%.

Later in the week, investors rediscovered their appetite for tech names and largely shrugged off a fresh round of U.S.-Iran strikes. SK Hynix’s American Depository Receipts (ticker: SKHYV) traded for the first time on Friday, about +13% higher than the offering price. The company successfully raised $26.5 billion in its Nasdaq debut, giving the AI memory trade a fresh jolt of enthusiasm into the weekend.

Looking ahead to next week, the focus shifts to the lifeblood of equities: earnings. The second quarter’s earnings season ramps Tuesday with US megabanks: JPMorgan (ticker: JPM), Bank of America (ticker: BAC), Goldman Sachs (ticker: GS), Citigroup (ticker: C), and Wells Fargo (ticker: WFC). Many market pundits continue to warn of an AI “bubble.” If earnings continue to surge, however, market levels will likely stay elevated. Aggregate earnings for the S&P 500 are expected to grow more than 20% over the next 12 months, which is more than double the index’s growth over the last 10 years.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

(1)")

")

Equities Slide as Iran Escalation and AI Spending Fears Grip Markets