Insights, Wealth Planning

Unlocking Opportunity With Net Unrealized Appreciation (NUA): A Tax-Smart Retirement Strategy

by Sequoia Financial Group

by Sequoia Financial Group

If you own a substantial amount of employer stock inside your 401(k) or similar retirement plan, there’s a strategy that could help you unlock significant tax savings: Net unrealized appreciation, or NUA.

This approach may be especially valuable for high-net-worth individuals, retirees in high tax brackets, and anyone with highly appreciated company stock in a qualified retirement plan. With proper planning, NUA may create an opportunity to help decrease taxes and optimize wealth in retirement or during a job transition.

What is net unrealized appreciation (NUA)?

Net unrealized appreciation refers to the growth in value of employer stock held in a tax-deferred retirement account. Specifically, NUA is the difference between the stock’s original cost basis and current market value. When NUA rules apply, you can distribute employer stock in-kind (without selling it) from your 401(k), and the tax treatment becomes more favorable:

- The cost basis of the stock (what was initially paid for it) is taxed as ordinary income at the time of distribution.

- The unrealized appreciation, the growth in value, is not taxed until you sell the stock, and when you do, it is taxed as a long-term capital gain, even if you’ve held it for less than a year after distribution.

This may create a meaningful tax opportunity, especially if the appreciation is significant.1-4

NUA vs. No NUA: How Your Company Stock Withdrawal Is Taxed

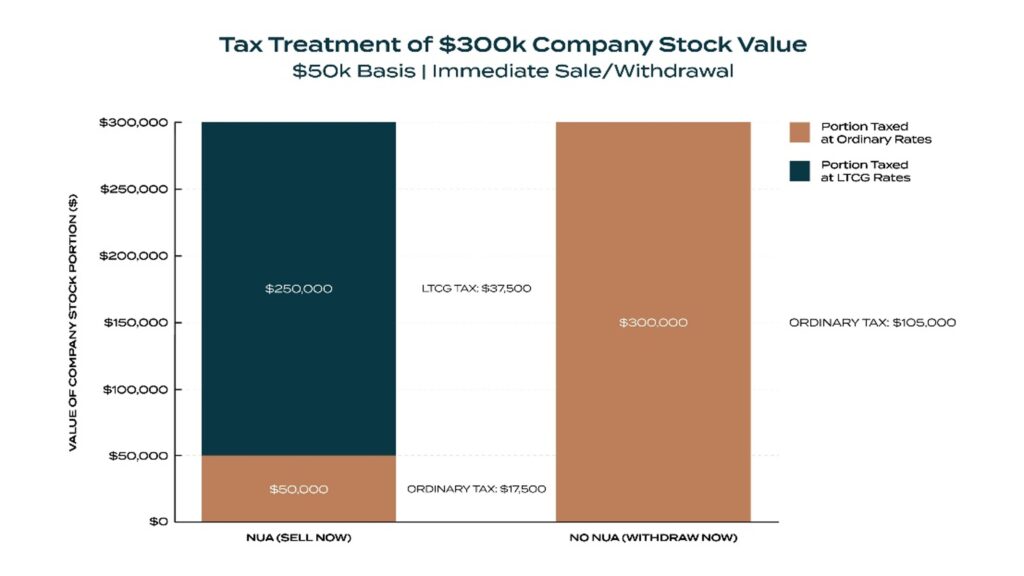

Let’s look at an example of an individual who earns $250,000 per year in taxable income and holds $300,000 worth of company stock with a $50,000 cost basis in their 401(k). The chart below compares the tax impact of withdrawing the stock under two scenarios5-7:

- Using net unrealized appreciation (NUA) rules and selling immediately

- Not using NUA rules and withdrawing the stock from the 401(k) immediately

Scenario 1: NUA (Sell Now)

With NUA, only the original cost basis ($50,000) is taxed at ordinary income tax rates when you withdraw. For a single tax filer with $250,000 in taxable income, their ordinary income tax rate would be 35% and their long-term capital gains tax rate would be 15%.

- Ordinary income portion: $50,000 × 35% = $17,500 in taxes

- The growth ($250,000) is taxed at the long-term capital gains (LTCG) rate instead of higher income tax rates.

- LTCG portion: $250,000 × 15% = $37,500 in taxes

Total taxes: $17,500 + $37,500 = $55,000

Scenario 2: No NUA (Withdraw Now)

If you skip the NUA approach and withdraw the stock as part of a normal 401(k) distribution, the entire $300,000 is taxed as ordinary income rates.

- Ordinary income tax: $300,000 × 35% = $105,000

Total taxes: $105,000

By using NUA in this example, you pay $55,000 instead of $105,000—a $50,000 tax savings.

NUA takes advantage of favorable capital gains rates on the stock’s growth, rather than taxing the entire amount as regular income.

Key Requirements to Qualify for NUA Treatment

Not every situation qualifies for NUA treatment. The IRS has strict requirements8-11:

- Triggering Event: The distribution must follow a qualifying event. This includes:

- Separation from service (e.g., retirement or job change)

- Reaching age 59½

- Disability (for self-employed individuals)

- Death

- Stock Source: The stock must be from a qualified employer-sponsored retirement plan, such as a 401(k).

- In-kind Distribution: The employer stock must be distributed in-kind from a qualified plan; it cannot be sold inside the plan first.

- Lump-sum Distribution: The stock must be part of a lump-sum distribution, which means the entire retirement account is distributed within one tax year. The retirement funds, not company stock, would be rolled over to an individual retirement account (IRA).

- Note: The lump sum distribution does not have to be done in the same year as the triggering event. It can be done in any future tax year after the triggering event, but the distribution must be complete in that one tax year.

Meeting these requirements is essential to capturing the NUA benefit. Missing a step could result in missing the tax advantage.

Strategic Benefits of NUA Planning

If done right, NUA can be a powerful wealth-planning lever. Here’s why:

- Tax Efficiency: You’ll pay ordinary income tax only on the cost basis of the stock, often a small fraction of its current value, while the remaining appreciation is taxed at lower long-term capital gains rates.

- Diversification Flexibility: You don’t have to take the entire account as stock; you can do a partial rollover into an IRA and only distribute the employer stock in-kind, allowing you to diversify the rest of your assets.

- Estate Planning Advantage: Beneficiaries may receive favorable tax treatment if you hold the NUA stock until death. They may benefit from a step-up in cost basis or other planning techniques in certain situations.

When to Consider the NUA Strategy

NUA isn’t right for everyone, but it can be highly effective under the right circumstances:

- Significant Appreciation: If your employer stock has grown considerably in value and has a low-cost basis, the tax savings may be substantial.

- Retirement or Job Change: These events create natural opportunities for a lump-sum distribution.

- Favorable Tax Timing: If you’re currently in a lower tax bracket (for example, just after retirement), you may realize the ordinary income portion at a lower rate.

- Charitable or Legacy Goals: Appreciated stock can be used to make charitable gifts or fund donor-advised funds, leveraging the tax benefits further.

Final Thoughts

Net unrealized appreciation is a nuanced but potentially game-changing strategy in the proper context. While it’s often overlooked in broader retirement planning conversations, its impact on long-term tax savings and legacy planning may be significant. Executing an NUA strategy requires careful timing, strict adherence to IRS rules, and professional guidance to avoid unintended consequences.

At Sequoia Financial Group, we help clients assess whether NUA fits into their broader tax, retirement, and estate planning strategy. Our team has deep experience navigating complex employer stock scenarios and guiding clients through tax-efficient decisions that align with their long-term goals.

If you’re nearing retirement, leaving your job, or want to understand your options better, now is a great time to explore with your advisory team whether NUA could benefit you. Want to learn more about Sequoia, connect with us to begin the conversation.

Sources:

- https://www.investopedia.com/terms/n/netunrealizedappreciation.asp?

- https://turbotax.intuit.com/tax-tips/retirement/net-unrealized-appreciation-nua-tax-treatment-amp-strategies/c71vBJZ2B

- chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.irs.gov/pub/irs-drop/not98-24.pdf

- https://www.irs.gov/taxtopics/tc412

- https://turbotax.intuit.com/tax-tips/retirement/net-unrealized-appreciation-nua-tax-treatment-amp-strategies/c71vBJZ2B

- https://www.fidelity.com/learning-center/personal-finance/retirement/company-stock

- https://wm.calamos.com/newsinsights/advice-and-planning-insights/net-unrealized-appreciation-forgotten-retirement-strategy/

- https://turbotax.intuit.com/tax-tips/retirement/net-unrealized-appreciation-nua-tax-treatment-amp-strategies/c71vBJZ2B?

- https://www.ameriprise.com/financial-goals-priorities/taxes/net-unrealized-appreciation

- https://www.annuities.pacificlife.com/home/resources/planning-strategies/individual-retirement-accounts/traditional-iras/net-unrealized-appreciation-in-a-nutshell.html

- https://www.covenantwealthadvisors.com/post/net-unrealized-appreciation-a-guide-to-tax-efficient-retirement

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

The tax and estate planning information offered by the advisor is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Clients requesting tax return or estate preparation services are referred to a commonly-held affiliate, Sequoia Tax Services or a third party and not Sequoia Financial Group.

")

Equity Performance Mixed as Market Leadership Shifts Beneath the Surface