Market Commentary

U.S. Stocks Surge on Strong Earnings, Eased Trade Tensions, and Consumer Spending Growth

by Sequoia Financial Group

by Sequoia Financial Group

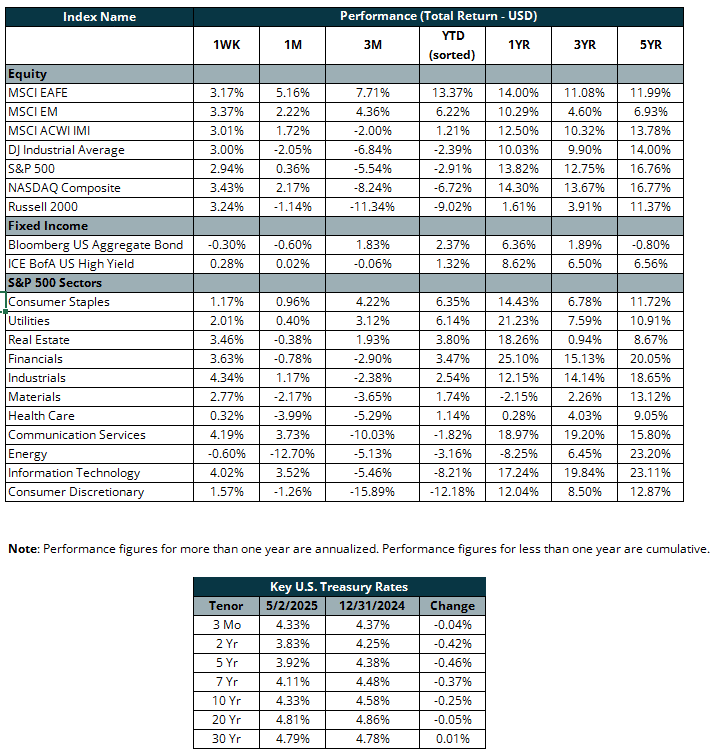

U.S. stocks rebounded sharply this week, with the S&P 500, Dow Jones Industrial Average, and Nasdaq all rising around 3%, marking their best performance in months and signaling a recovery from the early April selloff driven by trade tensions. The Dow gained 564 points, or 1.39%, the S&P 500 rose 1.47%, and the Nasdaq climbed 1.51%. The Dow and S&P 500 recorded their ninth consecutive daily gain, with the S&P achieving its longest winning streak since November 2004 and the Dow having its best weekly performance since December 2023.

Strong earnings from Microsoft and Meta fueled optimism in the tech sector, boosting investor confidence in Big Tech’s AI-driven strategies. Microsoft shares surged 7.6% on Thursday and 2.3% on Friday, while Meta rose 4.2% on Thursday and 4.3% on Friday. However, cautious outlooks from Apple and Amazon somewhat tempered the rally. Apple warned of a potential $900 million tariff-related impact in the second quarter, pushing its stock down 3.74% on Friday. Amazon reported solid first-quarter results but issued mixed full-year guidance, causing a slight dip in its shares.

With nearly three-quarters of earnings season complete, analysts raised their expectations. FactSet now projects S&P 500 companies will report first-quarter earnings growth of 12.8%, up from 7.0% two weeks ago.

Trade tensions between the U.S. and China appeared to ease, providing additional market support. China’s Commerce Ministry indicated it was evaluating U.S. proposals for trade talks, which raised hopes for a potential de-escalation of the tariff dispute. While no agreements were made, the willingness to engage in dialogue reduced fears of a trade war escalation. A Wall Street Journal report that China might address U.S. concerns over fentanyl exports further boosted investor sentiment.

Consumer confidence deteriorated in April, reflecting growing anxiety over the economy amid President Trump’s unpredictable trade policies. In April, consumer confidence dropped sharply, with the Conference Board’s index falling 7.9 points to 86—its lowest level since May 2020 and a steeper decline than economists anticipated. The Expectations Index, which reflects views on future economic conditions, plunged 12.5 points to 54.4, marking a 13-year low. The share of Americans expecting a recession in the next year surged to a two-year high, with many survey respondents citing Trump’s tariffs as a top concern.

U.S. consumer spending surged 0.7% in March, the largest increase since early 2023, as households likely bought goods ahead of expected price hikes from tariffs. At the same time, the U.S. economy contracted by 0.3% in the first quarter of 2025, marking its first decline since 2022. This slowdown was partly driven by a 41.3% surge in imports as businesses and consumers stockpiled goods ahead of higher costs.

This surge in spending coincided with the Federal Reserve’s preferred inflation gauge—the Personal Consumption Expenditures (PCE) Price Index—remaining unchanged in March, the smallest increase in ten months, following a 0.4% rise in each of the previous two months. Prices for goods fell 0.5% after a 0.2% increase in February, while prices for services rose 0.2%, easing from a 0.5% gain. Meanwhile, the core PCE Index, which excludes food and energy, also remained flat, defying expectations for a 0.1% increase. On an annual basis, the PCE rate slowed to 2.3%, its lowest in five months, while core PCE inflation eased to 2.6%.

Job growth exceeded expectations in April despite concerns about the potential impact of President Trump’s tariffs on U.S. trade partners. Nonfarm payrolls rose by a seasonally adjusted 177,000 for the month, slightly lower than the revised 185,000 in March but above the Dow Jones estimate of 133,000, according to the Bureau of Labor Statistics. The unemployment rate remained steady at 4.2%, which is in line with expectations and signals stability in the labor market. Average hourly earnings increased by just 0.2% for the month, falling short of the 0.3% forecast, while the annual growth rate of 3.8% was also 0.1 percentage point below expectations.

Treasury yields declined early in the week as investors anticipated potential rate cuts, with the two-year yield dropping to 3.56%, below the Fed’s effective funds rate of 4.33%. However, a stronger-than-expected April jobs report on Friday reversed that trend, signaling minimal labor market impact from new tariffs and pushing the 10-year yield to around 4.33%. The rise in yields reflected shifting expectations around Federal Reserve policy. It renewed confidence in the economy, partially unwinding the declines seen in prior week’s driven by tariff concerns and dovish Fed signals.

The U.S. Federal Reserve is widely expected to leave interest rates unchanged when it concludes its two-day meeting on Wednesday. However, investors still anticipate rate cuts—on Friday, interest rate futures markets showed that most investors expect at least three quarter-point cuts by year-end, according to CME Group’s FedWatch tool.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

Iran Stalks Strait of Hormuz Chokepoint, Stoking Inflation Concerns