Market Commentary

Trade Tensions Spark Pullback from Record Highs

by Sequoia Financial Group

by Sequoia Financial Group

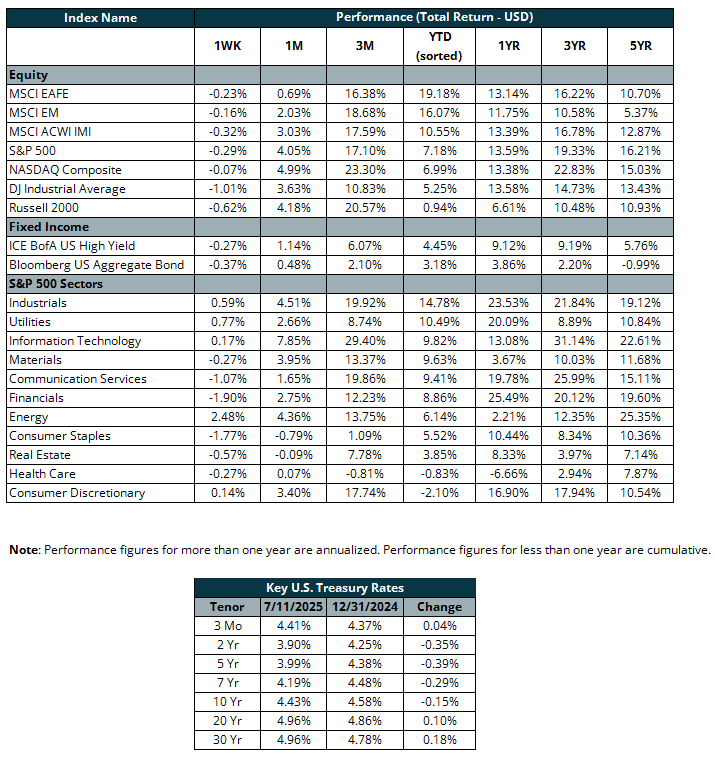

Last week was a volatile one for the U.S. stock market, as major indices hit record highs and then pulled back. The S&P 500 and the NASDAQ both posted slight declines after hitting all-time highs, following two weeks of strong gains that pushed the S&P 500 up by more than 5%. On Thursday, the S&P 500 rose 0.27% and the NASDAQ climbed 0.09%. However, on Friday, as futures suggested a possible decline, the S&P fell 0.3% and the NASDAQ slipped 0.22%.

Markets began the week on a strong note, buoyed by upbeat economic data and developments in global trade. Last week’s solid jobs report (147,000 vs. 110,000 expected) and a new U.S.-Vietnam trade agreement lifted investor sentiment. In a milestone for the tech sector, Nvidia became the first company to reach a $4 trillion market cap, highlighting the continued dominance of AI and technology as key drivers of equity performance.

However, market sentiment took a hit last week as renewed trade tensions resurfaced. President Trump threatened to impose a 35% tariff on Canadian imports and signaled that additional tariff hikes could follow for other major trading partners. Although investors initially viewed the rhetoric as part of broader negotiations, the administration’s decision to delay previously scheduled tariff increases from July 9 to August 1 suggested that talks remain in flux. The revised timeline also includes plans for higher tariffs on imports from countries like Canada and Brazil, while new threats targeting the EU and Mexico have further fueled uncertainty. These developments raised fresh concerns around inflation and corporate margins, pushing bond yields higher as markets priced in the risk of an escalating trade conflict.

U.S. government bond yields dropped on Wednesday after the release of minutes from the Federal Reserve’s latest meeting, which raised expectations for interest rate cuts later this year. However, yields climbed again on Friday as trade tensions intensified. By Friday afternoon, the 10-year U.S. Treasury yield had risen to around 4.42%, up from 4.35% at the close of the previous week.

As major U.S. banks gear up for the start of quarterly earnings season in mid-July, analysts are predicting a 4.8% average earnings growth for S&P 500 companies in the second quarter. If accurate, this would mark the slowest earnings growth since the fourth quarter of 2023, a sharp slowdown from the 13% growth seen in Q1.

Despite elevated tariffs, inflationary pressures remained largely stable through June. The May Consumer Price Index (CPI) report showed an annual rate of 2.4%, slightly above the four-year low of 2.3% recorded in April and in line with expectations. Looking ahead, investors will closely monitor the upcoming June CPI data and continue evaluating corporate earnings reports for insights into how companies are navigating the current economic environment. Evolving trade policies and their potential effects on inflation and corporate margins will remain central to market sentiment.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

AI Concerns Weigh on Stocks, but Iran Likely to Dominate News Flow