Strong Q1 Earnings, Cooling Inflation Boost Stocks Despite Uncertainties

by Sequoia Financial Group

by Sequoia Financial Group

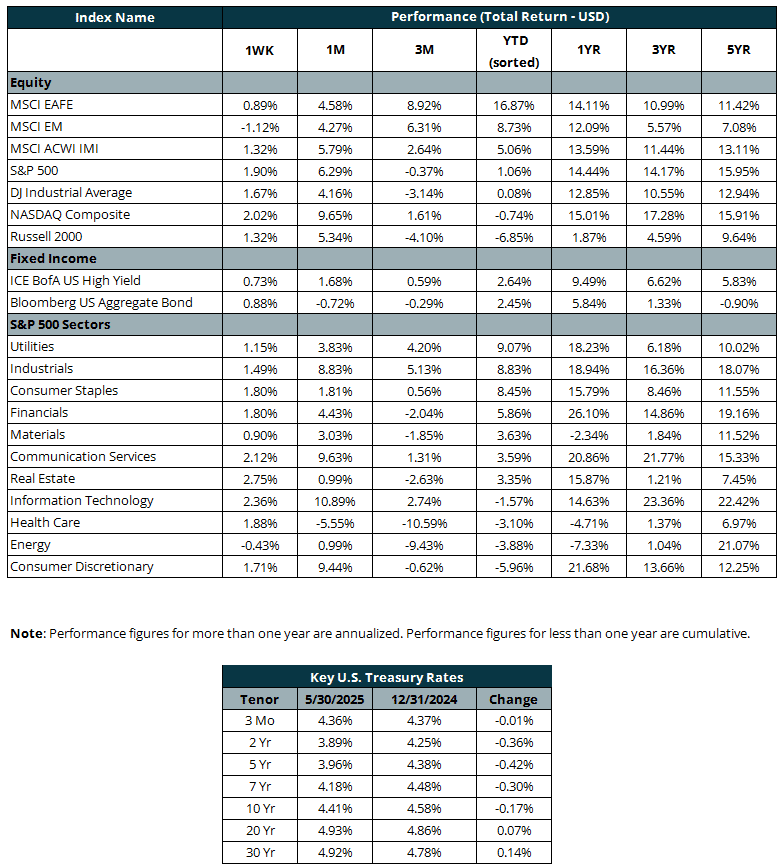

U.S. stocks ended May with solid gains, rebounding from the volatility of April and overcoming renewed trade tensions and shifting tariff policies. All three major indices rose about 2% this week, helping the S&P 500 notch a 6.2% monthly gain – its best May since 1990 – while the NASDAQ surged 9.6% and the Dow added 3.9%. Tech and AI-related names, notably Nvidia, fueled the rally, with the S&P 500’s Information Technology sector climbing more than 10%. Despite the strong May performance, the indices are little changed year to date after losses earlier in the spring.

Market optimism early in the week was driven by President Trump’s decision to delay a proposed 50% tariff on European Union imports until July 9, sparking a rally on Tuesday. However, sentiment turned choppy as legal battles over Trump’s broader “reciprocal” tariffs unfolded. A federal court initially blocked many of the tariffs, but an appeals court reversed that decision, leaving trade policy in a state of flux.

Adding to market volatility, the Trump administration signaled plans to tighten restrictions on Chinese tech firms. Bloomberg reported that the White House intends to expand export controls to cover subsidiaries of companies already on the U.S. Entity List, a move aimed at closing enforcement loopholes. Meanwhile, Treasury Secretary Scott Bessent described the U.S.-China trade talks as “stalled,” and President Trump publicly accused China of violating its preliminary trade agreement, raising fears of renewed escalation.

Despite geopolitical headwinds, equities found support in a strong batch of corporate earnings reports and encouraging inflation data. Technology stocks, particularly those tied to AI, led the charge, with Nvidia’s blowout results lifting sentiment across the sector. The company reported a 73% year-over-year increase in its data center business, which helped the NASDAQ to outperform. Elsewhere, results were mixed: Gap Inc. tumbled over 20% on tariff-related cost concerns, while Ulta Beauty and Costco posted gains of 11.8% and 3.1%, respectively, on strong quarterly performances.

April’s Personal Consumption Expenditures (PCE) data, the Federal Reserve’s preferred inflation gauge, showed signs of easing price pressures, offering modest relief to investors. Headline PCE rose 2.2% year over year, its lowest level since September. Core PCE, which excludes food and energy, increased 2.5%, down from 2.7% in March and in line with expectations. Markets interpreted the data as a gradual shift toward the Fed’s 2% inflation target, which helped support equities despite lingering concerns about the inflationary impact of higher tariffs.

However, the same report revealed a notable drop in consumer spending, which tempered optimism. Meanwhile, the University of Michigan’s final May reading on consumer sentiment edged up to 52.2 from the preliminary 50.8, matching April’s figure. While slightly improved, the index remains near a three-year low, reflecting persistent uncertainty among consumers. Together, the data painted a mixed picture: cooling inflation and somewhat better sentiment offered a tailwind for equities, but weaker spending kept gains in check.

The bond market also reflected rising investor anxiety. The bond market experienced sharp fluctuations this week as U.S. Treasury yields rose and then fell amid growing concerns over fiscal policy and government debt. The 30-year yield retreated to around 4.92% by week’s end, slipping back below the key 5% level after briefly reaching 5.09% – its highest point since 2023 – driven by weak auction demand and renewed concerns over President Trump’s tax and spending proposals. Shorter-term yields also declined, with the 10-year yield easing to 4.39% after climbing above 4.6% earlier in the week. Separately, JPMorgan CEO Jamie Dimon warned regulators of potential disruptions in the bond market, citing risks associated with proposed changes to banks’ supplementary leverage ratios.

Overall, markets managed to end May on a high note, with resilient earnings, cooling inflation, and AI-fueled tech strength offsetting renewed uncertainties in trade and fiscal policy.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Muted Inflation Report Pushes Stocks to New Heights