Strong Earnings, Mild Producer Inflation Help Stocks Build on Recent Gains

by Sequoia Financial Group

by Sequoia Financial Group

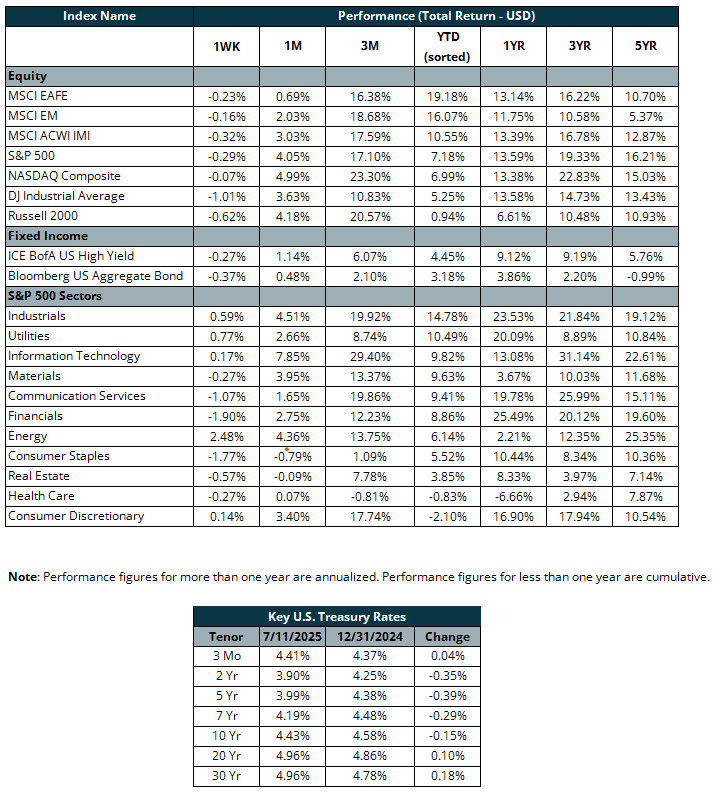

Second-quarter earnings season got off to a promising start last week thanks to solid reports from JPMorgan, Citigroup, and Goldman Sachs, among others. Expectations were high for the major banks, as merger & acquisition activity picked up throughout the quarter and interest rates remained steady. And stock market volatility, like we saw in April and May, can lead to big gains for trading desks. Those lofty expectations were largely met. JPMorgan’s investment banking revenue and trading revenue were both up eight percent. And in a positive sign for the health of the overall economy, JPMorgan’s loan loss provision was down slightly year over year. Citigroup showed similar strength, with earnings beating expectations by more than 20%, and past-due credit card payments down year over year. Meanwhile, Goldman profited from deal making and trading, with earnings per share jumping 26%.

Earnings shared top billing with consumer (CPI) and producer (PPI) price inflation reports. On Tuesday, CPI put the market on its heels by registering its highest level since January. The 2.7% headline number was in line with expectations, but the trend suggested that recent trade policy discussions out of Washington could start to affect prices. Food prices, for example, jumped three percent, with coffee and ground beef prices both up more than 10%. Thankfully, producer prices soothed inflation concerns Wednesday, as wholesale prices were stable compared to June. The tame PPI reading suggested that trade-related inflation might not be such a big factor after all.

And inflation doesn’t seem to be slowing consumer spending. Retail sales jumped more than expected in June, providing another positive read-through to the health of the economy. Spending grew across most sectors, with autos and clothing particularly strong. Stocks reacted favorably to the news, with the S&P 500 reaching a new closing record on Thursday. Bonds, on the other hand, sold off on the news. The 10-year Treasury yield crept back toward 4.5%, erasing early week gains.

Lingering in the background, however, were continued tariff concerns. Reports suggest that policymakers are pushing for higher tariffs on Europe than those previously announced. And other countries continue to push for reduced tariff rates ahead of an August 1 deadline. Some could also be holding out hope that a July 31 court hearing and the decision that follows could effectively block the tariffs. Of course, the administration may look for other avenues to implement its trade agenda. Either way, the tariff story isn’t going away. For now, earnings will continue to fill the headlines. This week, we’ll get reports from Coca-Cola, Verizon, General Motors, Tesla, and many more.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

")

Financial Markets Look Beyond the Government Shutdown