Stocks Rally on China Tariff Pause

by Sequoia Financial Group

by Sequoia Financial Group

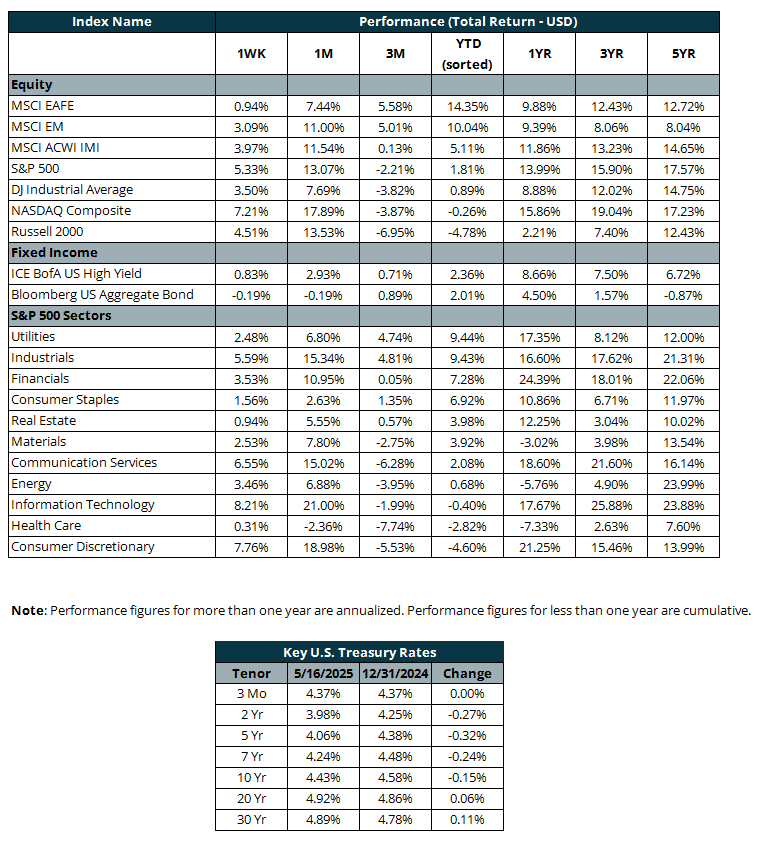

Last week started with a bang. Trade negotiations between the United States and China produced surprisingly positive results, with the US tariff on Chinese goods dropping to 30% from 145%, and the China tariff on US goods dropping to 10% from 125%.[1] The agreement cooled tensions that had stalled trade between the world’s two largest economies. Like other tariffs imposed by President Trump, the lower China tariff will remain in effect for 90 days, allowing negotiators some time to formalize a longer-term agreement. Investors cheered the de-escalation, with the S&P 500 rallying more than 3% and the NASDAQ surging more than 4% on Monday alone.

And the rally had legs thanks to lower recession odds and tame inflation reports. Stocks slid lower in early April on worries that tariffs could both slow the economy and push inflation higher. But now, multiple tariff pauses have economists dialing down their forecast odds of a recession. Indeed, Goldman Sachs trimmed its odds of a recession to 35% from 45%, citing trade optimism.[2] Meanwhile, inflation numbers continue to show stable prices for both consumers and producers. Tuesday brought the latest market-friendly Consumer Price Index (CPI) reading, with inflation ticking just 2.3% higher on a year-over-year basis for April. The inflation print came in a bit lower than the 2.4% expected.[3] The Producer Price Index (PPI) nearly mirrored those results, climbing 2.4% year over year in April, just below the 2.5% expected.[4]

Even an extremely negative Consumer Sentiment Survey from the University of Michigan couldn’t sour the market’s positive mood. The report showed consumers increasingly worried about the economy and inflation. Consumers expect inflation to jump to an eye-popping 7.3% over the next 12 months. That would bring inflation to its highest level since 1981. But the financial markets reflect much tamer inflation expectations[5], and even Federal Reserve Chairman Powell calls the U of M report an outlier regarding inflation. Still, the tone of the report was decidedly negative and the overall consumer sentiment index dropped to its lowest level since 2022, and its second-lowest level in nearly 75 years.[6] With the stock market rallying in recent weeks and trade tensions easing, we’ll be looking for improved sentiment in June.

Overall, it was a banner week for the stock market. The S&P 500 climbed 5.3% for the week, and now sits in positive territory (+1.9%) for the year to through May 16. We expect continued volatility through the summer months as trade deals get cobbled together and new tariffs rates are announced. But for now, we’ll enjoy the rally.

[1] Stock market news for May 12, 2025

[2] Brokerages Scale Back Recession Odds After U.S.-China Trade Truce

[3] CPI: Inflation rose 0.2% in April, 2.3% on the year; slightly below expectations

[4] Producer Price Index News Release summary – 2025 M04 Results

[5] 2-Year Expected Inflation (EXPINF2YR) | FRED | St. Louis Fed

[6] US consumer sentiment slides to 3-year lows as trade war raises inflation anxiety

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Your Financial Goals in 2026")

Plan")

")

")

")

Nvidia Earnings Fail to Quell AI Doubts