Stocks Rally on AI Momentum as Fed Cut Looms

by Sequoia Financial Group

by Sequoia Financial Group

U.S. equities delivered a milestone-filled week, with markets pushing to successive record highs before easing slightly into the close on Friday. Gains were steady through the early part of the week and accelerated on Thursday, when the Dow Jones surged 617 points to close above 46,000 for the first time. That move underscored the market’s resilience despite ongoing tariff concerns and signs of slower growth. The S&P 500 rose 0.85% and the NASDAQ gained 0.72%, leaving all three major indices at record highs. By Friday, momentum had eased, but the NASDAQ still capped a perfect week of record closes, rising with a 0.44% advance on strength in Tesla, while the S&P hovered near flat and the Dow slipped 0.59%. Even so, the weekly performance was strong across the board, with the S&P gaining 1.6% for its best showing since early August, the NASDAQ climbing 2% for a second straight week, and the Dow posting its first weekly increase in three.

Much of the rally was powered by technology leadership, particularly mega-cap names tied to AI. Oracle stood out after issuing upbeat cloud guidance, citing surging demand from AI clients. The stock jumped 36% in its steepest one-day rally since 1992. Adding to the positive momentum, the IPO market showed new signs of vitality, logging its busiest week in nearly four years as several high-profile deals raised billions of dollars.

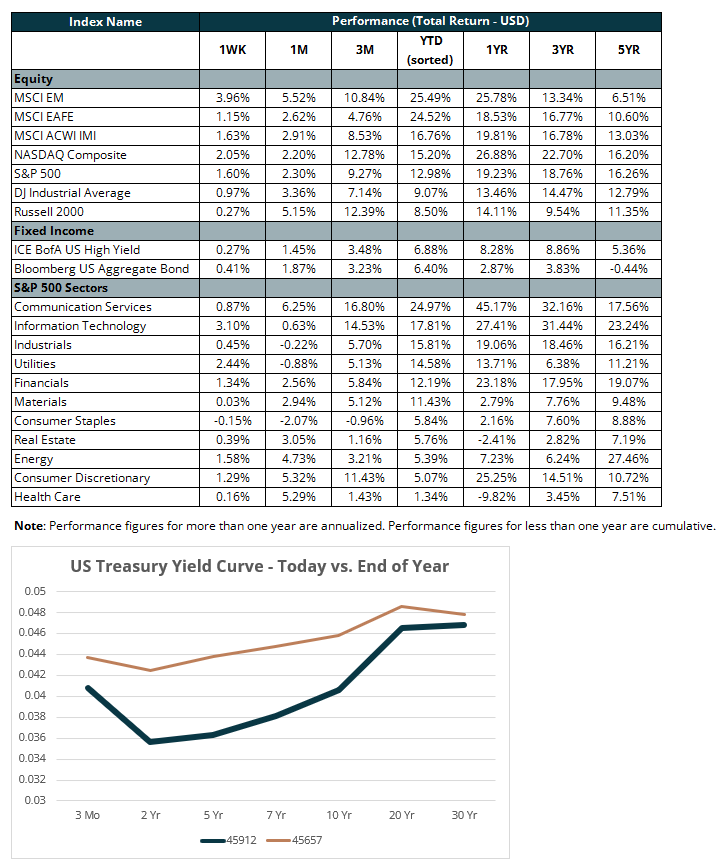

Bond markets also reflected shifting dynamics. Treasury yields swung sharply, with the 10-year briefly dipping below 4% on Thursday for the first time in more than five months before rebounding to finish near 4.06% by Friday. The 2-year ended at 3.56%, while the 30-year closed around 4.68%, highlighting investors’ back-and-forth positioning ahead of next week’s Fed decision.

Economic data, meanwhile, sent a more complicated signal. The August Consumer Price Index showed headline inflation rising 2.9% year over year, up from 2.7% in July, with a 0.4% monthly gain that exceeded expectations. Core inflation inched up to 3.1%, keeping price pressures above the Fed’s target but without signs of a sharp reacceleration. At the same time, labor market signals weakened. Jobless claims hit 263,000, the highest in nearly four years, while the Bureau of Labor Statistics revised down prior job gains by 911,000 between April 2024 and March 2025. Wage growth and private payrolls also showed little momentum, underscoring a softer employment backdrop. Adding another twist, the producer price index fell 0.1% in August, after a downwardly revised 0.7% increase in July and well off the Dow Jones estimate for a 0.3% rise. The release provides breathing room for the Federal Reserve to approve an interest rate cut at its meeting next week. Services prices, a key metric for the Fed when evaluating the stance of monetary policy, posted a 0.2% drop.

Consumer sentiment weakened notably in September, with the University of Michigan’s preliminary index falling to 55.4 from 58.2 in August, marking a four-month low. The survey also pointed to rising long-term inflation expectations, a development that could complicate the Federal Reserve’s policy decisions. Overall, Americans are becoming increasingly downbeat about the economy, as higher prices and worsening job prospects weigh on their sentiment. Compared to a year ago, the index has dropped by about 21%, underscoring the impact of tariffs and other economic headwinds on consumer sentiment.

Attention now shifts to the Federal Reserve’s September 17 policy meeting. As of Friday’s close, futures markets implied a 96.4% probability of a quarter-point rate cut and a 3.6% chance of a larger half-point move, according to CME FedWatch, underscoring market conviction that policymakers will ease next week.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Muted Inflation Report Pushes Stocks to New Heights