Stocks Extend Rally on Trade and Earnings Positives

by Sequoia Financial Group

by Sequoia Financial Group

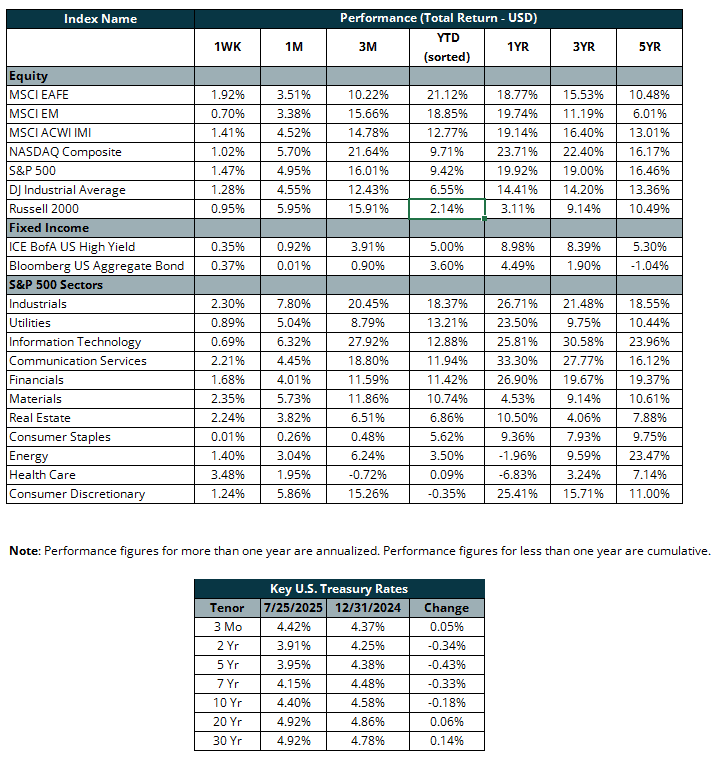

U.S. stocks hovered near all-time highs last week as cautious optimism grew that Washington could strike additional trade agreements, helping the economy avoid the impact of steep tariffs and maintain its momentum. The S&P 500 rose 1.5% for the week, its fifth straight record close and fourteenth of the year, marking the longest such streak in over a year. The NASDAQ also continued its ascent, ending the week up 1% after logging four record closes during the week. Meanwhile, the Dow Jones Industrial Average climbed 1.3% for the week, just shy of its all-time high in December.

Strong corporate earnings drove the market rally, as more than 80% of S&P 500 companies reporting so far have exceeded Wall Street expectations. The strong showing across sectors has lifted investor confidence and added to the market’s upward momentum. Alphabet and Verizon stood out, climbing 4% and 5% respectively after posting solid quarterly results. Alphabet also boosted sentiment by raising its capex outlook. In contrast, Tesla slipped after CEO Elon Musk warned of a few tough quarters ahead due to reduced EV incentives from a new tax bill. Intel also disappointed, dropping 8.5% after issuing weak guidance and announcing layoffs.

Volatility remained muted for most of July, with the Cboe Volatility Index (VIX) holding below its long-term median and touching a five-month low this week. That said, sudden spikes in names like Kohl’s and Opendoor, both heavily shorted, suggest a renewed burst of meme stock activity among retail investors. While market momentum has been strong, valuations appear stretched. The S&P 500 now trades at 22.6x forward earnings, well above its historical average of 15.8x, raising the risk of a pullback if results fall short of expectations.

In addition to strong earnings, recent trade agreements between the U.S. and key partners have contributed to the market’s continued climb. The President announced a trade deal with Japan late on Tuesday, which lifted U.S. equities as investors welcomed signs of easing global trade tensions. The agreement sets reciprocal 15% tariffs on Japanese imports, which is well below the previously threatened 25% and a positive surprise for the markets. While proposed tariffs remain a key source of uncertainty, the Japan deal fueled optimism that further trade agreements might be on the horizon and supporting broader market sentiment. U.S.-listed shares of Honda Motor (+11%) and Toyota (+13%) popped in pre-market trading after the President announced the deal.

Markets have been closely watching U.S. trade negotiations ahead of the August 1 deadline, when 30% tariffs on European Union imports would be set to take effect without a finalized deal. The President had warned there was only a “50-50 chance” at best of reaching an agreement in time. The U.S. had previously delayed similar tariffs in April due to market volatility, keeping the risk of escalation in focus. Despite the uncertainty, signs of progress emerged as European Commission President Ursula von der Leyen met with U.S. President in Scotland. Following their talks, both leaders announced that a trade deal had been reached, with the agreement imposing a 15% tariff on most European goods exported to the U.S., including cars. Although the exact scope and timing of the EU’s investments are still unclear, the agreement represents a significant breakthrough for the American administration after weeks of uncertainty over U.S.-EU trade negotiations.

In housing data released last week, both existing and new home sales fell short of expectations. Existing home sales dropped 2.7 percent in June to an annual rate of 3.93 million, while new home sales rose just 0.6 percent to 627,000 as high mortgage rates and elevated prices continued to pressure the market.

Looking ahead, attention will turn to this week’s Federal Reserve meeting, a key jobs report, and the busiest stretch of earnings season. More than 150 S&P 500 companies, including major tech companies such as Meta and Apple, are scheduled to report their results. The Fed is expected to hold rates steady when it concludes its policy meeting on Wednesday, while Friday’s jobs report will provide insight into July’s labor market performance following June’s stronger-than-expected gain of 147,000 jobs.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Your Financial Goals in 2026")

Plan")

")

")

")

Nvidia Earnings Fail to Quell AI Doubts