S&P 500 Snaps Six-Week Win Streak

by Sequoia Financial Group

by Sequoia Financial Group

Earnings season kicked into high gear last week, with 20% of the S&P 500 reporting. Expectations were raised after the strong showing by the banks, which generally beat income and revenue expectations. The positive earnings momentum continued, but interest rate concerns kept a lid on stock prices.

Tesla, coming off a disappointing robotaxi announcement two weeks ago that was long on hype and short on details, delivered an impressive quarter. Improved margins, strong volumes, and even stronger projections pushed the stock up 20%.[1] In fact, Elon Musk said volume growth could reach a stunning 20%-30% next year. Analyst expectations aren’t quite that lofty, but price targets were reset upward based on the optimistic announcement.

UPS also delivered a strong quarter. Margin forecasts improved, and profit and revenue both topped analyst expectations.[2] E-commerce providers Temu and Shein have driven package volume higher, but margins have been an ongoing concern. Progress on that front led to a more than 8% gain in the stock on Thursday, though it remains down more than 10% since the first of the year.

Coca-Cola’s report was less impressive, as volume dipped 1% in the third quarter.[3] However, the drop was smaller than Pepsi’s, which slipped 2%. Further, Coke CEO James Quincey said the revenue drop was temporary and that he expects the company will be back to volume growth in 2025. In other beverage news, Keurig Dr. Pepper purchased energy drink maker GHOST for nearly $1 billion, in its biggest acquisition to date.[4] Keurig’s stock dropped 5% following the announcement.

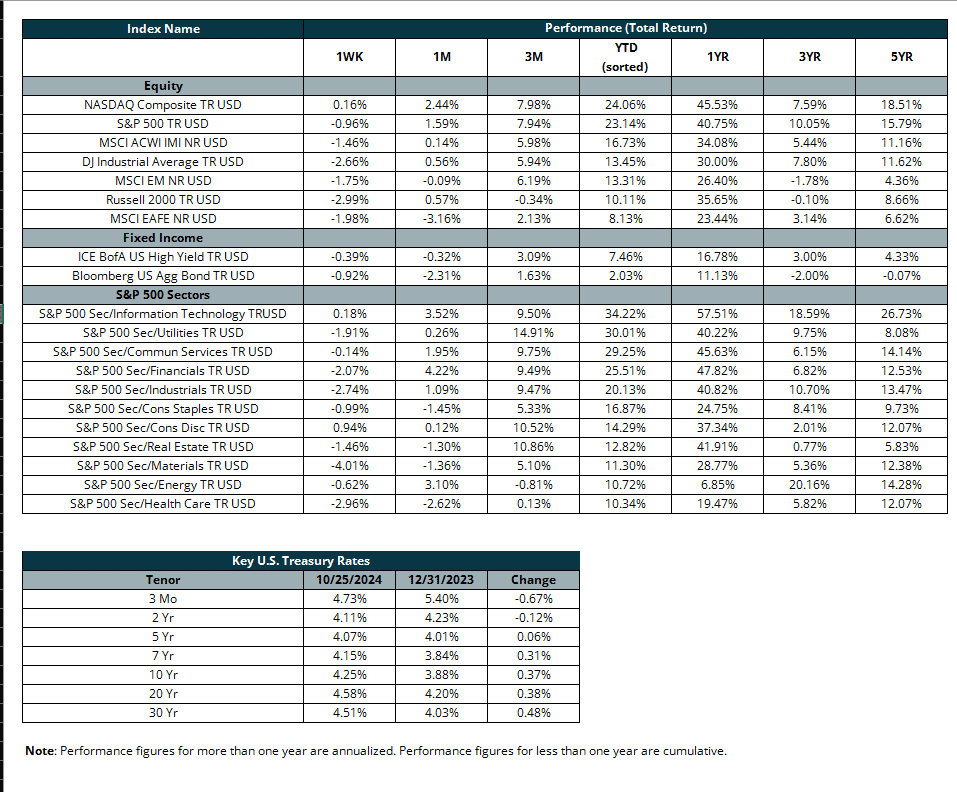

But while earnings season so far has been solid overall, interest rate concerns haven’t abated. Indeed, the 10-year Treasury yield briefly topped 4.25% last week before pulling back slightly to end the week at 4.23%. For comparison, the benchmark yield started the year at just 3.95%. Higher bond yields can hurt stock prices, as the added yield can shift demand from stocks to bonds. Higher yields could also signal more gradual rate cuts by the Federal Reserve. Overall, the bond market ended the week down about 1%.

The tech sector takes center stage this week, with reports due from Magnificent 7 members Alphabet, Microsoft, Amazon, Apple, and Meta. We’ll also get a new look at the Fed’s favored inflation measure – personal consumption expenditure inflation – and an estimate for third quarter GDP. Add in the upcoming election November 5, and we could see a possibly volatile start to November.

[1] https://www.cnbc.com/2024/10/23/stock-market-today-live-updates.html

[2] https://www.cnbc.com/2024/10/24/ups-q3-earnings.html

[3] https://www.foodbusinessnews.net/articles/27039-coca-cola-deals-with-volume-decrease

[4] https://keurigdrpepper.com/behind-the-scenes-of-the-ghost-acquisition/#:~:text=Today%2C%20Keurig%20Dr%20Pepper%20announced,every%20need%2C%20anytime%20and%20anywhere.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Q2 Market Review – Stocks Climb the Wall of Worry – Again