Q2 Market Review – Stocks Climb the Wall of Worry – Again

by Sequoia Financial Group

by Sequoia Financial Group

Stocks Climb the Wall of Worry—Again

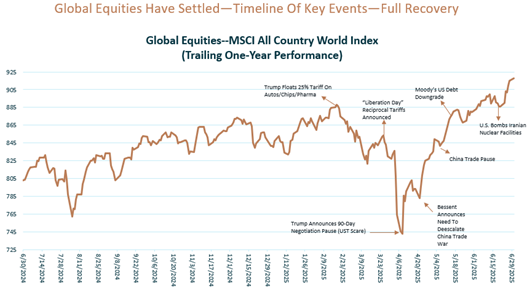

Amidst a cacophony of market noise and heightened uncertainty during the second quarter, global equities again demonstrated their resilience. Investors navigated choppy waters as concerns over global trade policy, U.S. fiscal budget challenges, and escalating geopolitical tensions led to a sharp drawdown in April. Yet, as the quarter unfolded, stocks rebounded and surged to new all-time highs—a testament to the market’s enduring ability to climb the proverbial wall of worry. As a historic and turbulent quarter comes to a close, U.S. stocks are reaching new highs, with many investors convinced the rally still has room to run. The sharp April downturn—which pushed the S&P 500 to the edge of a bear market—has been erased and surpassed, as the index has climbed more than 8% since President Trump’s sweeping tariffs first triggered market turmoil.

Each round of new tariffs or trade restrictions has been met with heightened volatility and investor anxiety, only to be followed, in some cases, by policy rollbacks or negotiated agreements that help restore confidence and spark renewed buying. This cycle of escalation and de-escalation has kept markets on edge. Still, it has also created opportunities for sharp recoveries as investors anticipate—and sometimes benefit from—trade and regulatory policy shifts.

Q2 2025 served as a textbook example of the perils of market timing and the critical importance of avoiding emotional responses to the daily news cycle. Those who succumbed to fear during April’s volatility and moved to cash likely found themselves watching from the sidelines as markets roared back to record levels. The quarter underscored a fundamental truth: while headlines may drive short-term sentiment, disciplined investing and maintaining perspective through market turbulence often prove far more rewarding than attempting to time the market’s every twist and turn.

Source: Bloomberg

Source: Bloomberg

This dramatic turnaround occurred in just over two months, with the VIX volatility index spiking to extreme levels during the April selloff before normalizing as markets regained their footing. While it’s undeniably difficult to buy when the VIX is elevated (as it doesn’t feel good to invest when fear is palpable), history consistently demonstrates that periods of elevated fear often provide some of the most attractive entry points into the market. For investors who panicked and sold during this period, the cost was severe—missing just the 10 best trading days over 20 years can cut returns nearly in half.

The Erosion of American Exceptionalism: Not So Fast!

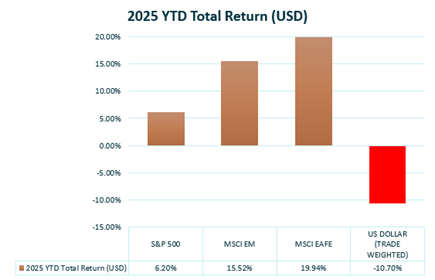

Over the past quarter, we’ve seen a significant change in how global investors view U.S. assets. The longstanding belief in “American Exceptionalism”—the notion that U.S. markets offer unparalleled safety and opportunity—has been seriously challenged. This shift was most clearly reflected in the 9% drop in the trade-weighted dollar during Q2, which underscored declining confidence in the U.S. economic outlook.

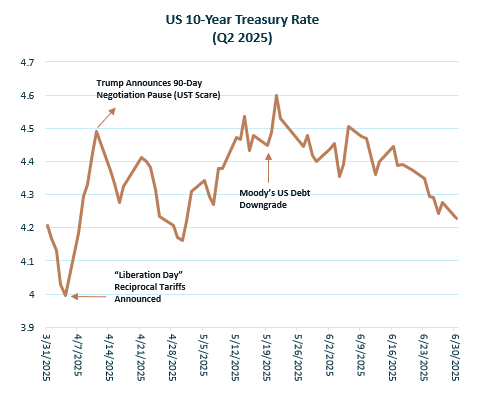

The catalyst for this change was the administration’s announcement of new, aggressive tariffs in early April. These measures introduced considerable uncertainty into U.S. economic policy and rattled markets. This time, the market’s reaction was unusual. Instead of the typical “flight to safety” into U.S. Treasuries during stock market turmoil, stocks and bonds sold off together. The 10-year Treasury yield jumped sharply from below 4% to over 4.5% in just a few days, signaling that investors were not only concerned about short-term volatility but also about the underlying fiscal health of the U.S.

Several other factors compounded this loss of confidence. The U.S. sovereign credit rating was downgraded, citing persistent deficits and a lack of fiscal discipline. Congress advanced legislation expected to add trillions to the national debt, further fueling concerns about long-term fiscal sustainability. Notably, Treasury yields continued to rise even as economic data softened, suggesting that investors demanded a higher risk premium to hold U.S. government debt.

The usual pattern of seeking safety in U.S. assets during global uncertainty broke down. Instead, investors began to hedge their U.S. exposures and shift capital to other markets. Over 70 countries reached out to U.S. officials to express concerns about the new trade policy, and global portfolios were rebalanced away from U.S. assets at a pace not seen in years.

Source: Bloomberg

Source: Bloomberg

It’s worth noting that it wasn’t just the stock market decline that triggered a policy response but the sharp and sustained rise in Treasury yields. This reaction from the bond market sent a clear message about the limits of investor patience with fiscal and policy uncertainty, prompting the administration to pause the most aggressive tariffs. More specifically, it’s unusual to see recession fears associated with international trade wars being met with a 50-basis-point increase in Treasury rates.

Source: Bloomberg

Source: Bloomberg

Looking ahead, this quarter’s events serve as a reminder that while the U.S. still benefits from deep capital markets and strong institutions, these strengths alone cannot guarantee its status as a safe haven. Global investors are becoming more discerning, and the U.S. must demonstrate sound policy and fiscal discipline to maintain its position as the world’s financial anchor.

That said, despite the recent pullback, reports of the dollar’s demise are premature. While the dollar’s global reserve currency status is not a divine right, with regime changes possible over extended periods, no other currency currently matches the dollar’s stability, liquidity, or global reach. The euro faces political and fiscal challenges, while China’s renminbi remains too tightly controlled. The U.S. economy’s size and the depth of its financial markets continue to make the dollar the preferred choice for central banks, investors, and international trade. With over 60% of global reserves and nearly 90% of currency transactions in dollars, its central role remains firmly intact.

Talk of U.S. economic leadership ending is overstated, particularly regarding U.S. equities. The country is still home to many of the world’s largest and most innovative technology companies, which continue to drive global growth and attract substantial investment. As the chart below illustrates, the recent quarter saw some of the heaviest net buying of Information Technology stocks ever recorded.

The main hesitation about investing in U.S. equities is driven by the uncertainty that President Trump’s policies are creating, particularly around the value and stability of the U.S. dollar. Over the last several years, many investment portfolios have steadily increased their U.S. holdings. Now, as U.S. markets show weaker performance compared to other regions, investors are adjusting their allocations accordingly. This trend is also evident in the market for U.S. Treasury securities. For global investors to regain confidence and return in significant numbers, the key factor is restoring dollar stability and overall economic certainty under the current administration.

AI and Productivity: This Innovation May Be Our Savior…

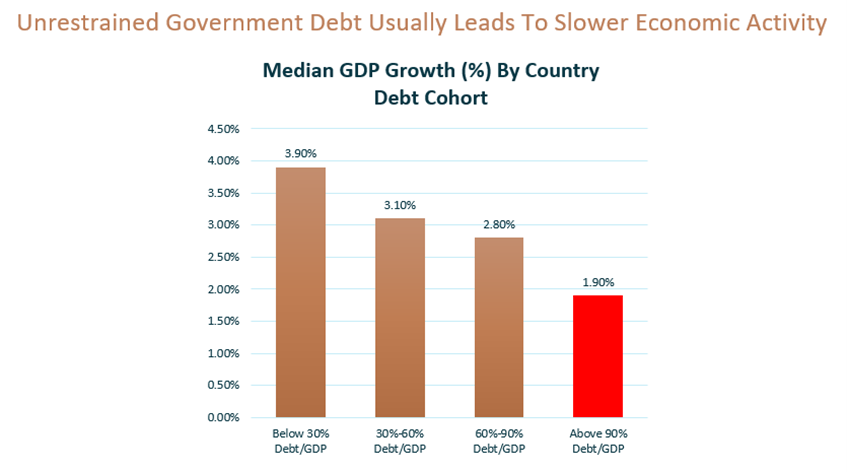

There are growing concerns about the long-term sustainability of U.S. economic growth, particularly as recent government spending has raised concerns about fiscal responsibility. The ongoing increase in national debt has not been met with much urgency or corrective action by policymakers in Washington.

As shown in the chart below, economic growth tends to slow significantly when government debt exceeds 90% of GDP. Slowing growth happens for a few reasons. When the government borrows heavily, it can increase interest rates, making it more expensive for businesses to borrow money for expansion and investment. This “crowding out” effect means less money is available for private sector growth, which is vital for innovation and economic progress. Furthermore, as more funds are used to pay interest on debt, fewer resources are available for essential public investments, such as infrastructure and education. Uncertainty about future tax increases or spending cuts can also make consumers and businesses more cautious about spending and investing.

Source: Bloomberg

Source: Bloomberg

However, there is reason for cautious optimism. Advances in artificial intelligence (AI) can potentially significantly boost productivity across the economy. Experts estimate that AI could add between 0.1% and 3.0% to annual productivity growth, depending on the pace and extent of adoption. Over time, these productivity gains could offset some of the growth-suppressing effects of high government debt by enabling more output with the same resources and raising living standards. While there is no guarantee that AI-driven productivity will fully counteract the challenges posed by our debt burden, it can offer a promising pathway to help sustain and accelerate long-term economic growth.

The pace of technological advancement has reached unprecedented levels, reshaping industries and redefining economic possibilities. Artificial intelligence (AI) stands at the forefront of this transformation, rapidly evolving from a promising concept to a powerful catalyst for change. As organizations navigate this swift progress, a key question emerges: can AI-driven productivity gains serve as a stabilizing force—or even a savior—for businesses in an increasingly complex landscape?

The surge in capital expenditures for AI infrastructure, with major companies investing hundreds of billions of dollars in data centers and AI technologies, underscores the immense scale of this transformation. Meanwhile, real-world AI is rapidly expanding across corporate America, with nearly 10% of the workforce utilizing AI daily, and broader adoption rates are climbing steadily.

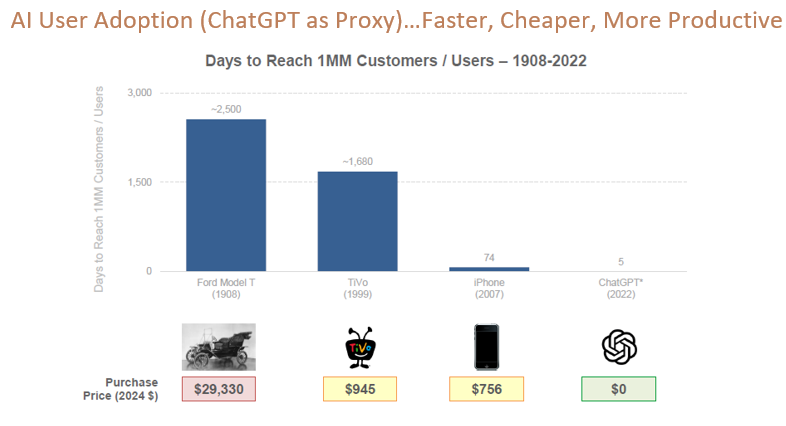

While real-world AI applications are still in their early stages, initial results are compelling. Organizations that integrate AI technologies report significant gains in efficiency and output. As adoption scales and AI systems become more sophisticated, the full impact on productivity can unfold over the next decade, suggesting that AI is not a fleeting trend but a foundational driver of long-term economic and operational transformation. The chart below highlights how quickly users are adopting AI technology compared to earlier examples of groundbreaking innovation—things are really moving at a remarkable speed!

Source: BOND

Source: BOND

Housing Market Dynamics Creating Multifamily Investment Opportunities

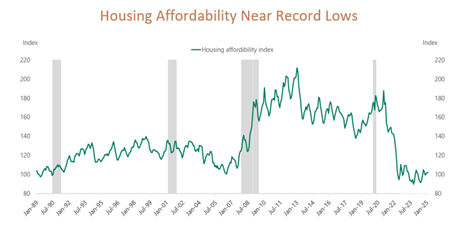

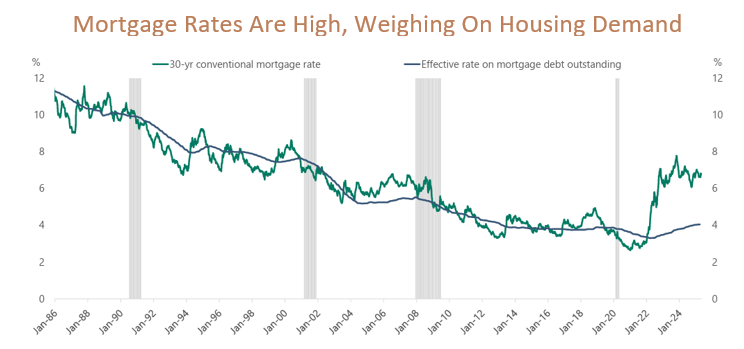

The current U.S. housing market faces significant challenges shaping buyer and seller behavior. Mortgage rates remain stubbornly high, hovering around 7%, while home prices continue to rise despite signs of softening in some regions. This combination has made homeownership increasingly unaffordable for many Americans, particularly first-time buyers. As a result, existing home sales have dropped to multi-year lows, with many would-be buyers choosing to stay on the sidelines until conditions improve.

Source: Apollo

While slightly improved from recent lows, inventory levels (above, right) remain well below what is needed for a balanced market. Many homeowners are reluctant to list their properties due to the “lock-in effect;” they are unwilling to trade their current low-rate mortgages for higher ones in today’s market. This has led to a shortage of available homes and elevated prices despite affordability constraints that suppress demand. Additionally, new construction has slowed, further limiting supply and making it difficult for the market to absorb pent-up demand.

Source: Apollo

Source: Apollo

These market dynamics are creating a confidence crisis among buyers and sellers. Buyers hesitate to commit to large purchases amid economic uncertainty and high costs. At the same time, sellers are wary of entering a market where homes may take longer to sell or require price reductions to attract interest. The situation is further complicated by policy uncertainty and the potential impact of new federal initiatives, which could influence supply and demand unpredictably.

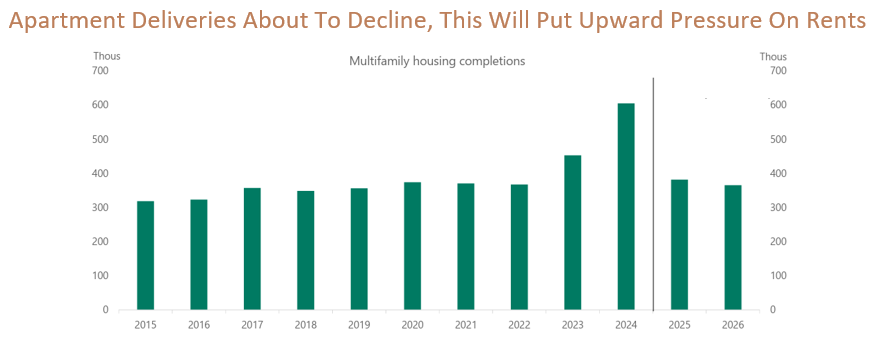

Despite these challenges, the current environment is generating notable opportunities in the multifamily rental sector. With homeownership increasingly unaffordable, more Americans are turning to rental housing, particularly in multifamily developments. This shift is driving strong demand for apartments, even as a record number of new units are coming online. While this influx of supply is expected to push vacancy rates higher and moderate rent growth, well-managed properties in markets with balanced supply and demand can still achieve stable returns.

Source: Apollo

Source: Apollo

Multifamily investments offer several advantages. They provide consistent cash flow, as income from multiple tenants helps offset the impact of individual vacancies. Economies of scale make property management more efficient, resulting in lower operational costs than single-family rentals. Tax benefits and the potential for long-term appreciation further enhance the appeal of multifamily properties.

Conclusion:

The second quarter of 2025 was marked by significant market volatility and uncertainty, driven by concerns over U.S. trade policy, rising government debt, and shifting global investor confidence. Early in the quarter, concerns about new tariffs and fiscal challenges led to a sharp selloff in both stocks and bonds, with the S&P 500 briefly approaching bear market territory and Treasury yields spiking as investors grew more cautious about the U.S. economic outlook. However, as has often happened, the market proved resilient—stocks not only recovered but surged to new all-time highs by the end of the quarter. This policy escalation and de-escalation cycle, where negotiations or rollbacks follow new tariffs or regulations, has kept investors on edge but also created opportunities for those who stayed invested and avoided emotional reactions to short-term headlines.

The U.S. dollar and Treasury securities’ traditional “safe haven” status were tested as global investors, unsettled by policy uncertainty and rising yields, began to reduce their U.S. exposure and seek alternatives. This shift was accelerated by a downgrade to the U.S. sovereign credit rating and ongoing concerns about fiscal discipline. Despite these challenges, the U.S. remains home to many of the world’s leading technology companies, which continue to drive innovation and attract investment. Recent data indicate that information technology stocks have experienced some of the strongest buying in years, reflecting continued confidence in the sector’s growth potential.

Looking ahead, the most significant risks to U.S. economic growth stem from high and rising government debt. This could slow growth by crowding out private investment, raising interest rates, and limiting the government’s ability to invest in crucial areas such as infrastructure and education. However, there are reasons for cautious optimism. Advances in artificial intelligence are transforming the economy, with companies investing heavily in AI infrastructure and nearly 10% of the workforce now utilizing AI tools daily. While the full impact of AI on productivity is still unfolding, early results suggest significant gains in efficiency and output, which could help offset some of the growth-suppressing effects of high debt.

In summary, while the U.S. faces real challenges from policy uncertainty, rising debt, and shifting global investor sentiment, its markets and economy remain fundamentally strong. The resilience of U.S. equities, the ongoing technological innovation, and the potential for AI-driven productivity gains all provide reasons for optimism. For investors, the key will be maintaining discipline, focusing on long-term fundamentals, and avoiding the temptation to react to short-term volatility. The U.S. is not immune to global trends or its policy missteps. Still, its deep capital markets, strong institutions, and capacity for innovation continue to set it apart, even as the world becomes more complex and interconnected.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Muted Inflation Report Pushes Stocks to New Heights