We are living through one of the most extraordinary periods in modern market history. The number of public companies available to investors has shrunk dramatically over the last three decades. At the same time, passive strategies have overtaken active management as the dominant force in global capital markets. Most recently, market returns have become concentrated in a handful of technology giants riding the wave of artificial intelligence.

These shifts have fundamentally altered the pursuit of “alpha,” which refers to investment returns in excess of the market index. Where once disciplined active managers in public markets could attempt to generate excess return, the structural realities of the market today make that task far more difficult. This raises the central question for long-term investors: where do durable opportunities still exist, and how should portfolios adapt?

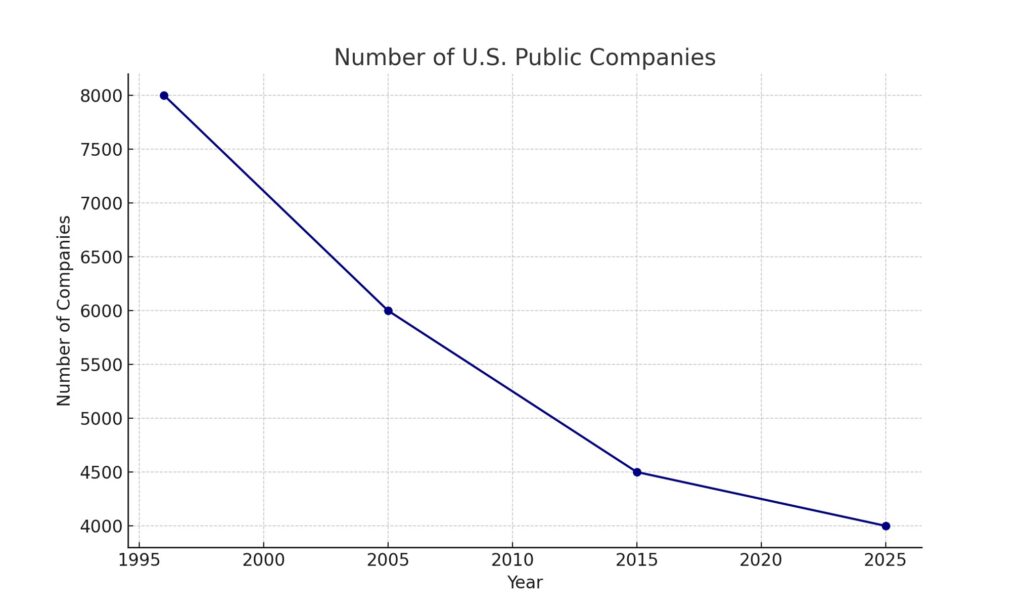

In the 1990s, there were more than 8,000 publicly listed companies in the United States. Today, there are fewer than 4,000. This phenomenon, often called “de-equitization,” is driven by rising regulatory costs, abundant private capital, and relentless M&A activity.

Source: World Bank, CRSP, S&P Capital IQ;

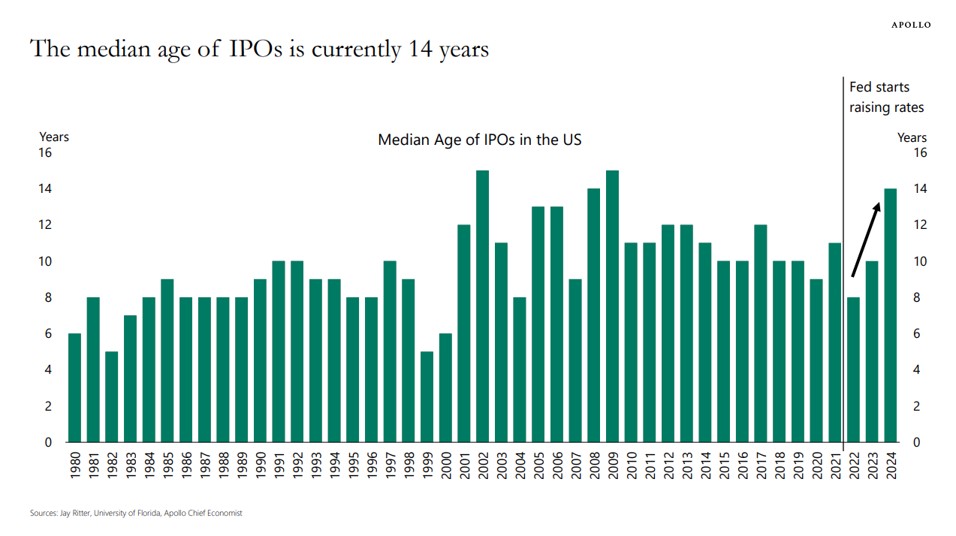

Not only are there fewer companies available, but those that do list are arriving much later in their corporate lifecycle. The average company now waits more than 14 years before going public, compared to just 8 years not long ago. In Europe, the median IPO age has risen to nearly 30 years. By the time investors gain access, much of the growth phase is already behind them.

Source: The Daily Spark 9/9/25 Torsten Slok Apollo

Why Go Public?

Recently, high-profile business leaders such as Larry Fink (CEO of BlackRock) and Jamie Dimon (CEO of JPMorgan Chase) have suggested that companies should report earnings semiannually rather than quarterly, a concept also floated by President Trump during his first term. For perspective, U.S. companies have reported quarterly results for over 50 years. Advocates argue that the regulatory burden, liability exposure, and pressure of quarterly guidance make private ownership far more attractive.

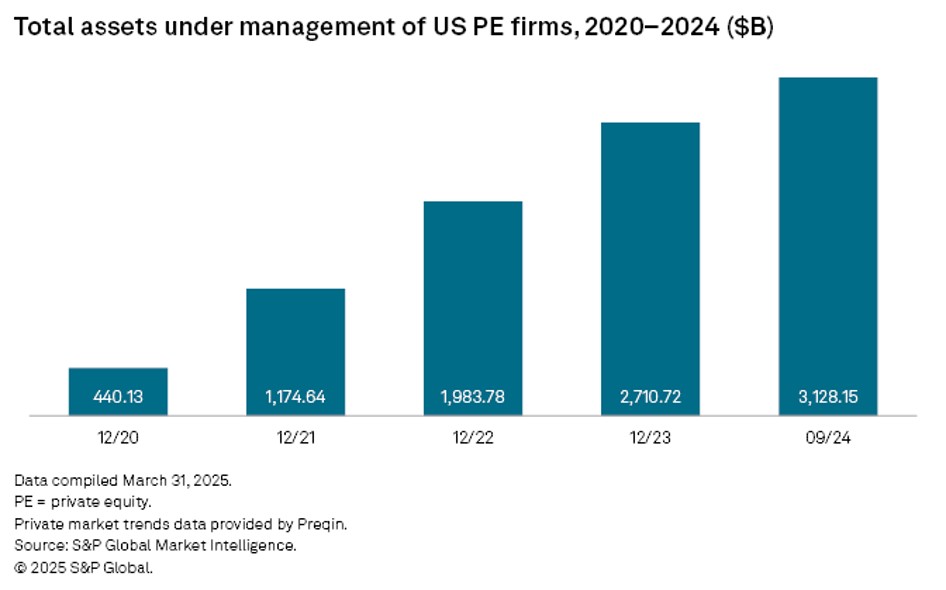

Meanwhile, private capital has evolved dramatically. The number of private equity firms has grown from roughly 500 to over 2,000, and assets under management have increased sixfold over the past 15 years. In March 2025, OpenAI raised $40 billion in the private markets, eclipsing Saudi Aramco’s record $25.6 billion IPO. Liquidity options have also expanded, with investors and employees increasingly able to sell stakes privately. Given this access to capital and flexibility, it’s worth asking: why would a company go public at all today?

The Rise of Passive and the Decline of Price Discovery

At the same time, the structure of public markets has transformed. Passive investing has become dominant. In 2024, U.S. passive mutual funds and ETFs surpassed active funds in total assets for the first time. More than $400 billion flowed into passive vehicles, while $300 billion was withdrawn from active strategies.

The advantages of passive investing—low fees, simplicity, and transparency—are undeniable. But they come with a cost. Passive strategies replicate index weights rather than analyze companies. As a result, price discovery weakens, and the challenge of generating outperformance in public equities grows even steeper.

The New Concentration Risk

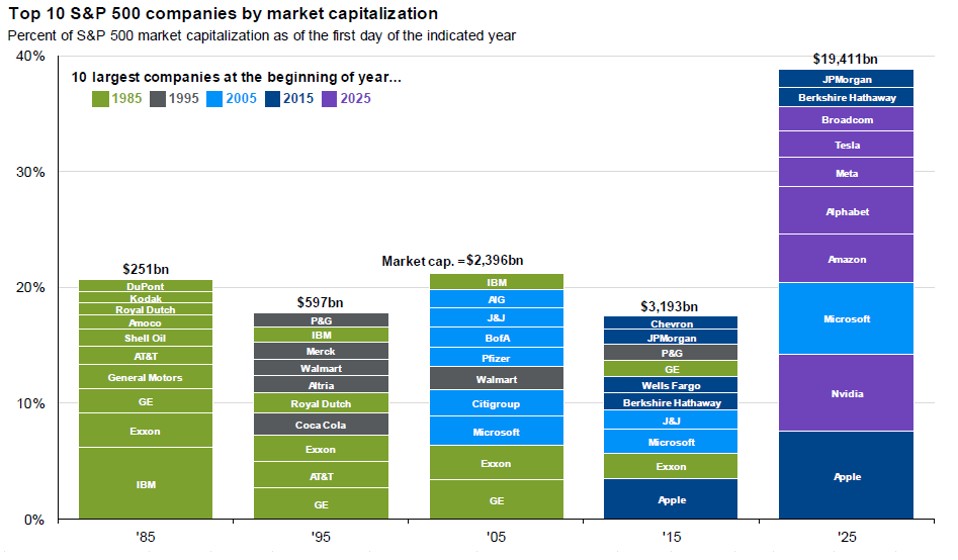

Perhaps the most striking feature of today’s market is its concentration. The “Magnificent Seven” (Apple, Microsoft, Amazon, Alphabet, Tesla, Meta, and Nvidia) now account for more than 30% of the S&P 500’s market capitalization.

Source: JP Morgan Asset Management, Standard and Poor’s

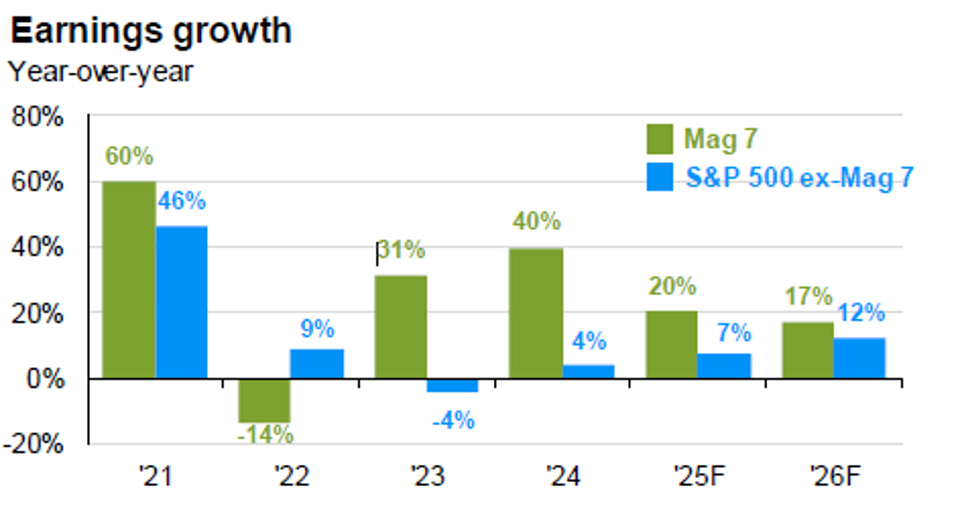

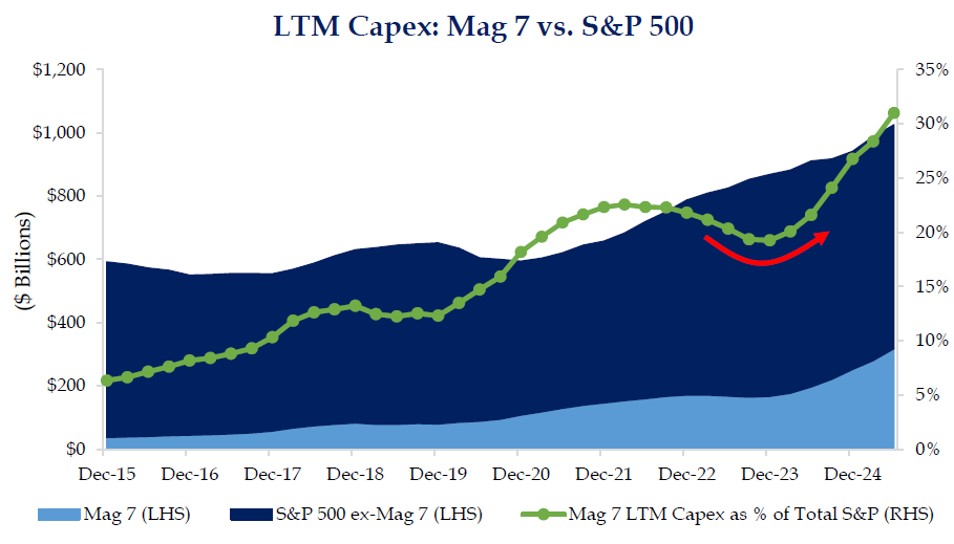

Recent research from Apollo shows that since January 2021, the top 10 companies have accounted for more than half of the S&P 500’s total returns. Earnings growth is concentrated almost entirely in the Magnificent Seven, while the rest of the index has shown little progress. These companies now represent over 30% of all S&P 500 capital expenditures, with hyperscalers alone comprising 7% of total U.S. private domestic investment.

Source: JP Morgan, Standard and Poor’s

Source: Strategas, FactSet

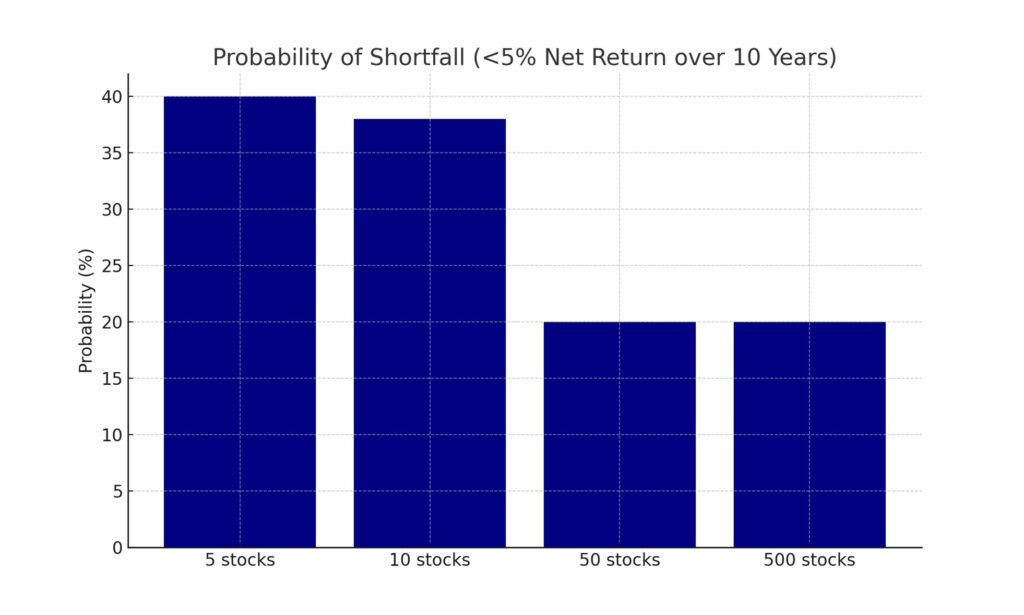

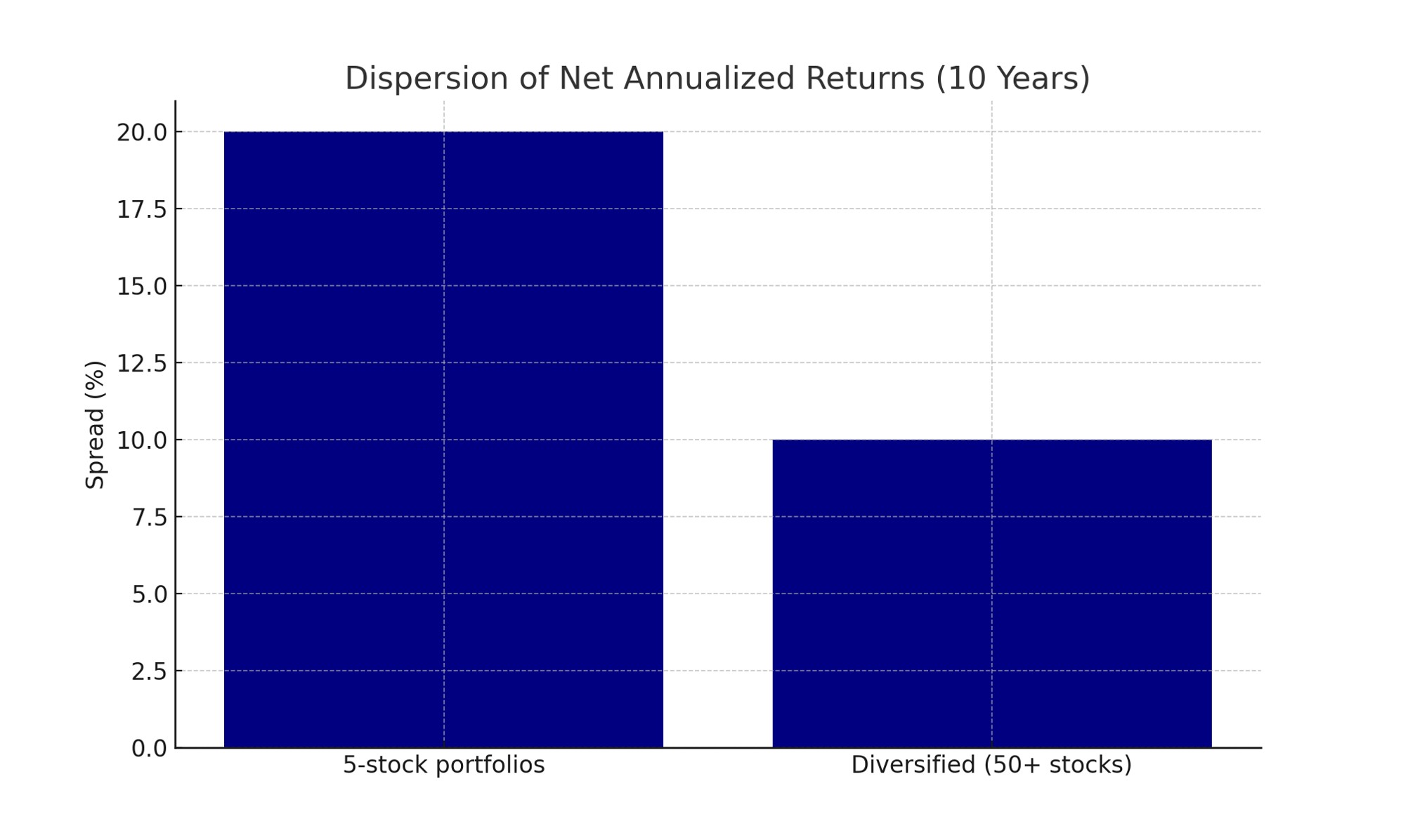

The structural evidence from Apollo is reinforced by decades of empirical research. Verdad Advisors, led by Brian Chingono, found that concentrated portfolios increase volatility drag, raise the chance of missing return targets, and amplify survivorship bias.

Source: Verdad Research simulations (1996–2023) using S&P Capital IQ data

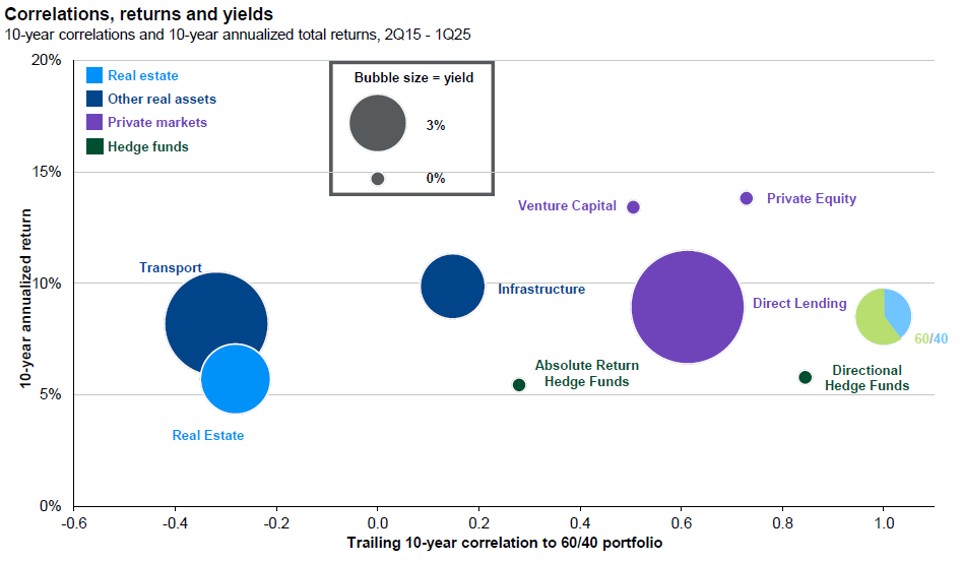

Where Alpha Lives Now: The Private Markets

These structural forces, shrinking public markets, passive dominance, and extreme concentration, make it increasingly difficult to find sustainable alpha in traditional public equities.

That doesn’t mean opportunity has disappeared; it has shifted. Private markets, including private equity, venture capital, and private credit, offer what active managers seek:

- Access to companies earlier in their growth cycle

- Less efficient markets where skilled managers can add value

- Lower correlation to public markets during volatility

Source: JPM Asset Management, Burgiss, Cliffwater, FactSet, PivitolPath

Private equity has always been a long game, but that too is evolving. Liquidity is coming to private markets. Tokenization, turning ownership stakes into tradable digital tokens, is enabling fractional ownership and secondary trading. Continuation vehicles, NAV loans, and secondary deals are giving investors new ways to unlock value without waiting for an IPO or acquisition.

All this means private equity is becoming less locked up, making it more appealing to investors seeking returns without a decade-long commitment.

Sentinel’s View

We believe the prudent course is to take advantage of both public and private markets while remaining faithful to our risk budget. Sentinel has been an active investor in private markets—both debt and equity—for many years.

Today, alpha potential remains abundant in private markets. Public markets, particularly the S&P 500, have become highly concentrated, adding risk to blind indexing. Alternatives to public equities remain compelling, and we expect to continue allocating capital accordingly. Our focus remains on rigorous manager selection, careful liquidity management, and bespoke portfolio design to ensure our families remain well-positioned for success.

Closing Reflection

The investment landscape is undergoing a profound transition. Real-time evidence shows unprecedented concentration in AI-driven mega caps. Long-term research confirms that hyper-concentration is not a recipe for sustainable returns. Taken together, these insights highlight a timeless truth:

“The virtue of diversification is proved by the costs of concentration.”

~ a foundational principle of modern portfolio theory

In an uncertain world, humility, broad diversification, and thoughtful exposure to private markets remain the most reliable path to enduring wealth.

We look forward to discussing these themes further and continuing our partnership.

Warm regards,

Your Sentinel Family Office Team

Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor.

Registration as an investment advisor does not imply a certain level of skill or training.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

AI Concerns Weigh on Stocks, but Iran Likely to Dominate News Flow