Market Commentary

Powell’s Speech Stokes the Markets

by Sequoia Financial Group

by Sequoia Financial Group

Markets ended the week on a strong note, with a powerful Friday rally reversing earlier losses and lifting the Dow Jones Industrial Average to its first record high of 2025. The Dow surged 846 points, or 1.9%, to close at 45,631.74, its highest level ever. The S&P 500 gained 1.5% to finish at 6,466.91, coming within a few points of its record intraday level, while the NASDAQ Composite advanced 1.9% to 21,496.53. For the week, the Dow rose 1.5%, the S&P 500 edged up 0.3%, and the NASDAQ slipped 0.6%.

The rebound was fueled by Federal Reserve Chair Jerome Powell’s remarks at Jackson Hole on Friday, where he struck a notably dovish tone. Powell suggested that recent signs of labor market cooling, combined with shifting risks around inflation, could justify a policy adjustment as soon as next month. He also highlighted the broader backdrop of changes in tax, trade, and immigration policy as factors the Fed is monitoring. His comments reset expectations in futures markets, where the probability of a quarter-point cut at the September 16-17 meeting climbed to about 83%, up from 75% earlier in the week.

Equities reacted swiftly. Mega-cap technology stocks, which had been under pressure earlier in the week, surged on Powell’s signal. Nvidia gained 1.7%, Meta rose more than 2%, Alphabet and Amazon each advanced over 3%, and Tesla rallied about 6%. The move helped erase much of the week’s earlier tech-driven weakness. Beyond Big Tech, value shares again led growth, with financials, energy, and homebuilders among the top performers.

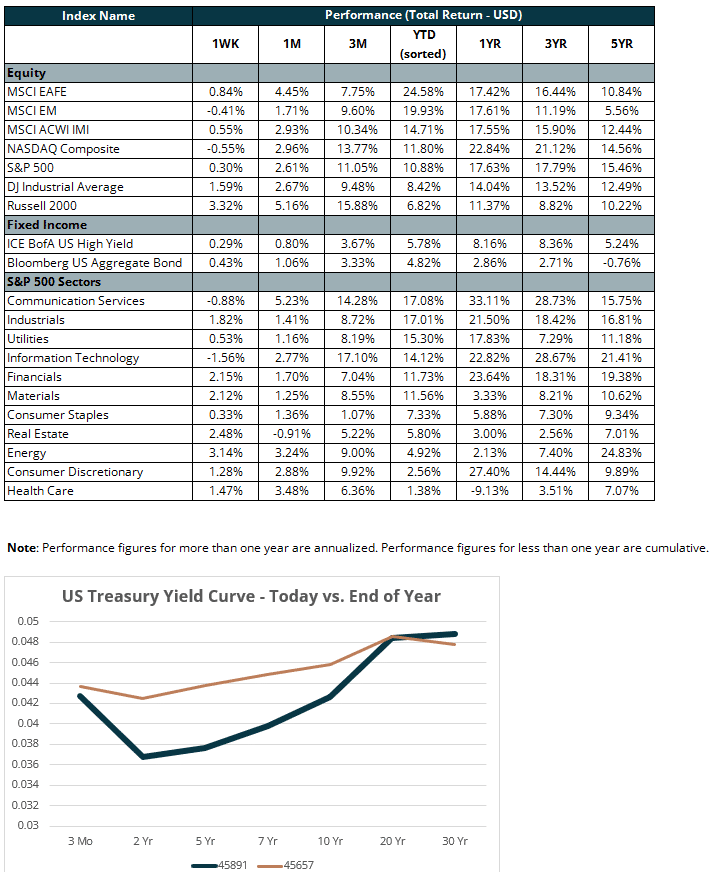

Rate-sensitive assets also rallied. Treasury yields declined across the curve, led by the two-year, which dropped to 3.69% from 3.79% a day earlier. The 10-year yield finished near 4.26%. The yield shift reflected growing conviction that the Fed is poised to pivot from restrictive policy toward easing.

Economic data added to the optimism. July existing home sales rose 2%, exceeding forecasts, as moderating mortgage rates lent some support. Housing starts increased 5.2%, their strongest pace in five months, though building permits fell to their lowest level since mid-2020. The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 2.5% on August 15, unchanged from August 7 after rounding. The outlook points to underlying consumer strength even as investment growth moderates.

Internationally, Canada said it would roll back a number of tariffs on U.S. goods, though duties on autos, steel, and aluminum remain. U.S. officials welcomed the partial de-escalation but emphasized that trade frictions are far from resolved.

Looking ahead, markets are fixated on two key events. The July PCE inflation report, set for release on August 29, will be closely watched for clues on the Fed’s next move, especially after June’s core reading climbed to 2.8%, the highest in four months. Nvidia’s upcoming earnings are another focal point, with investors eager to see if the AI rally is being matched by business results. At the same time, analysts are voicing concerns that lofty valuations could be outpacing fundamentals.

The events of last week underscored a market in transition: the Fed edging closer to easing, housing showing tentative stability, and inflation and AI sentiment likely to steer the next leg.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

")

Iran Stalks Strait of Hormuz Chokepoint, Stoking Inflation Concerns