Ongoing Fed-Driven Rally Pushes Stocks to New Heights

by Sequoia Financial Group

by Sequoia Financial Group

S&P 500 Poised to End Third Quarter Near Record Level

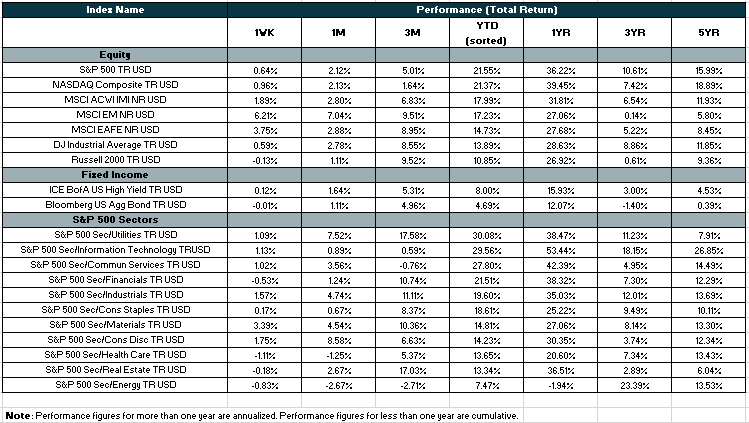

Stocks built on recent gains last week, with the S&P 500 and Dow Jones indexes both rising to record highs. The economy remained front and center, as investors looked for evidence that the Fed’s initial rate cut will help accomplish its dual goals of keeping inflation under control while promoting maximum employment. The rate cut was seen as a victory lap over inflation, but also a response to a weakening job market. Last week brought updated readings on both.

Stocks started the week strong despite a weak report on consumer confidence[1]. The drop in confidence from August to September was the biggest drop in three years and reflected job-market and inflation concerns. However, strong showings from Nvidia and Caterpillar, along with a new China stimulus program, helped the S&P 500 and Dow Jones Industrial Average to close at record levels.

And a strong employment report Thursday put some labor market concerns to rest[2], at least for the moment. Jobless claims ticked lower and signaled that the Fed was not playing catch up with its initial rate cut. Durable goods orders also firmed up, despite expectations that they would decline in August. Finally, we got the last of three second quarter GDP readings, showing GDP rose at an annualized rate of 3% in Q2. Looking ahead, the Atlanta Fed GDPNow model projects similar growth for the third quarter[3], which ended yesterday.

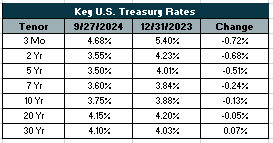

The latest inflation report also calmed some fears. The Fed’s favored inflation reading (PCE inflation) rose just 2.2% over the last 12 months[4]. Expectations were for a slightly higher 2.3% increase. The annual reading was the lowest for PCE inflation since February 2021. Further, personal income and personal spending ticked slightly higher, indicating a healthy consumer overall. And the reports support the argument for future rate cuts, as the Fed looks to keep the economy on track heading in 2025. The market is pricing in a rate cut at the Fed’s next meeting in November, but is split on whether the cut will be a quarter point or half point[5]. Stocks head into October on a three-week winning streak.

Sources:

[1] https://www.cnbc.com/2024/09/23/stock-market-today-live-updates.html

[2] https://www.cnbc.com/2024/09/25/stock-market-today-live-updates.html

[3] https://www.atlantafed.org/cqer/research/gdpnow

[4] https://www.cnbc.com/2024/09/26/stock-market-today-live-updates.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Equity Markets Reach Records After Mid-East Tensions Ease