Market Commentary

Nvidia Earnings Fail to Quell AI Doubts

by Sequoia Financial Group

by Sequoia Financial Group

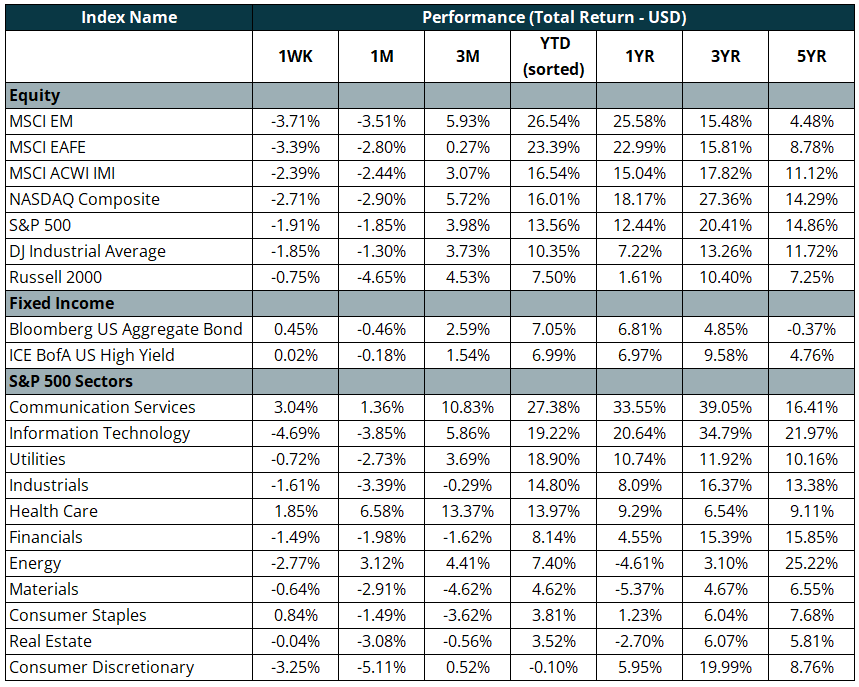

When Nvidia (ticker: NVDA) reported earnings after Wednesday’s close, it appeared that concerns about an AI bubble had been well and truly squashed. Nvidia beat both earnings and revenue expectations, and CEO Jensen Huang extolled that sales were “off the charts.” Indeed, the company grew earnings 62 per cent year over year. When the market opened on Thursday, NVDA and the S&P 500 were up five per cent and 1.5 per cent, respectively. Sentiment quickly shifted mid-morning, however, when investors dove deeper into the company’s financial statements. One notable concern was customer concentration: over the nine months ending October 2025, more than one-third of Nvidia’s data center revenue came from only two customers. Last year, a similar percentage came from three customers.

NVDA finished Thursday down more than three per cent and ended the week down six per cent. The sell-off affected many other tech stocks. AI darling Palantir (ticker: PLTR), which trades at an astonishing 161x forward earnings, was down 11 per cent for the week. NVDA and PLTR are still well into positive territory this year, up 33 per cent and 105 per cent, respectively. The S&P 500 closed the week down two per cent but has still returned more than 12 per cent this year.

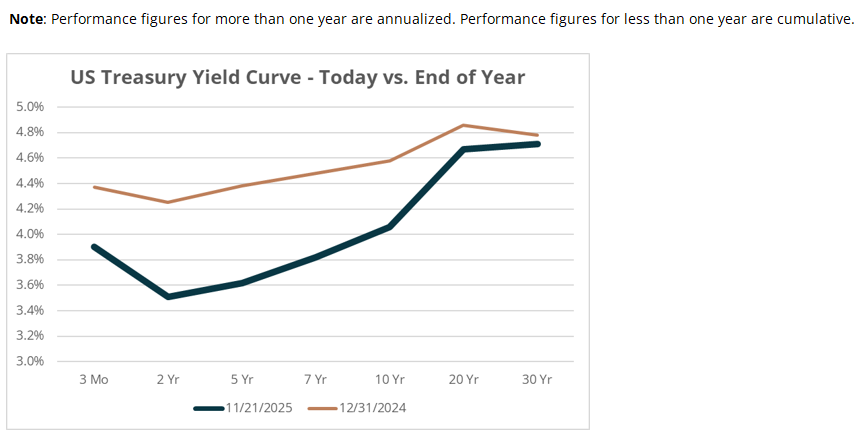

Last week’s volatility emphasized the importance of holding a diversified portfolio. The 10-year US Treasury yield decreased to 4.06 per cent from 4.14 per cent, as investors rotated into safe haven assets. As a result, both investment-grade and high-yield bonds saw gains. Real Estate Investment Trusts (REITs), which are rate-sensitive, also generated positive returns.

Despite the tech sell-off, investors could find returns elsewhere in US equities. The iShares US Healthcare ETF (ticker: IYH) and the iShares US Consumer Staples ETF (ticker: IYK) returned 1.9 per cent and 1.1 per cent, respectively. Stocks within these sectors tend to be relatively isolated from economic downturns. IYH’s largest constituent, Eli Lilly (ticker: LLY), made headlines this week when it became the first healthcare company to achieve a $1 trillion valuation. Lilly’s weight-loss injection Zepbound and diabetes treatment Mounjaro have led to the company’s dominant 58 per cent share of the GLP-1 antagonist space. The company’s dominance could position it well when GLP-1s for weight loss transition to oral delivery, which is expected in 2026.

Now that the US government is open again, the Bureau of Labor Statistics released a delayed September jobs report on Thursday. Added jobs of 119,000 were much higher than the 50,000 expected. The economic resilience seen in that print might have been enough reason for the Fed to hold rates steady, if it were not for the conflicting unemployment reading. The unemployment rate ticked up to 4.4 per cent, the highest reading over the past four years. The path of interest rates is even more uncertain, given the October report will not be released because of a lack of data collection during the shutdown. September’s labor report will be the last before the FOMC meets on December 9-10.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

AI Concerns Weigh on Stocks, but Iran Likely to Dominate News Flow