Micron Technology Earnings Breathe New Life into the AI Trade

by Sequoia Financial Group

by Sequoia Financial Group

Micron Technologies (MU) rose 10% last week, after the company markedly beat Q1 FY26 revenue and earnings expectations. The company is a key player in memory and storage products for many technology sectors, including AI data centers. AI models rely on vast amounts of data during training and inference (processing of trained models). Being able to quickly query such data sets is a critical part of a model’s user experience. MU’s stock price has more than tripled during the 2025 year-to-date. Micron’s strong earnings seem to have kicked the AI bubble can down the road, for now.

Before Micron’s earnings, equity markets started the week on edge. Certain tech companies, such as Meta Platforms (META) and CoreWeave (CRWV), have taken on debt to fuel their immense AI capital expenditure plans. CoreWeave is an intermediary that buys high-performance chips, the computing power of which the company rents to other companies training AI models. For every $1 of EBITDA (a profit measure), CoreWeave carries more than $4 in net debt (debt minus cash). CRWV’s 4x ratio is significantly higher than 1.3x for the overall S&P 500. The combination of high debt and insufficient future returns on capex have potential for unwanted ripple effects.

Momentum from Micron’s earnings buoyed softness in the labor market. Investors received long-awaited economic data on Tuesday, when the BLS released November unemployment and October and November jobs data. Unemployment came in at 4.6%, worse than the 4.5% economists expected. While the economy lost 105,000 jobs in October, it gained 64,000 jobs in November, ahead of the 45,000 expected additions. On top of the relatively soft jobs data, hourly earnings grew 3.5% year-over-year, which was the lowest growth in several years.

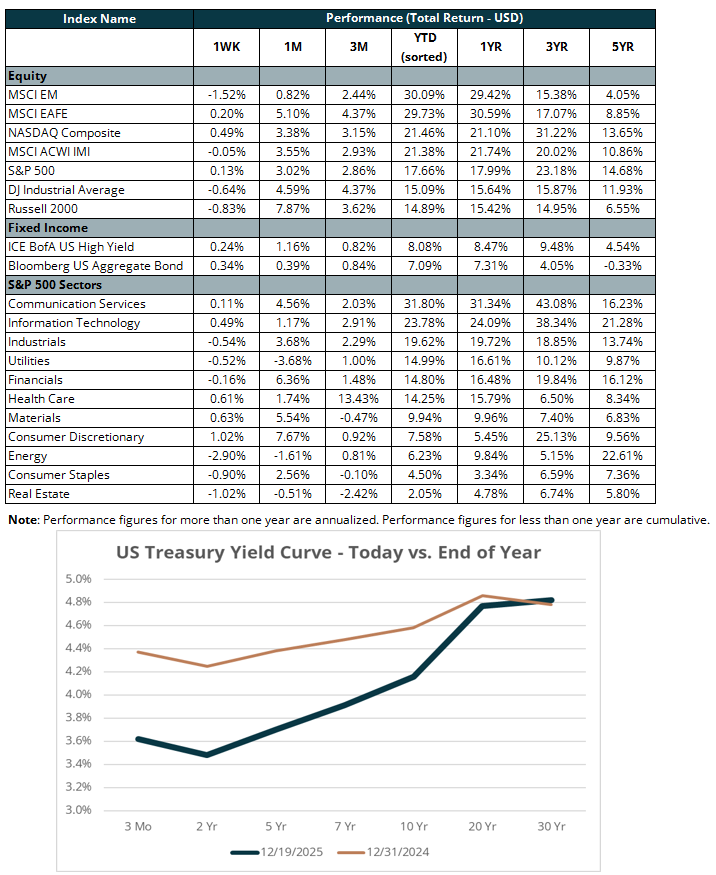

Turning to other side of the Fed’s dual mandate, the Bureau of Labor Statistics (BLS) reported Consumer Price Index (CPI) on Thursday. When taken at face value, November inflation appeared to have made the Fed’s decision easy to cut rates in January. Headline inflation increased 2.7% y/y in November, down from 3.0% in September and lower than the 3.1% expected. Despite the favorable reading, economists warned that the recent government shutdown had distorted the data. Gaps in data collection and the lack of a month-month comparison made it hard for investors to assess the reading’s relevance. Indeed, the bond markets barely budged last week.

With only a handful of trading days left in the year, the S&P 500 is on pace for three consecutive years of double digit returns. The index has returned >23% annualized returns over the trailing 3 years, much higher than the 11% annualized returns over the past 20 years. High recent returns and US stock valuations suggest subdued returns going forward. Many smart investors have tried but failed at timing past markets, however. Even those that have successfully called downturns haven’t shown consistency in deciding when to get back in.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

")

Your Financial Goals in 2026")

Plan")

What the 2025 Law Changes Mean for Investors and Founders")

Micron Technology Earnings Breathe New Life into the AI Trade