Markets Boosted by Favorable Inflation and Labor Data

by Sequoia Financial Group

by Sequoia Financial Group

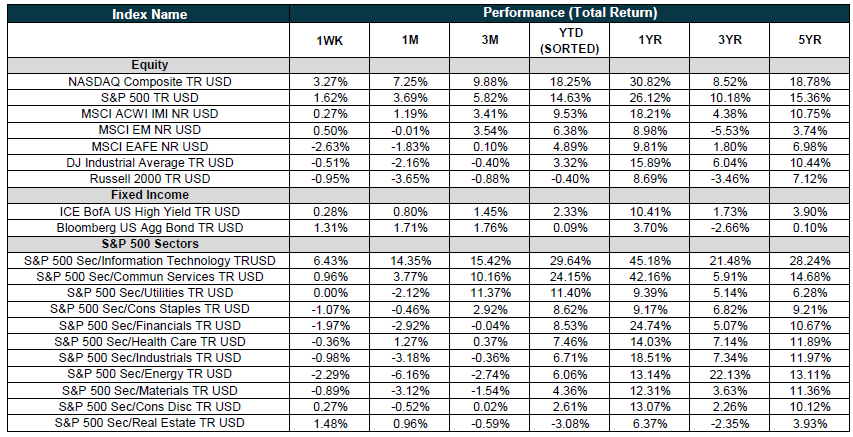

Strong economic data and renewed optimism for an interest rate cut by the Federal Reserve drove most major equity indices higher last week. The technology-heavy NASDAQ Composite Index advanced 3.27% to new highs, while the S&P 500 posted an increase of 1.62%. Meanwhile the Dow Jones Industrial Average declined 0.51%.1

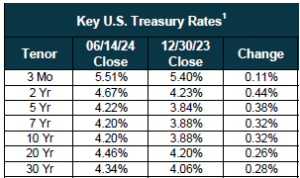

Similarly, fixed income markets posted strong returns this week as yields shifted lower on positive market sentiment across the US Treasury curve. The US 10-year Treasury bond fell 23bps, closing on Friday at 4.22%.2 The Bloomberg US Aggregate Bond Index advanced 1.31% on the week.

The rise in equities was primarily driven by the Technology sector, after several companies updated the financial markets on the potential benefits they expect to derive from the implementation of artificial intelligence (AI) within their organizations. Apple announced its long-awaited push into AI by introducing a range of new features, including an overhaul of its voice assistant Siri, integration with OpenAI’s ChatGPT and more writing assistance tools. However, it is likely that users will have to upgrade their phones to access these features, possibly resulting in a replacement cycle.3 Similarly, Adobe stated its “highly differentiated approach to AI and innovative product delivery are attracting an expanding universe of customers and providing more value to existing users.”4 Meanwhile, Broadcom shares rose after the company posted second fiscal quarter earnings that beat analysts’ estimates and showed that it is benefiting from the artificial intelligence boom.5 For the week, these stocks rose 7%, 12% and 23%, respectively.

During the week, the release of numerous economic data points concerning inflation and unemployment were viewed positively by market participants. The Bureau of Labor Statistics reported on Wednesday that the Consumer Price Index (CPI) was unchanged in May, surprising the market which had forecast a 0.1% increase, after rising 0.3 percent in April. Over the last 12 months, the Index has increased 3.3%. The core CPI (which excludes food and energy) also came in better than expected. The shelter component continues to disappoint, however, rising for a fourth consecutive month.6

Further supporting the positive trend of lower inflation, Thursday saw the release of the Producer Price Index, a measure of inflation at the wholesale level, which slipped 0.2% in May, lower than economists’ expectations of a 0.1% uptick and April’s 0.5% rise. The May decrease in final demand prices can be attributed to a 0.8-percent decline in the index for final demand goods.7

The markets also welcomed the news of some softening in the labor market. Initial claims for unemployment insurance jumped to 242,000 in the previous week, the highest level since August 2023.8

On Wednesday, the Federal Reserve opted to hold interest rates steady at 5.25-5.50% for a thirteenth consecutive month. While this was somewhat expected, the updated Summary of Economic Projections (SEP), which reflects the collective views of the voting members, now indicates that the members expect only one interest cut this year, significantly lower than the three cuts in the prior SEP, owing to the lack of progress in reducing inflation to their target rate.9

Given the events of the week, expectations for an easing of monetary policy by the Federal Reserve gained momentum. Using data from the CME Group’s FedWatch Tool, the likelihood of a cut in the Federal Funds rate at the September meeting rose to 67%.10

Sources:

- Morningstar Direct

- https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202406

- https://www.cnbc.com/2024/06/11/apple-shares-pop-to-record-high-after-company-unveils-ai-software.html

- https://www.cnbc.com/2024/06/14/adobe-shares-surge-and-head-for-sharpest-rally-since-2020-.html

- https://www.cnbc.com/2024/06/13/broadcom-stock-up-13percent-on-earnings-beat-increased-demand-for-ai-chips.html

- https://www.bls.gov/news.release/pdf/cpi.pdf

- https://www.bls.gov/news.release/pdf/ppi.pdf

- https://www.dol.gov/ui/data.pdf

- https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20240612.htm

- https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

President Trump Signs the ‘One Big Beautiful Bill’ into Law