Insights

Making Intrafamily Loans in an Era of Higher Mortgage Rates

by Sequoia Financial Group

by Sequoia Financial Group

As mortgage rates remain elevated, some families are exploring alternative ways to support younger members pursuing homeownership. One option to consider is an intrafamily loan, a private lending arrangement between family members that, when properly structured, can offer flexibility and support long-term financial planning goals.

How do intrafamily loans work?

In short, an intrafamily loan replaces a traditional lender with a family member. Typically, we see a matriarch or patriarch loan money from one generation to the next. While this is commonly done for a real estate purchase, it can also be for other reasons, such as starting a new business. Proper intrafamily notes are structured much like a traditional lending arrangement, with formal agreements around items such as:

- Amount: How much is being loaned?

- Term: What is the length of the note?

- Payments: How are payments made? Are payments interest-only or principal and interest?

- Interest Rate: What is the applicable rate?

To reduce gift tax concerns, the interest rate should be at least the Applicable Federal Rate (AFR). The AFR is published monthly and provides the minimum interest rate the IRS deems appropriate for the term of the loan to reduce gift tax concerns. As payments are made, the lender reports taxable interest income. Families should work with legal counsel to draft the promissory note outlining the terms of the arrangement. If drafted and recorded properly, an intrafamily mortgage loan may allow the borrower to deduct their interest costs, as is common with a typical mortgage loan. It is important to also work closely with a tax advisor.

Advantages of Intrafamily Loans

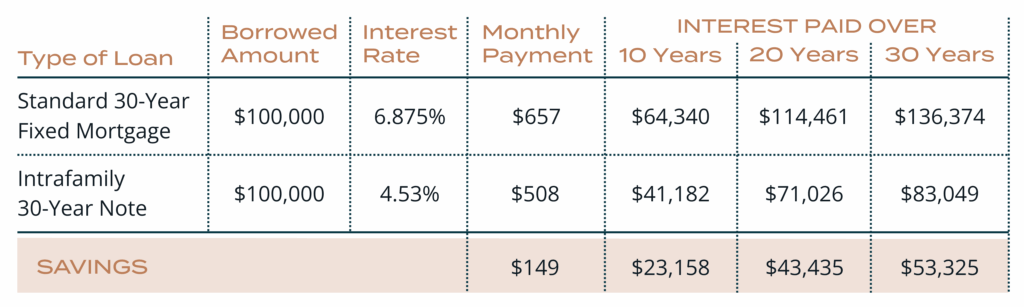

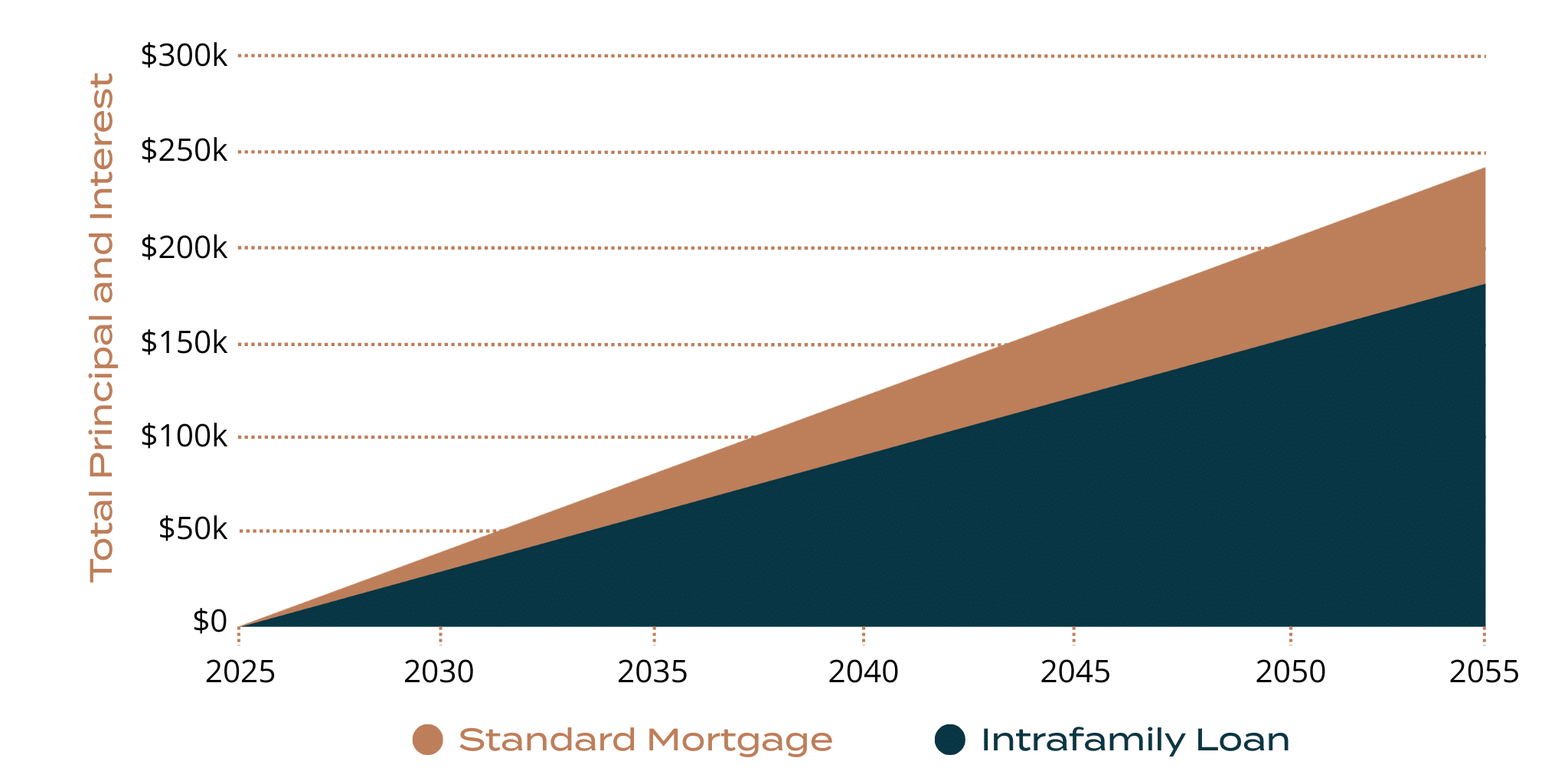

The primary advantage of this tool is to lower the interest rate for family members in need of funds. These savings can be significant over the life of the loan. In the example shown in the chart, a borrower with an intrafamily loan at the current AFR would save $23,000 over the first 10 years.

Savings for Intrafamily Borrowers

Table is for illustrative purposes only. Data sources: Standard fixed interest rate for Ohio, May 2025. Applicable Federal Rates for May 2025. Amortization calculator.

Table is for illustrative purposes only.

These types of loans can also support estate planning and family gifting strategies. Some families may consider using annual exclusion gifts (up to $19,000 per recipient in 2025, unchanged for 2026) to reduce the principal balance owed by the borrower to the lender. The annual exclusion represents the amount one individual may gift to another each year without triggering federal gift or income tax consequences.

Intrafamily Loans Are Not Without Risk

While making an intrafamily loan is a generous way to smooth the path for a family member, there are important considerations to take into account. Legal concerns can arise if the IRS reviews the terms of the loan and deems it as a gift. For this reason, it is important to work with legal counsel to draft the note.

The borrowers should be credit-worthy and have the means to repay the loan, just as would be required for a conventional mortgage. Additionally, the risk of the IRS deeming the loan a gift is reduced by collecting payments on the note and reporting the interest income on the lender’s income tax return. In short, treat the loan as a loan.

The lending family member should keep in mind how they will fund the loan. There may be tax implications associated with creating the funds to make the loan. Additionally, there will be ongoing tax costs related to the interest income.

Family Communication is Key

One additional consideration is family dynamics. These types of arrangements may create strife between family members. It’s important for the parties involved to discuss if, when, and how the details of a loan arrangement are disclosed among the family. Families should also consider what the ramifications and impact may be if the borrower is unable or unwilling to repay the loan.

With careful planning, an intrafamily loan can be a powerful tool to leverage resources for the benefit of the entire family. If this may be of interest to you, your Sequoia team is here to help you think through the nuances and create an optimal plan.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.The tax and estate planning information offered by the advisor is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Clients requesting tax return or estate preparation services are referred to a commonly-held affiliate, Sequoia Tax Services or a 3rd party and not Sequoia Financial Group.

")

")

AI Concerns Weigh on Stocks, but Iran Likely to Dominate News Flow