Market Commentary

US Equities Hit New All-time Highs in First Full Week of 2026 Trading

by Sequoia Financial Group

by Sequoia Financial Group

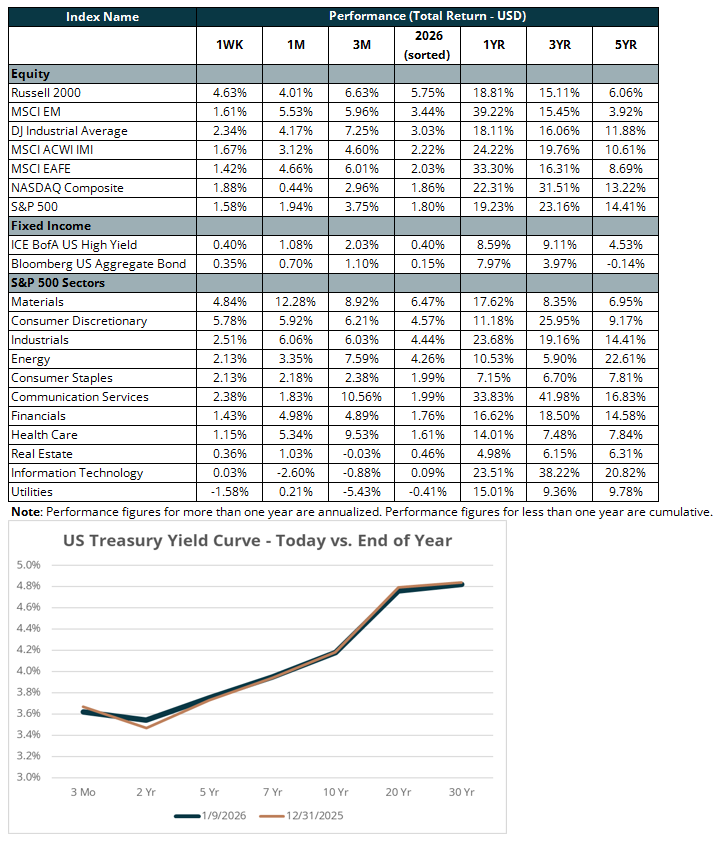

U.S. equities moved higher in the first full week of 2026. The Dow Jones Industrial Average, S&P 500, and Russell 2000 all finished the week at record levels, reflecting a continuation of the positive momentum that closed out last year. The S&P 500, an index of the largest U.S.-based companies, gained 1.6 per cent. Small caps fared even better, as the Russell 2000 surged 4.6 per cent. Markets appeared comfortable looking through near-term uncertainty, supported by expectations for stable U.S. economic growth and healthy corporate earnings in 2026.

The markets have also remained largely unfazed by the busy geopolitical backdrop. Much of the news focus has centered on developments in Venezuela following the U.S. capture of President Nicolás Maduro. President Trump stated that the U.S. would temporarily oversee the country’s transition and sell sanctioned Venezuelan oil at market prices, while pledging $100 billion of investment from the U.S. oil industry. Despite this pledge, Exxon (XOM) CEO called Venezuela “uninvestable” in its current state due to aging infrastructure and other challenges. Chevron (CVX), the last major U.S. oil company operating in Venezuela, ended the week down 1.1 per cent. While the situation remains fluid, broader market reaction was muted, as oil markets continued to be driven more by expectations of oversupply in 2026 than by near-term geopolitical risk.

Economic data released last week pointed to a labor market that is weakening gradually but remains intact. The December ADP National Employment Report came in below expectations, reinforcing signs that hiring momentum has slowed. This was followed by the December nonfarm payrolls report, which showed modest job growth with downward revisions to prior months, while the unemployment rate edged lower to 4.4 per cent. The data suggests employers are pulling back on hiring but are not engaging in widespread layoffs, consistent with what economists have described as a “low hire, low fire” environment. We note that initial jobless claims – the most timely labor market report, which tracks new applications for unemployment benefits – remained relatively low. This supports the view that labor market conditions are softening but are not rapidly deteriorating.

Looking ahead, investors are turning their attention to the start of fourth-quarter earnings season next week for insight into corporate fundamentals entering 2026. According to FactSet, consensus estimates call for roughly eight per cent earnings growth for the S&P 500 in the fourth quarter. Markets will also be watching for a potential U.S. Supreme Court ruling related to the administration’s tariff authority under the International Emergency Economic Powers Act (IEEPA), which could have major implications for trade policy.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Rising Oil Prices, Inflation Expectations Send Stocks and Bonds to 2026 Lows