Market Commentary

Stocks End Choppy Week Near Highs Amid Policy and Earnings Crosscurrents

by Sequoia Financial Group

by Sequoia Financial Group

U.S. stocks finished a volatile week with mixed performance, extending a second consecutive week of modest declines for major indices. Despite the pullback, markets remain close to record levels. The S&P 500 and Dow Jones Industrial Average are still within about one percent of their mid-January highs. The NASDAQ sits roughly two percent below its prior peak. Friday’s session reflected broader uncertainty: the S&P 500 was essentially flat, the Dow down about 0.6 percent, and the NASDAQ up roughly 0.3 percent. Small caps underperformed, with the Russell 2000 falling nearly two percent on the day. Losses for the week were contained: the S&P 500 was down 0.4 percent, the Dow off 0.5 percent, the NASDAQ lower by 0.1 percent, and the Russell 2000 down 0.3 percent.

Beneath the surface, the markets experienced sharp swings driven largely by political developments. Early in the week, major indices fell roughly two percent as tensions escalated around U.S. policy toward Greenland and renewed tariff threats against Europe, triggering a broad risk-off move. However, sentiment improved later in the week after President Trump dialed back tariff rhetoric and pointed to progress on a potential framework agreement involving Greenland. This helped equities recover much of their losses. Altogether, the rebound underscored how sensitive markets remain to geopolitical signals, especially when policy threats are followed by partial reversals after financial conditions tighten.

Earnings added another layer to an already volatile backdrop. As the second week of quarterly reports progressed, expectations for fourth-quarter S&P 500 earnings edged modestly higher, with analysts now forecasting roughly 8.2 percent year-over-year growth, up slightly from estimates at the start of earnings season. However, results at the company level continued to drive dispersion, most notably at Intel, where weaker-than-expected first-quarter guidance revived concerns around its turnaround. The company posted a quarterly loss and cited challenges in meeting demand for AI-related server chips, sending shares sharply lower. Beyond earnings, sentiment found some support from incremental progress on U.S.-China technology issues, including a finalized arrangement allowing TikTok to continue operating in the U.S. with Oracle and partners, as well as reports that Chinese authorities are allowing domestic tech firms to begin planning orders for Nvidia’s H200 chips despite ongoing import restrictions.

Inflation data released late in 2025 showed price pressures remain somewhat elevated compared to the Federal Reserve’s long-term target, even as economic growth proved stronger than previously expected. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, rose 0.2 percent in November. This left the annual rate at 2.8 percent, unchanged from the prior reading and still above the Fed’s two percent goal. Core inflation, which excludes food and energy, also increased 0.2 percent for a fifth consecutive month. This highlights the persistence of underlying price pressures. The October and November figures were released together, as agencies address delays tied to the recent government shutdown. The results were in line with consensus expectations. At the same time, revised data showed the U.S. economy entered late 2025 with solid momentum. Third-quarter GDP growth was revised higher to a 4.4 percent annualized pace, the strongest in two years. Growth was supported by the fastest increase in consumer spending this year.

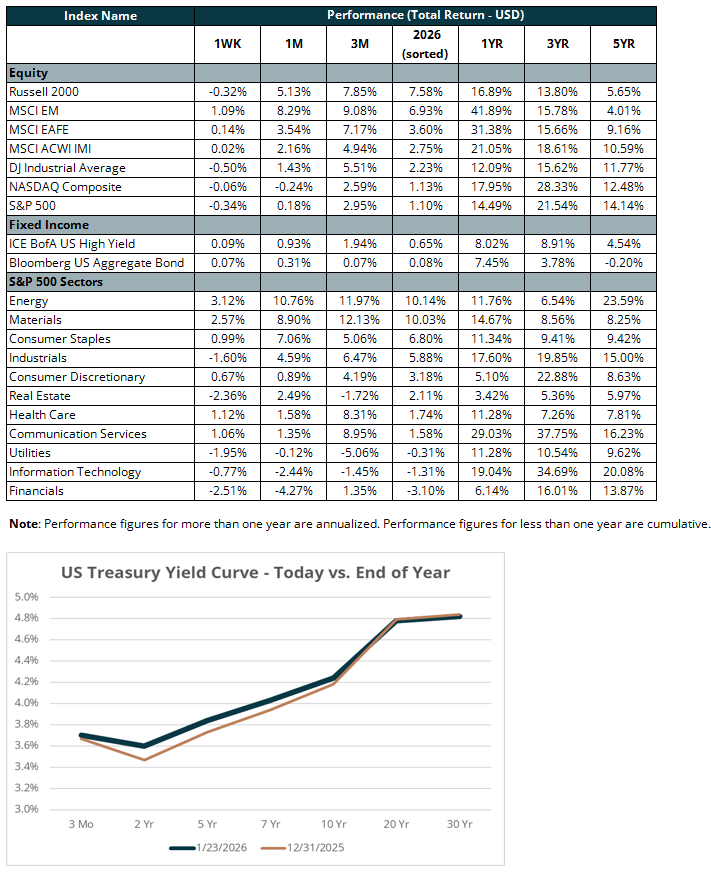

Bond market pricing ahead of the Federal Reserve’s policy meeting points to a pause after the recent run of rate cuts, with futures implying about a 97 percent chance the Fed holds rates steady when the meeting concludes Wednesday. While the Fed has cut rates by 25bps at each of its last three meetings, markets still price in at least one additional cut later this year, and expectations for an extended pause are growing as policy nears neutral, labor-market risks ease, and inflation appears to have peaked. Investor focus is also shifting toward political and policy risks, including pressure on Chair Jerome Powell from the Trump administration, speculation around his successor ahead of his term ending in May, and broader geopolitical or policy developments that could weigh on confidence and risk assets.

Looking ahead, investor focus on the trajectory of U.S. corporate profits in likely to intensify this week as roughly 20 percent of the S&P 500 will be reporting earnings. Overall earnings growth is expected to accelerate this year and broaden beyond the narrow group of leaders. Results from Apple, Microsoft, Meta Platforms, and Tesla, four members of the so-called Magnificent Seven, will be highlighted. A central question this season is whether companies are beginning to see measurable financial returns, such as increased revenue or cost efficiencies, from their massive investments in AI. Skepticism over the payoff from heavy data center and AI infrastructure spending weighed on technology stocks late in 2025, particularly the mega-caps that had driven much of the multi-year U.S. equity rally. Entering 2026, many remain well below prior highs, lowering the bar for earnings and guidance and increasing the potential for positive surprises as companies outline expectations for the year ahead.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Geopolitical Developments in the Middle East Drive Market Volatility