Market Commentary

Market-Broadening Rally Materializing at Last

by Sequoia Financial Group

by Sequoia Financial Group

“This earnings shift puts fundamental backing to one of the most prominent calls on Wall Street . . . The stock market rally will broaden.” This quote reflected common sentiment at the start of 2024, when just a few “Magnificent 7” stocks had been driving much of the S&P 500’s earnings growth and returns. Such market concentration is often unsustainable. Over the past week, that expected broadening appears to be materializing, albeit two years later than expected.

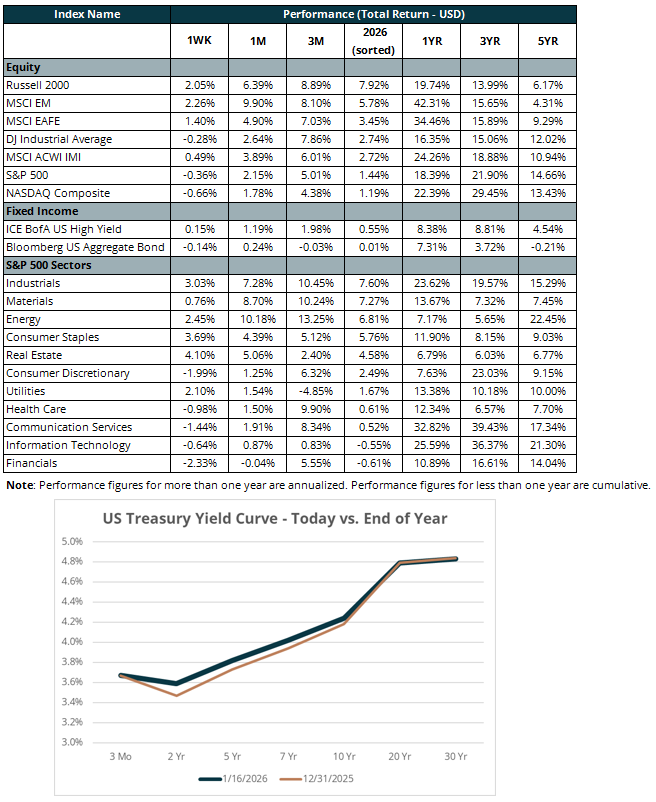

Despite the broadening-out call in early 2024, narrow market breadth persisted through 2025. In 2025, around one-third of S&P 500 constituents beat the overall Index, but more than 60% are outperforming year to date in 2026. Many of the winners so far this year lagged last year. The equal-weight S&P 500 is beating the market-weighted S&P 500, Value is ahead of Growth, Small Cps are leading Large Caps, and Energy is outpacing Technology.

That shift is good news for active managers, who have struggled in recent years. Many of the Magnificent 7 are Large-Cap Growth names, and only 28% of managers in that category beat their benchmarks over the past three years. Active managers may find it impractical to hold overweighs in names such as Apple (AAPL), which commands a >10% weight in the iShares Russell 1000 Growth ETF (ticker: IWF). While Apple is an exceptional company, it is expected to grow earnings 8% annually over the long term, yet it trades at 30.4x forward earnings. This could be unattractive considering IWF’s 14% expected earnings growth and 28.3x P/E multiple. An underweight to AAPL detracted from relative returns in 2023, when the stock gained 49%. With the rally broadening in 2026, 77% of Large Cap Growth managers are now outperforming their passive peers. Whether this trend lasts could depend on Q4 earnings results, which kicked off last week with the largest US banks.

The top four U.S. megabanks (JPMorgan, Bank of America, Wells Fargo, Citigroup) all fell last week. Their shares dropped an average of 5.2%, making Financials the worst-performing sector for the week as well as year to date. A bright spot was improving credit quality. Wells Fargo’s credit card balances 90+ days past due, relative to outstanding balances, fell to 1.43% from 1.51% in Q4 2024. This is encouraging given concerns about a weakening consumer. Economists have described a K-shaped economy, in which low-income consumers have negatively diverged from their high-income peers. The low-income segment is more vulnerable to missed payments, so better delinquency data is a positive sign. The trend will be tested this week, when regional banks report. Ally Financial (ticker: ALLY), a major auto lender, reports on Wednesday, January 21.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Rising Oil Prices, Inflation Expectations Send Stocks and Bonds to 2026 Lows