Market Commentary

Geopolitical Developments in the Middle East Drive Market Volatility

by Sequoia Financial Group

by Sequoia Financial Group

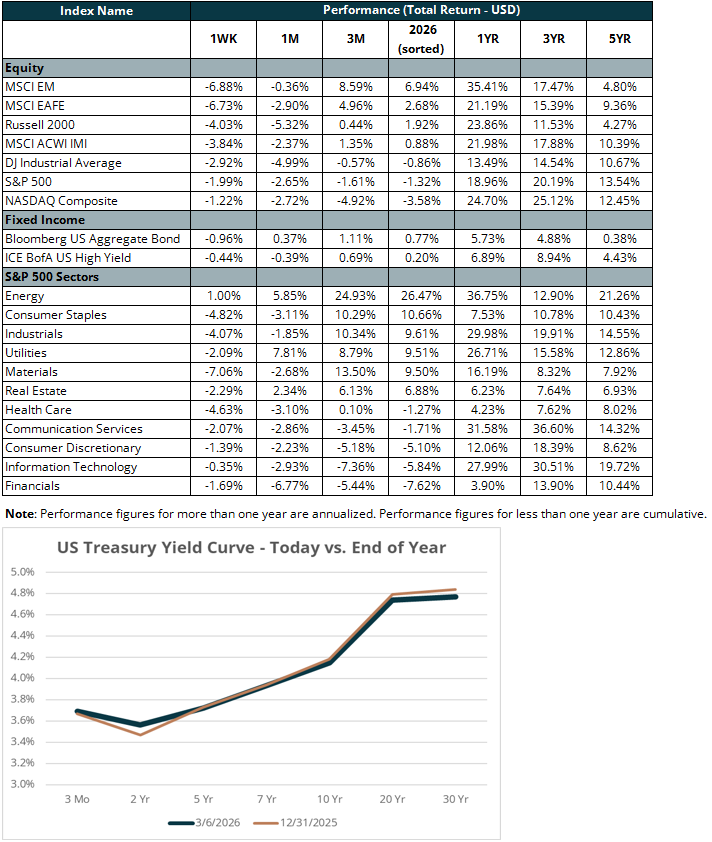

U.S. equity markets declined last week as geopolitical developments dominated the narrative. The S&P 500, an index of the largest U.S. companies, fell two percent for the week as escalating conflict between the United States and Iran drove heightened market volatility. Small-cap equities fared even worse – down four percent – as risk assets broadly came under pressure. Fixed income markets did little to offset equity volatility: the Bloomberg U.S. Aggregate Bond Index declined one percent for the week as U.S. Treasury rates rose across the yield curve. The U.S. 10-Year Treasury yield ended the week higher at 4.15 percent.

Much of the week’s market movement was tied directly to developments in the Middle East. U.S. equities initially shook off the attack on Iran but succumbed to pressure as the week progressed due to concerns that a prolonged and broadening conflict could be poised to destabilize the region. Oil prices surged as investors reacted to the growing risk of supply disruptions stemming from the conflict with Iran. The Strait of Hormuz, a critical maritime chokepoint connecting the Persian Gulf to the Arabian Sea, is in effect closed. According to the U.S. Energy Information Administration, roughly 20 million barrels of oil per day (~20 percent of the global supply of seaborne crude) passed through this waterway prior to the conflict. Major oil producers Iraq and Kuwait have begun cutting oil production due to full storage facilities. The sharp increase in energy prices pushed inflation expectations higher, raising concerns that inflation could remain more persistent than previously anticipated.

Economic data released during the week added another layer of complexity to the outlook. The February employment report came in weaker than expected, as the U.S. economy lost 92,000 jobs during the month and prior months’ data was revised lower. While the unemployment rate remained relatively stable, the softer hiring data suggested continued cooling in labor market momentum. The report reveals a more challenging backdrop for policymakers, as the Federal Reserve must balance signs of slowing employment growth against the risk that energy prices could push inflation higher. In other words, the Fed appears increasingly caught between the two sides of its dual mandate – supporting employment while maintaining price stability.

Developments over the weekend continued to draw investor attention. Iranian authorities announced the selection of a new Supreme Leader, Mojtaba Khamenei, son of former supreme leader Ali Khamenei. On Sunday, oil prices crossed $100/bbl for the first time since Russia invaded Ukraine in 2022. While the long-term implications remain uncertain, investors will continue to monitor developments in the region closely.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Rising Oil Prices, Inflation Expectations Send Stocks and Bonds to 2026 Lows