Market Commentary

Equities Extend Losing Streak as Iran Conflict Roils Markets

by Sequoia Financial Group

by Sequoia Financial Group

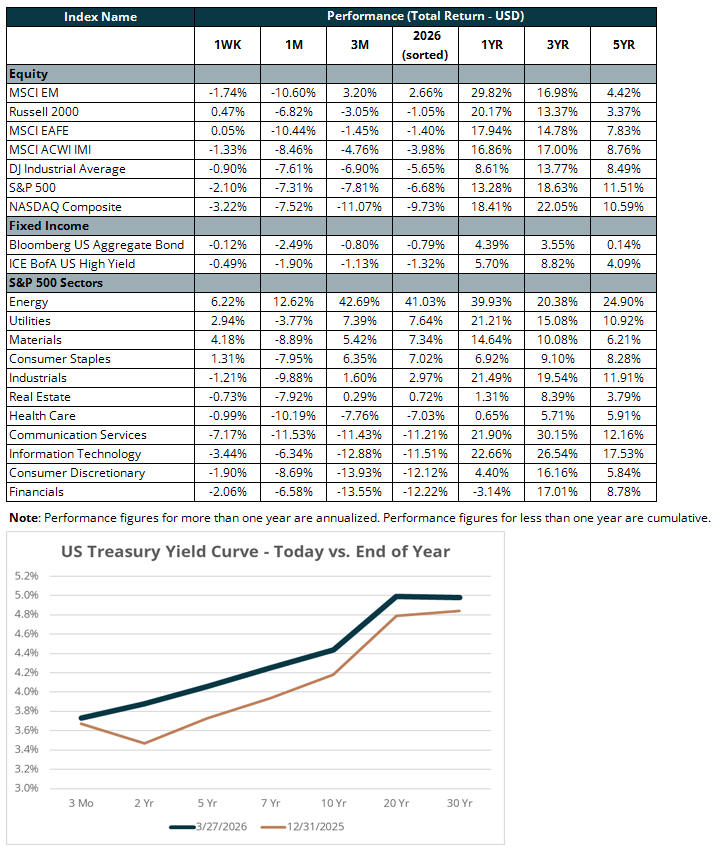

U.S. equities declined as the ongoing conflict in the Middle East continued to dominate market sentiment. The S&P 500 posted its fifth consecutive weekly loss, falling 2.1 percent during the week, while the NASDAQ Composite dropped 3.2 percent on weakness in technology, software, and memory names. The Bloomberg U.S. Aggregate Bond Index (the “Agg”), a broad measure of investment-grade fixed income, declined 0.1 percent, offering little of the ballast bonds have historically provided during periods of equity weakness. The NASDAQ has now declined in ten of the past eleven weeks, and the S&P 500 has touched its lowest level since early September. With equities and bonds both under pressure, traditional diversification has provided little relief for investors.

The week’s market action was dominated by developments in the Iran conflict, which has now entered its second month. Early in the week, markets briefly rallied on hopes for de-escalation after the President paused strikes on Iranian energy infrastructure and signaled productive diplomatic discussions. That optimism faded quickly, however, as Iran publicly denied that negotiations were underway and reports emerged that the Pentagon was dispatching an additional 10,000 troops to the region. On Thursday, the President announced a 10-day extension to the pause on strikes to allow more time for diplomacy, offering another brief lift to risk sentiment. Iran signaled over the weekend that it was prepared to respond to a U.S. peace proposal, while regional diplomats gathered in Pakistan to explore a path toward an end to the conflict. Over the course of the war, more than 3,000 people have been killed and 4 million displaced across the region. The Strait of Hormuz, through which roughly 20 percent of the world’s seaborne crude oil passes, in effect remains closed, though some modest signs of relief emerged as Saudi Arabia’s East-West pipeline, which bypasses the Strait, reportedly reached full capacity and a small number of vessels transited the waterway over the weekend. Oil ended the week at over $110/barrel.

In response to the war, the market has dramatically repriced Federal Reserve expectations. According to CME Group’s FedWatch tool, markets are now assigning a 74 percent probability of no rate cuts in 2026, a considerable shift from one month ago when the odds of no cuts stood at just 3.9 percent. The U.S. 10-Year Treasury yield rose on the week, ending at 4.4 percent, reflecting a market that remains more focused on the inflationary implications of higher oil prices than on the potential drag to economic activity, a view that could come under increasing pressure the longer the conflict persists. The Fed now faces an increasingly difficult policy dilemma: with oil prices fueling inflation expectations while the labor market remains soft, policymakers are caught between the two sides of their dual mandate. The March payrolls report, due Friday, will be closely watched for additional signs of labor market stress. In the meantime, investors will continue to be attentive to developments in the Middle East.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

")

Equities Extend Losing Streak as Iran Conflict Roils Markets