Progress Was Earned

If 2025 taught us anything, it’s that progress can be made in uncertain times. The past year brought meaningful gains across markets, but they weren’t handed to anyone. Instead, they had to be earned—through patience, perspective, and a willingness to stay the course when the headlines made that challenging.

There was no shortage of noise. The year’s defining event—the sweeping U.S. trade policy reform dubbed “Liberation Day”—set off bouts of optimism and anxiety in equal measure. Markets rose and fell with each new interpretation of what it all meant. Yet beneath those emotional swings, something steadier was taking shape: company fundamentals were improving. Earnings grew, margins expanded, and corporate balance sheets remained sound. In short, the foundation for better markets was quietly being rebuilt, even as sentiment wavered.

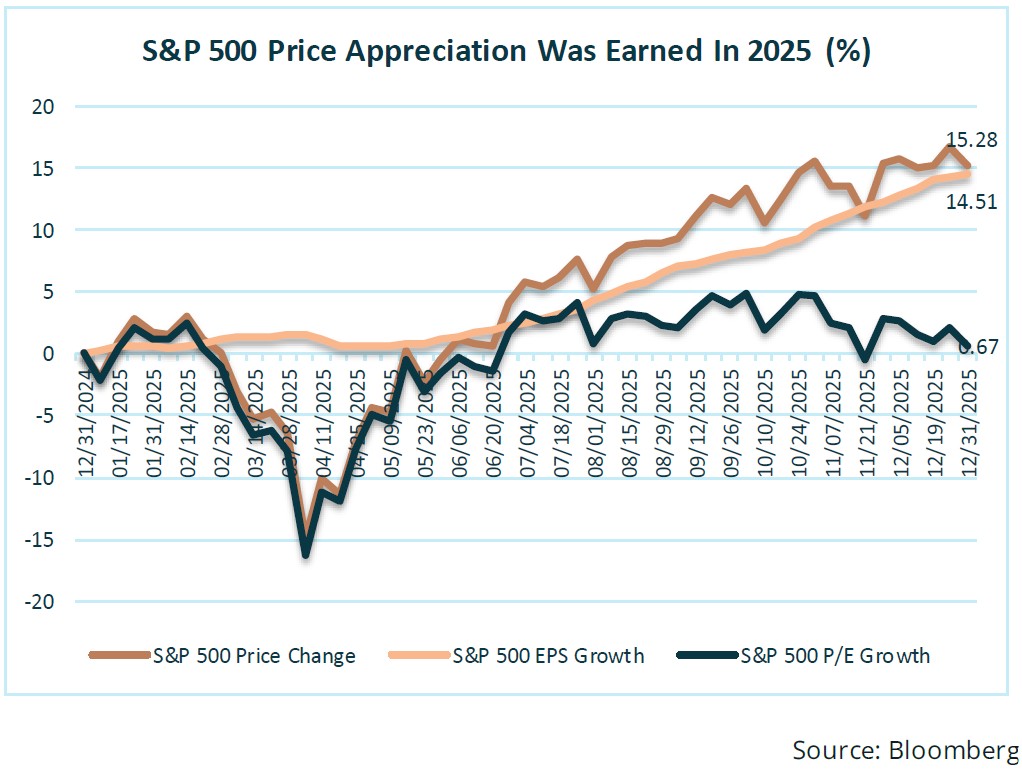

By year-end, equity investors had reason to smile. The S&P 500 gained roughly 18%, and what made those returns particularly notable was their foundation in real earnings growth rather than valuation expansion. As trade uncertainty diminished and productivity began reflecting the early fruits of technological reinvestment, profit growth exceeded expectations. Valuations moved around a lot, but earnings momentum gave markets a sturdier base than many anticipated at the peak of policy uncertainty early in the year.

The chart below highlights how fundamental growth drove the S&P 500’s gains in 2025. Despite sharp swings in valuation multiples throughout the year, the steady rise in corporate earnings provided the foundation for the market’s strong performance.

Technology remained the focal point, but the character of that leadership evolved. In prior years, investors might have rightly asked whether tech’s dominance was sustainable or simply a reflection of excess enthusiasm. In 2025, that question began to find an answer. Spending on artificial intelligence, cloud infrastructure, and digital media surged again in the second half—but this time, the payoff was measurable. These sectors accounted for about 60% of the S&P 500’s total return and nearly two-thirds of its earnings growth. What once looked like concentrated leadership increasingly resembled genuine reinvestment and a powerful structural shift in corporate profitability. AI-led innovation, once abstract, began showing up in productivity data, operating margins, and forward guidance across industries.

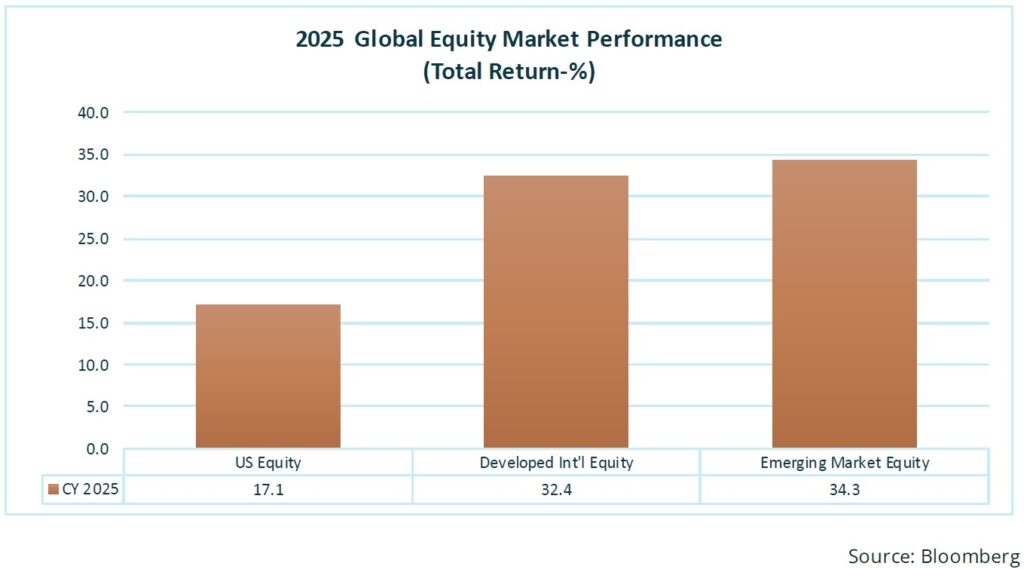

If 2025 was a good year for staying invested, it was an even better one for being globally diversified. After several years of disappointment, international equities finally held up their end of the bargain. Non-U.S. markets outperformed the U.S., aided by appealing starting valuations, better earnings growth abroad, and a slightly weaker dollar. Emerging markets benefited from stronger domestic fundamentals and capital inflows seeking opportunities beyond American shores. For globally allocated investors, those who stuck to their policy weights even when it was hard, the year served as a timely reminder: Diversification is often uncomfortable, but comfort is rarely profitable.

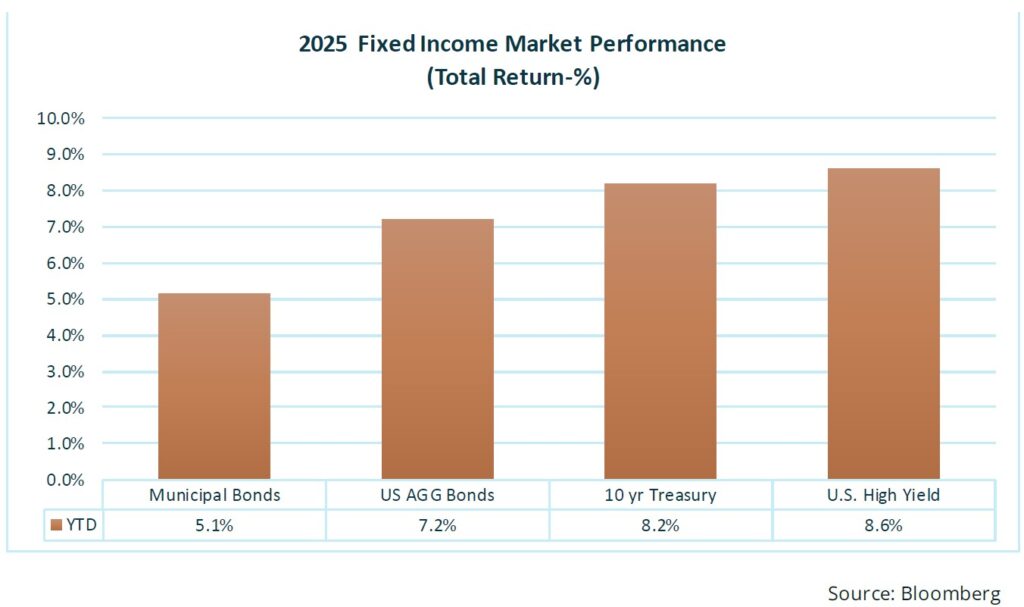

Fixed income in 2025 delivered on both sides of the ledger, with investors rewarded by strength in both interest rate and credit exposure. As inflation eased and growth settled into a steadier, less worrisome pace, yields drifted lower across the curve, turning duration from a source of prior-year pain into a meaningful contributor to returns. At the same time, a still healthy economy, strong corporate profitability, and generally sound balance sheets kept defaults subdued and left credit spreads hovering near their historical lows, allowing investors to earn attractive spread income without having to venture too far out on the risk spectrum. After several years in which stocks and bonds too often declined together, 2025 felt like a throwback to a more traditional world—one in which fixed income once again provided both income and ballast, and diversified portfolios behaved the way their architects had intended. As the accompanying chart shows, both credit and duration produced total returns exceeding 8% for the year, underscoring just how rare and rewarding this combination proved to be.

Gold’s 2025 ascent has been less a speculative moonshot than a slow, rational repricing of risk in a world that has finally recognized its own fragility. With real rates oscillating but never offering a convincing, risk-free alternative, investors have treated gold as the asset you buy not because you expect the world to end, but because you no longer take stability for granted. Persistent fiscal deficits, recurring debt ceiling theatrics, and the nagging sense that inflation is less “transitory” than “tamed for now” have all chipped away at confidence in paper promises, nudging capital toward an old, dull asset whose virtue is precisely that it doesn’t depend on anyone’s performance. Add to that a bid from central banks diversifying away from the dollar and occasional geopolitical flare-ups that remind us risk isn’t just a line item in a spreadsheet, and gold’s outperformance in 2025 looks less like a surprise and more like the logical outcome of a decade in which defense has finally regained respect.

Looking back, 2025 might not be remembered for runaway optimism or dramatic headlines, but for something subtler: a market that learned to look through the noise and reward tangible progress. Economic growth remained healthy, inflation continued to fade, and corporate America proved once again that it could adapt with agility. For investors willing to stay focused on fundamentals, diversify their exposure, and remain patient through volatility, the year offered not just returns but perspective. Progress, as ever, tends to come not through comfort, but through resilience.

Data Fog: Reading Between the Lines and the Implications on Monetary Policy

The latest batch of post-shutdown numbers looks, at first glance, like a reassuring nod to the Fed: growth is cooler, inflation is softer, and the quarter-point cut appears more like prudent risk management than aggressive easing. Yet in this business, the first look is rarely the last word. The market’s muted reaction tells you a lot: If investors truly believed the data painted a clear and benign picture, front-end yields would not be this stubborn, and the odds of another cut would not be this restrained. Instead, there’s an undercurrent of skepticism—not so much about the direction of the economy as about the reliability of the scorecard itself. When the statisticians are restarting the machinery mid-stream after a prolonged shutdown, you should expect noise, quirks, and holes in the time series, and you should be wary of drawing precise conclusions from imprecise inputs. In other words, we are being asked to predict the cycle when the measuring tools are least reliable.

Once you look past the statistical fog, the picture that emerges is more familiar, and a bit less benign. Job gains are decelerating, hiring is increasingly concentrated in fewer sectors, and wage growth is cooling as workers gradually relinquish the leverage they had earlier in the expansion. The most telling development may not be the headline payroll figure, but the rise in unemployment driven by more people reentering the labor force, a pattern more consistent with financial strain than with exuberant optimism. Put together, this is a classic late-cycle mix: softer labor conditions, easing inflationary pressures, and a Fed that has begun to cut, not because it sees a crisis, but because it knows the balance of risks is shifting and would rather be early than late.

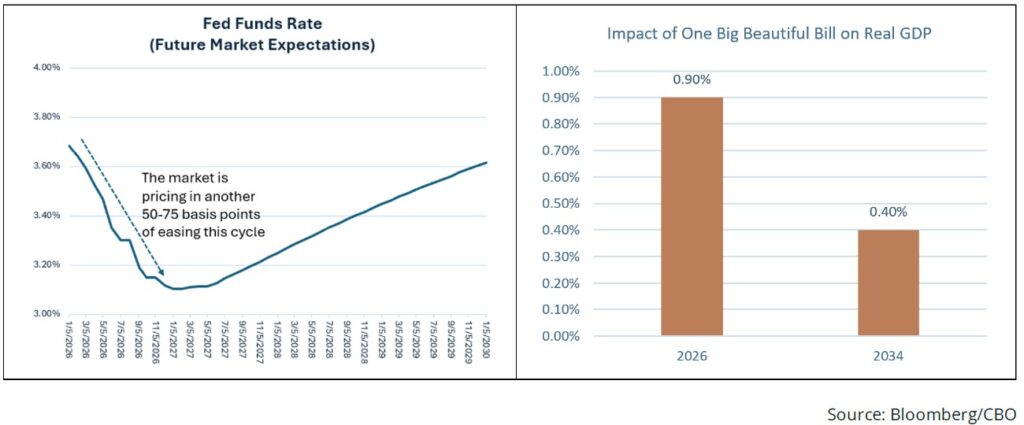

As we look toward 2026, the prospect of further monetary easing looms large in the background, even if it is not yet the main act. With the current chair’s term ending in May and the odds rising that a more administration-friendly successor will be in place by spring, it is reasonable to assume a modest downward tilt in policy at the short end of the curve. That shift has been reinforced by the Fed’s recent decision to formally draw a line under quantitative tightening and begin expanding its balance sheet once again, a change that adds liquidity to the system and provides another potential source of accommodation for risk assets. Whether this policy mix ultimately filters through to long-term yields is far less certain; given persistent fiscal deficits and lingering inflation concerns, it would not be surprising if longer-term rates remained somewhat elevated even as overnight rates become cheaper. For investors worried about an eventual downturn or growth scare, the key takeaway is straightforward: he Fed still has room to act, and that capacity offers an essential buffer against a more severe economic outcome.

As we look toward 2026, the prospect of further monetary easing looms large in the background, even if it is not yet the main act. With the current chair’s term ending in May and the odds rising that a more administration-friendly successor will be in place by spring, it is reasonable to assume a modest downward tilt in policy at the short end of the curve. That shift has been reinforced by the Fed’s recent decision to formally draw a line under quantitative tightening and begin expanding its balance sheet once again, a change that adds liquidity to the system and provides another potential source of accommodation for risk assets. Whether this policy mix ultimately filters through to long-term yields is far less certain; given persistent fiscal deficits and lingering inflation concerns, it would not be surprising if longer-term rates remained somewhat elevated even as overnight rates become cheaper. For investors worried about an eventual downturn or growth scare, the key takeaway is straightforward: he Fed still has room to act, and that capacity offers an essential buffer against a more severe economic outcome.

In addition to monetary policy accommodation in the form of lower rates and an expanding Fed balance sheet, the OBBBA is set to provide a meaningful fiscal tailwind as 2026 begins, with the Congressional Budget Office estimating the legislation will lift real U.S. GDP by about 0.9% next year. A key channel is consumer-focused tax relief: Households are projected to receive significantly larger refunds in early 2026, helped by a higher standard deduction, enhanced child tax credits, and new deductions that effectively lower the tax bill for many working and middle-income families. In parallel, the bill introduces tax incentives for private-sector investment to pull forward capital spending and expand productive capacity. Taken together, these consumer benefits and investment incentives should support demand, encourage hiring and capex, and amplify the growth impulse from easier monetary policy in 2026.

AI Adoption: A Productivity Boom in Progress

Artificial intelligence has become this cycle’s signature theme, but like most powerful ideas in markets, its progress is anything but linear. Over the past year, companies poured capital into AI infrastructure—data centers, chips, and computing power—while actual, broad-based adoption lagged behind the headlines. That widening gap between spending and demonstrated payoff has left some investors uneasy, especially as more of that capex is financed with borrowed money. History shows that when enthusiasm gets too far ahead of evidence, markets eventually impose discipline: Capital migrates from those merely building capacity to those proving they can turn it into profits. The coming phase, therefore, may not be about who can talk the loudest about AI, but who can quietly show it on the income statement.

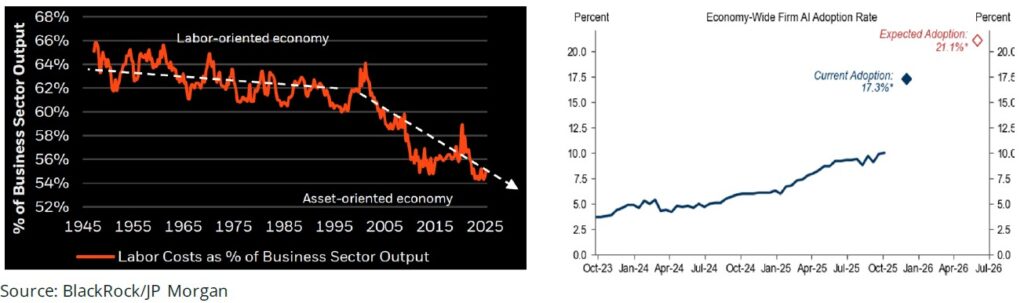

One helpful way to frame that income statement impact is as a classic cost story rather than a pure growth story: If AI succeeds in trimming labor costs as a share of output by even a few percentage points, and if most of that saving accrues to corporations while the rest flows to AI providers, the implications for margins and free cash flow are substantial. In that world, companies with large, repeatable, process-driven workloads would see meaningful improvement in unit economics, while a parallel ecosystem of platforms and service firms would enjoy growing, annuity-like revenue streams. So far, much of the market’s strength has been rooted in real earnings growth, particularly among the firms at the center of the AI buildout, where double-digit profit gains and strong free cash flow generation have validated at least part of the excitement. The pricing today reflects not only continued spending but also a powerful assumption: That AI will sustain the productivity and margin improvements that began years ago and carry them forward. As the chart below illustrates, we’ve seen a ~10% reduction in labor costs as a percent of revenue since the 1990s. While not guaranteed, it seems plausible that the rapid increase in AI adoption across the economy will sustain this trend.

If it does, sustained improvements in margins and earnings should follow, providing a more durable foundation than narrative alone can offer. As always, the key is distinguishing between what is merely exciting and what is truly profitable. AI, in that sense, is not a departure from past cycles but a new arena for an old challenge: separating the enduring from the ephemeral.

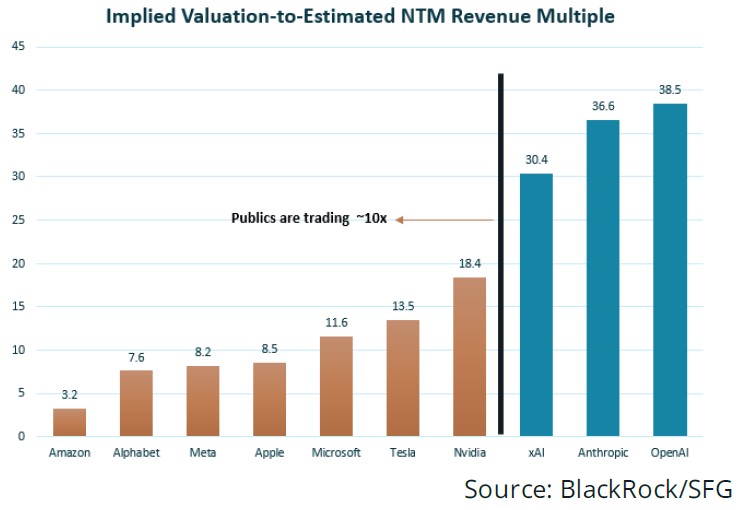

AI is likely to lift economic productivity over time, but the market path from here will almost certainly be uneven rather than a straight upward trend. Heavy AI capex is set to weigh on free cash flow in 2026, and much will depend on how long investors are willing to wait for that spending to translate into convincing gains in profitability and return on investment. Today’s excess looks most pronounced in private markets, where a handful of leading large language model platforms command the richest valuations and many standalone LLM businesses are burning cash well in excess of what their operations generate. By contrast, listed AI beneficiaries, though hardly cheap, tend to be priced with at least some reference to observable earnings and cash flows, leaving the most significant bubble risk in late-stage private valuations rather than in the broad public equity market.

We Expect Return Opportunities to Broaden Out

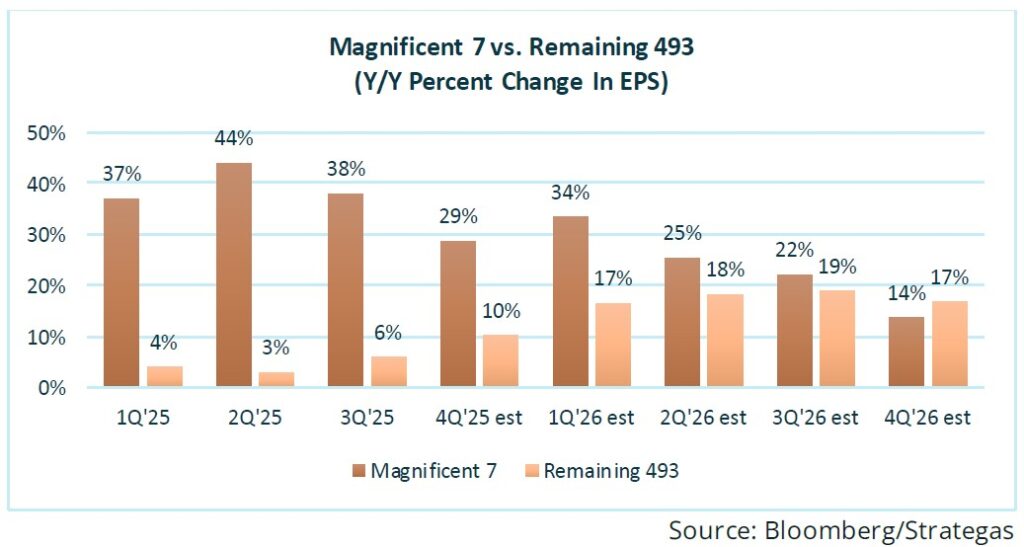

The market’s gains have been highly concentrated, reflecting where the earnings growth has been. In 2025, the market-cap-weighted index beat the equal-weighted index by 6.6 percentage points, indicating that large-cap names—especially mega-caps—were responsible for most of the advance while the average stock lagged. Looking to 2026, the broader adoption of AI has the potential to improve fundamentals across a wider swath of companies, allowing more of the market to participate in earnings growth.

Conclusion

2025 offered a reminder that investors can still make meaningful progress in an environment that rarely felt calm or straightforward. Progress was earned through discipline: staying invested when headlines were unsettling, leaning on diversification when it was uncomfortable, and letting fundamentals—not sentiment—set the tone.

Across assets, that discipline was rewarded. Equities advanced on the back of real earnings growth, not just higher multiples, while leadership in AI-related sectors increasingly reflected tangible investment and profitability rather than story alone. Global exposure finally paid off as international and emerging markets contributed more fully and fixed income once again provided both income and ballast, restoring a more traditional role in balanced portfolios.

Policy shifted from a headwind toward a cautious tailwind. Monetary authorities have moved from restraint to measured support, and fiscal policy is adding its own boost, even as noisy data clouds the precise strength of the cycle. That mix argues less for heroics than for balance: enough risk to participate if growth persists, enough defense to endure if the path is choppier than the consensus suggests.

AI sits at the center of both the opportunity and the uncertainty. Capital spending has been heavy, the productivity payoff is building but uneven, and pockets of excess—especially in select private markets—have emerged alongside genuine, cash-generating winners. The investment task is to distinguish durable cash flows from hopeful narratives and to remember that even powerful technological shifts translate into returns in fits and starts, not in straight lines.

As 2026 begins, the conditions are in place for returns to broaden beyond a narrow group of leaders. A healthier backdrop for global equities, a more supportive policy stance, the renewed usefulness of fixed income, and the gradual diffusion of AI-driven productivity all favor portfolios that are diversified, quality-focused, and time-horizon aware. The lesson of the past year is simple but enduring: Progress tends to accrue to investors who stay thoughtful, flexible, and invested through the noise rather than trying to trade around it.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

This material is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Diversification cannot assure profit or guarantee against loss. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. Sequoia Financial Advisors, LLC makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third-parties. Certain assumptions may have been made by these sources in compiling such information, and changes to assumptions may have material impact on the information presented in these materials. Sequoia Financial Advisors, LLC does not provide tax or legal advice. Investment advisory services offered by Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Rising Oil Prices, Inflation Expectations Send Stocks and Bonds to 2026 Lows