Market Commentary

Escalating Tensions in Middle East Affect Stocks and Oil

by Sequoia Financial Group

by Sequoia Financial Group

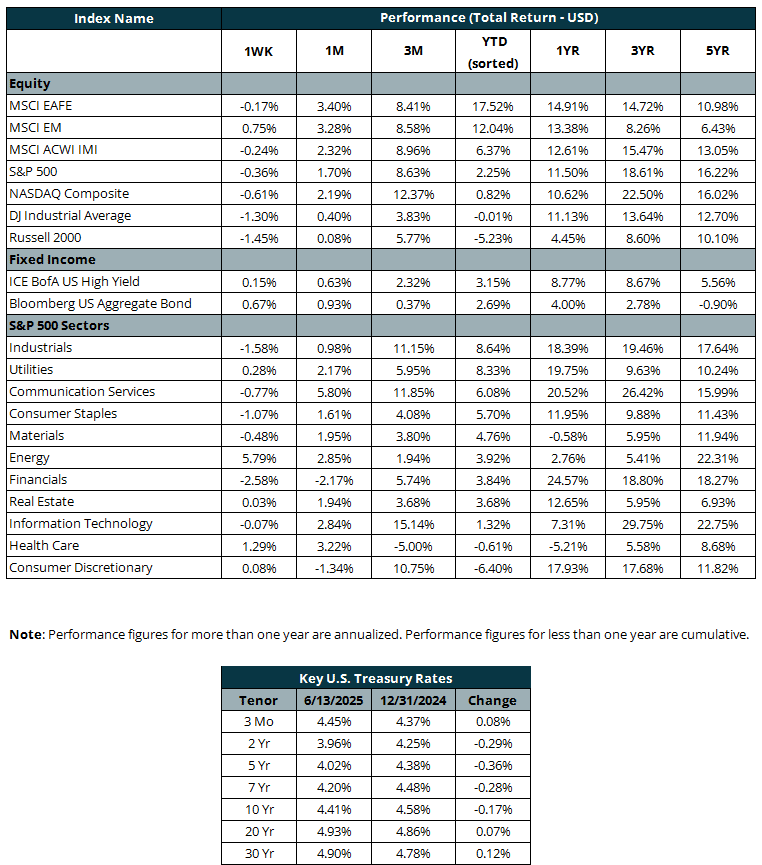

Escalating tensions in the Middle East rattled markets this week after Israel launched a wave of airstrikes on Iranian nuclear and military infrastructure, pushing energy prices sharply higher and driving investors toward safe-haven assets. U.S. crude surged more than 7% on Friday, marking its largest single-day gain in months. It finished the week up nearly 12% at around $73/bbl, the highest level since late 2023. The spike lifted energy stocks in early trading but weighed on broader sentiment. U.S. equity indices fell on Friday after recording gains in the previous two weeks. The S&P 500 and the NASDAQ posted fractional weekly declines, while the Dow finished down more than 1%.

On the inflation front, May’s Consumer Price Index (CPI) offered some relief. Headline CPI rose just 0.1% month over month, coming in below expectations, putting the annual inflation rate at 2.4%. Core CPI, which excludes food and energy, also rose 0.1% in May, falling short of the anticipated 0.3% increase. On an annual basis, core inflation remained at 2.8% for the third consecutive month, slightly below expectations of 2.9% and marking the lowest level since 2021. Shelter and food each rose 0.3%, but broad declines in categories like gasoline (-2.6%), apparel (-0.4%), and vehicle prices helped keep overall inflation subdued.

U.S. Treasury markets sent mixed signals this week, with yields briefly dipping midweek before rising again on heightened geopolitical tensions. The 10-year yield climbed roughly 6.5 basis points to 4.41% by Friday following news of Israeli airstrikes on Iran. Thursday’s 30-year Treasury auction drew stronger-than-expected interest, with a yield of 4.84%, well below the previous day’s 4.91% close, calming fears after the bond’s yield had recently topped 5%. Solid auctions for both 10- and 30-year notes provided a stabilizing force in the market and reinforced confidence in the safety of U.S. government debt.

Meanwhile, trade negotiations between U.S. and Chinese officials ended with a preliminary agreement on several key issues, including tariffs. Both sides endorsed a framework, though final approval from Presidents Trump and Xi remains pending. Hopes for a U.S.-China tariff truce lifted market sentiment earlier in the week, driving gains in sectors such as semiconductors and consumer discretionary. However, the rally lost steam as risk appetite faded, causing small caps to lag the broader market.

U.S. consumer sentiment rebounded in June for the first time in six months, according to the University of Michigan’s preliminary survey. The index rose to 60.5 from a near-record low of 52.2 in late May, coming in well above expectations as concerns about inflation eased. Short-term inflation expectations fell sharply to 5.1% in June, down from 6.6% in May, while long-term expectations edged down for a second consecutive month to 4.1%.

Looking ahead, the Federal Reserve is expected to leave interest rates unchanged when it wraps up its two-day meeting on Wednesday. While no near-term move is anticipated, markets are still pricing in the possibility of rate cuts later this year. According to the CME Group’s FedWatch tool, futures suggest that investors expect one to three quarter-point rate cuts by year end, most likely beginning in September and potentially followed by another in December. With the Federal funds rate still above the current inflation rate, the Fed has room to ease policy if needed. However, policymakers remain cautious, waiting for greater clarity on the impact of tariffs and broader economic momentum before making any moves.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Geopolitical Developments in the Middle East Drive Market Volatility