Market Commentary

Equity Markets Reach Records After Mid-East Tensions Ease

by Sequoia Financial Group

by Sequoia Financial Group

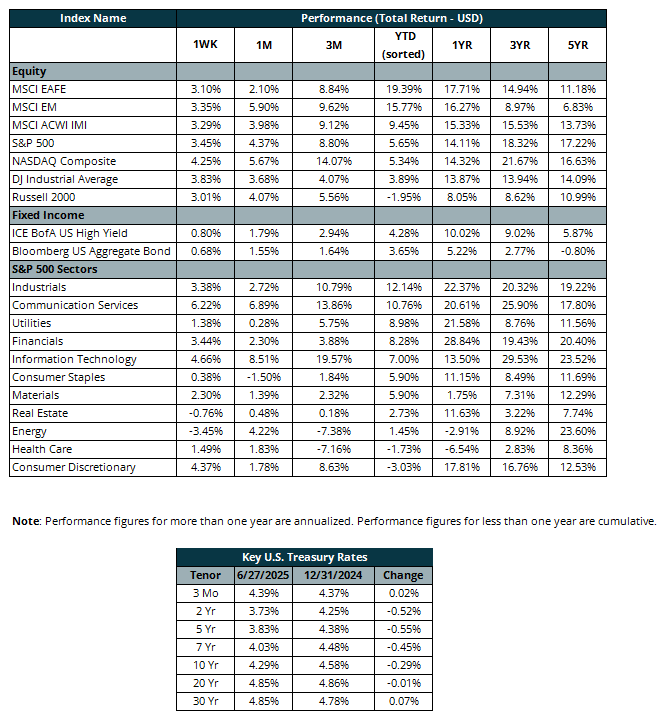

The S&P 500 and the NASDAQ both closed at record highs on Friday. Earlier in the week, President Trump announced a ceasefire agreement between Israel and Iran. Since the start of June, crude oil prices had surged 21% from $61/bbl to $74/bbl on fears that Iran would close the Strait of Hormuz, through which 20% of global oil production is transported. Goldman Sachs estimated that a 10% sustained increase in oil prices would result in a >0.2% increase in inflation and a 0.1% decline in GDP growth. After the ceasefire announcement, crude oil futures declined 11% this week to close at $65/bbl.

Unfavorable Personal Consumption Expenditure (PCE) price index readings on Friday weren’t enough to worry equity markets. The Federal Reserve’s preferred measure of inflation, the PCE rose an annualized 2.3% in May. Core PCE (excluding food and energy prices, which are more susceptible to supply dynamics) rose 2.7%, above the 2.6% estimate and the Fed’s 2% target. Services were the primary driver of the increases. Unlike goods, services are less affected by tariffs, so equity markets could be doubting that recent trade wars will have a sustainable impact.

Consumer spending and personal income declined 0.1% and 0.4% month-over-month, respectively. These drops, combined with higher inflation, indicate stagflationary concerns might be warranted. Stagflation would mean that the Fed would have to prioritize one pillar of its dual mandate over the other – price stability or maximum employment. The central bank can raise interest rates to combat inflation, but that would disincentivize companies from borrowing to stimulate their revenue and ultimately hire more workers. This has led to differing opinions among the Fed’s policymakers. While Fed Chair Jerome Powell is in a “wait-and-see” mode, many others are split between hiking rates and cutting them. The next meeting to determine the path of interest rates takes place in late July.

Developments in the global trade war might warrant an interest rate cut. During the week, the US and China confirmed that they signed an agreement for a trade “framework.” As part of the framework, China will continue allowing the export of rare earth metals, while the US will cancel a “range of restrictive measures imposed against Beijing.” China controls around 90% of the global supply of dysprosium and terbium, which are used to produce magnets used in many products, including cars and smartphones.

While tensions calmed with China, those with Canada intensified on Friday. President Trump announced an end to all trade talks with our northern neighbor after Canada announced a digital service tax on American tech companies. Equity markets remained unfazed, as the S&P 500 returned 0.5% on Friday. By Sunday, Canada reversed course and rescinded the tax.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

")

Iran Stalks Strait of Hormuz Chokepoint, Stoking Inflation Concerns