Equities Decline on Surprise Labor Market Weakness

by Sequoia Financial Group

by Sequoia Financial Group

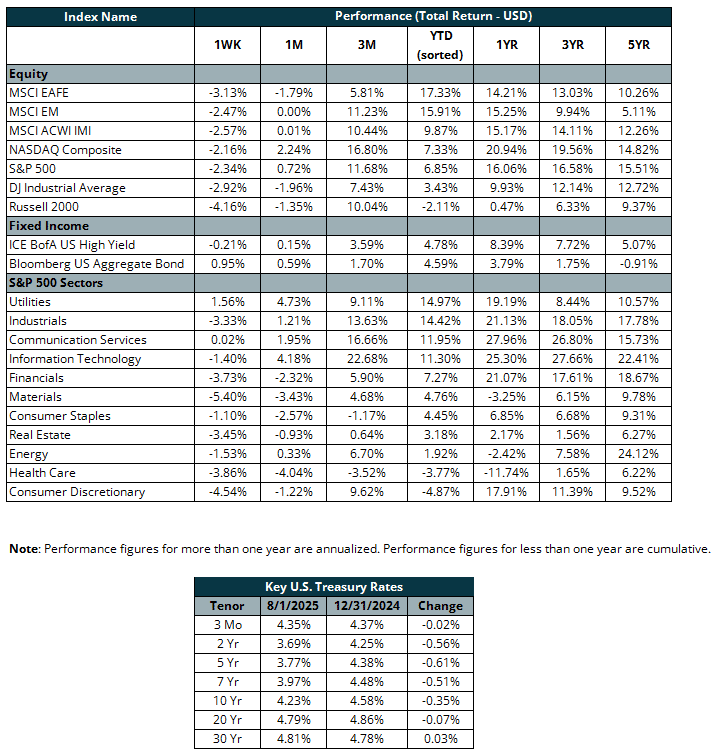

Last Friday’s employment report painted a troubling picture of the US labor market. The economy added 73,000 jobs in July, falling short of already modest expectations of 100,000. As a result, the S&P 500 returned -2.3% last week. More concerning were the substantial downward revisions to prior months, with May and June payroll statistics reduced by a combined 258,000 jobs.

The strong GQP print earlier in the week wasn’t enough to offset labor market concerns. GDP expanded at a 3% annualized rate, well above the 2.3% forecast. A reversal in net imports from Q1, when many companies front-loaded deliveries from overseas, was the primary driver of the current quarter’s growth. Thus, the print was less impressive than it looked, especially considering the economy’s H1/25 annualized growth of 1.2% was lower than the 2.8% growth in 2024.

The Bureau of Labor Statistics also released the Federal Reserve’s preferred measure of inflation on Friday. The Core PCE Price Index showed prices increased at an annualized 2.8% rate in June, in line with May. While much lower than the 6.5% rate in 2021, inflation is still higher than the Fed’s 2% target.

The contradictory data – labor market softness and stubborn inflation – is sending mixed signals as to the optimal path for interest rates. Accordingly, Wednesday’s Federal Open Market Committee (FOMC) meeting witnessed a “double dissent” for the first time since 1993. Two Federal Reserve governors voted for a rate cut, opposing the overall committee’s decision to hold rates steady at 4.25 – 4.50%. The markets must wait for a potential rate cut until mid-September, when the FOMC meets next.

Meanwhile, in the stock market, US tech companies guided for continuation of their AI spending momentum. Meta Platforms (ticker: META) reiterated its expectations of $66-72 billion in AI capex for the full year. META closed the week up 5.2%. While the overall market rewarded this spending commitment, other market participants are making pessimistic comparisons to the 2000 dot-com bubble. While the internet undoubtably provided productivity gains, the burst bubble of 2000-02 reflected investors’ willingness to overpay for those gains. The S&P 500’s forward price-to-earnings ratio of 21.8x isn’t as high as the 25.7x level seen in December 1999, but it is higher than the average 18.7x level over the past 10 years. Only time will tell whether tech firms can adequately monetize their AI expenditures. Many investors have lost money by rationalizing, “this time is different.”

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Strong Tech earnings outweigh doubts about further rate cuts in 2025