AI Theme Drives Equities to New Heights in Spectacular First Half

by Sequoia Financial Group

by Sequoia Financial Group

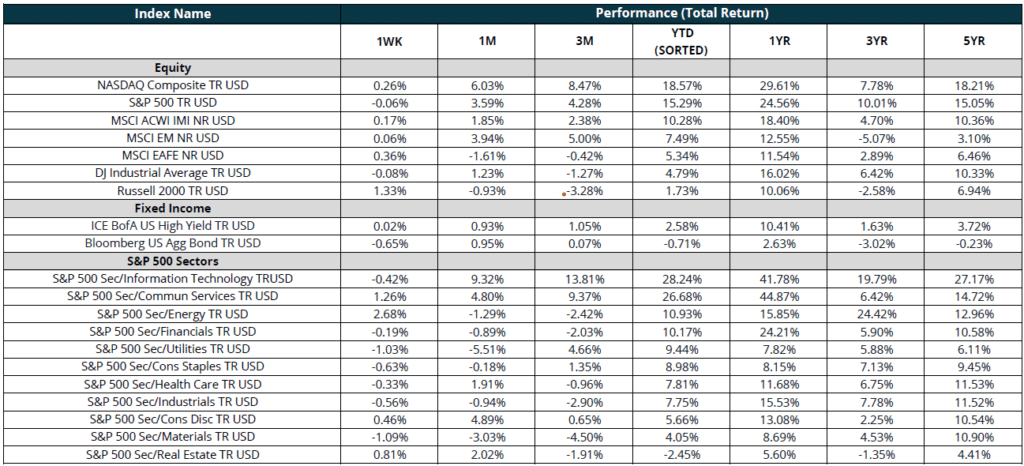

The first half of 2024 proved very profitable for stock investors. The benchmark S&P 500 Index returned more than 15%, while the tech-heavy NASDAQ jumped nearly 20%. The gains were driven by Nvidia (up 149%), Meta (up 42%), Broadcom (up 44%), Microsoft (up 19%), and other technology-related names.[1] Investor demand for tech stocks mirrored the growing global demand for artificial intelligence (AI), which is expected to drive efficiency across industries and geographies. Indeed, 199 S&P 500 companies referenced AI on earnings calls conducted between March 15 and May 23.[2]

The rally in equities was somewhat narrowly focused, however. Despite its benchmark status, the S&P 500 is top heavy, with its largest five constituents, all tech, making up more than 25% of the Index.[3] In contrast, the top five holdings in the equal-weighted S&P 500 Index make up less than 1.5% of the Index. And in the first half of 2024, the equal-weighted index returned just 4%.[4] That puts it on pace for a nice 8% annual return, but that pales in comparison to the market-cap weighted index’s lofty results.

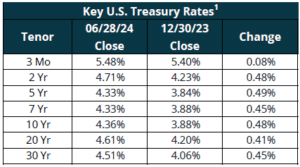

In contrast to the soaring stock market, the bond market stalled in the first half. Expectations of bond-friendly interest-rate cuts fizzled, as the Federal Reserve remained sidelined by stubbornly high inflation. The Fed still expects to cut rates before year end[5], which could drive better second half bond returns. But the first half ended with the benchmark index posting a small loss.

The final week of the first half was relatively quiet. The Fed’s preferred inflation indicator came in just as expected Friday. Core PCE, which excludes food and energy prices, climbed 2.6% year over year.[6] That’s down from the 2.8% reading in May but still well off the Fed’s 2% inflation target. Stocks ended last week little changed, while bonds ended the week down slightly.

This week could prove equally quiet, as equity markets close Wednesday afternoon and Thursday for the July 4th holiday. The calm will be broken soon after with highly-anticipated second-quarter earnings reports and more inflation readings. But for now, we’ll enjoy the strong first half gains as we set off fireworks and fire up the grill.

1. https://www.slickcharts.com/sp500/performance

3. https://www.morningstar.com/indexes/spi/spx/portfolio

4. https://www.spglobal.com/spdji/en/indices/equity/sp-500-equal-weight-index/#overview

6. https://www.cnbc.com/2024/06/27/stock-market-today-live-updates.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Protected: Q2 Market Review – Stocks Climb the Wall of Worry – Again