Market Commentary

Hopes of Peace Lift Markets, but Caution Still Warranted

by Sequoia Financial Group

by Sequoia Financial Group

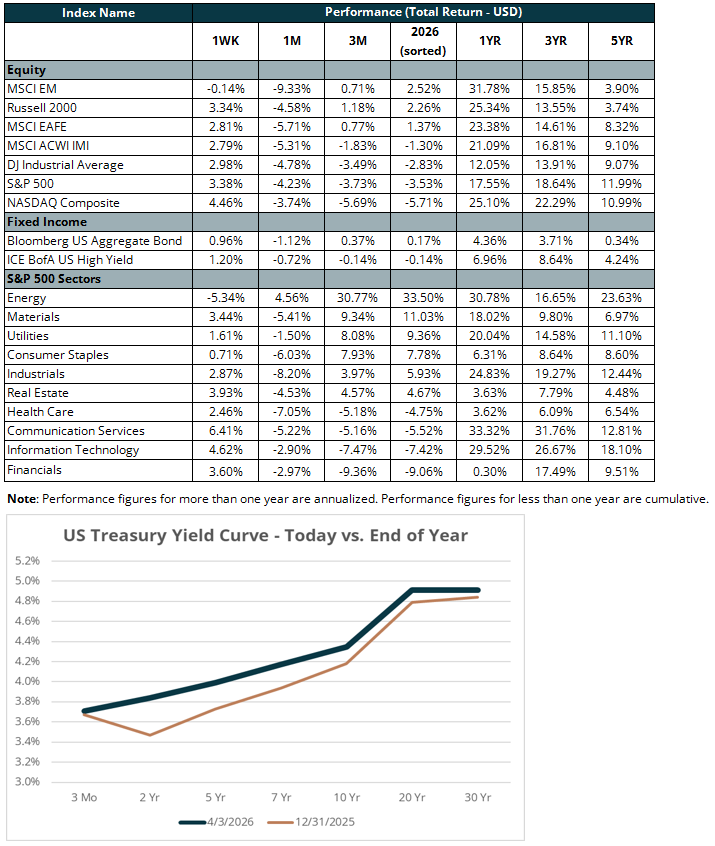

Equity markets staged a meaningful recovery last week, driven by optimism of a ceasefire in Iran. The S&P 500 returned 3.4 percent, the NASDAQ gained 4.5 percent, and the Dow Jones Industrial Average added three percent – the best weekly performance in recent memory. All three averages remain in negative territory year to date (YTD), after valuations entered the year at historically high levels.

The early optimism of Monday’s morning trading faded into a losing session, but Tuesday changed the tone entirely. An unconfirmed report suggested the Iranian President might be open to peace talks, triggering a sharp risk-on rally. Biotech and Magnificent 7 stocks surged. Oil, which might have been expected to crater on legitimate ceasefire news, fell only 0.8 percent. Energy traders were skeptical, noting the report contained little that was genuinely new, and questions continue as to whether the Iranian President holds real authority or is merely a figurehead.

Wednesday brought fresh anticipation as markets continued to rally ahead of the President’s evening address. Stock futures declined during the speech, however, as the President’s assertive tone seemed to outweigh possibilities for a ceasefire. At one point, the President promised to “send Iran back to the Stone Age where they belong.” The week’s gains ultimately held, but the whipsaw trading underscored the current fragility of the markets.

Last week marked a sharp reversal in the sector leadership that has defined much of 2026. Energy, the year’s standout performer, gave back 5.3 percent last week. Every other sector finished in positive territory, on the back of an optimistic outlook on the war in Iran. Six of the Magnificent 7 stocks posted meaningful weekly gains, with Tesla (TSLA) the lone exception. Despite this, all Mag 7 stocks remain deeply under water for the year, with Microsoft (MSFT) leading the group lower at 23 percent.

Despite negative returns YTD, forward earnings growth expectations for the S&P 500 have risen from roughly 15 percent at the start of the year to 17 per cent today. Both estimates are well above the nine percent annualized pace over the past decade. Compression of valuation multiples has driven the S&P 500’s performance this year, explaining why growth stocks (trading at elevated valuations) have sharply lagged their value counterparts (-8.7 percent vs. +3.1 percent).

The week closed on a more constructive macroeconomic note. March’s jobs report surprised to the upside, with hiring defying expectations and reversing last month’s negative reading. The unemployment rate ticked down to 4.3 percent, offering some reassurance that the labor market continues to be resilient. Many market commentators questioned the significance of the unemployment reading, however, given the declining participation rate.

Earnings season is nearly upon us – large-cap Financials are set to kick things off in two weeks, with this week being relatively slow for corporate results.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory