Market Commentary

AI Concerns Weigh on Stocks, but Iran Likely to Dominate News Flow

by Sequoia Financial Group

by Sequoia Financial Group

A wave of concerns that the ongoing AI boom could hurt the overall economy was fueled last week by a report from Citrini Research. The report warned of AI-driven job losses, which in turn could decrease consumption and reduce corporate revenue. It also flagged business segments that could be at risk, from insurance to tax prep to food delivery. Citrini called it a “thought exercise” and a “scenario”, not a prediction. But the research piece rattled an already shaky market, pushing financials, logistics, and software stocks lower. Overall, the Dow Jones Industrial Average slid more than 800 points on Monday, while the S&P 500 dropped into negative territory for the year through February 23.

Stocks rebounded on Tuesday and Wednesday but failed to build on that momentum. Tuesday brought news that Meta had partnered with AMD to deploy AMD processing units in its data centers, and Wednesday saw a positive response to the President’s State of the Union address. However, a widely anticipated earnings report from NVIDIA failed to calm ongoing AI concerns, and the stock suffered its worst day since April. The largest constituent in the S&P 500 topped analysts’ estimates for earnings and revenue, and provided positive guidance. Yet competitive threats from China and fears that capital spending on AI could taper off overshadowed the results.

Renewed inflation fears and weak tech earnings further weighed on stocks. The Producer Price Index (PPI) jumped 0.5 per cent in January, higher than the 0.3 per cent expected. And core PPI, which excludes food and energy, jumped 0.8 per cent compared with expectations of 0.3 per cent. Higher inflation could delay market-friendly interest-rate cuts, as lower rates would likely push inflation even higher. Meanwhile, Zscaler missed earnings expectations and CoreWeave issued disappointing guidance. Both fell more than 10 per cent on Friday. For the week and for the month, the S&P 500 and the NASDAQ ended lower.

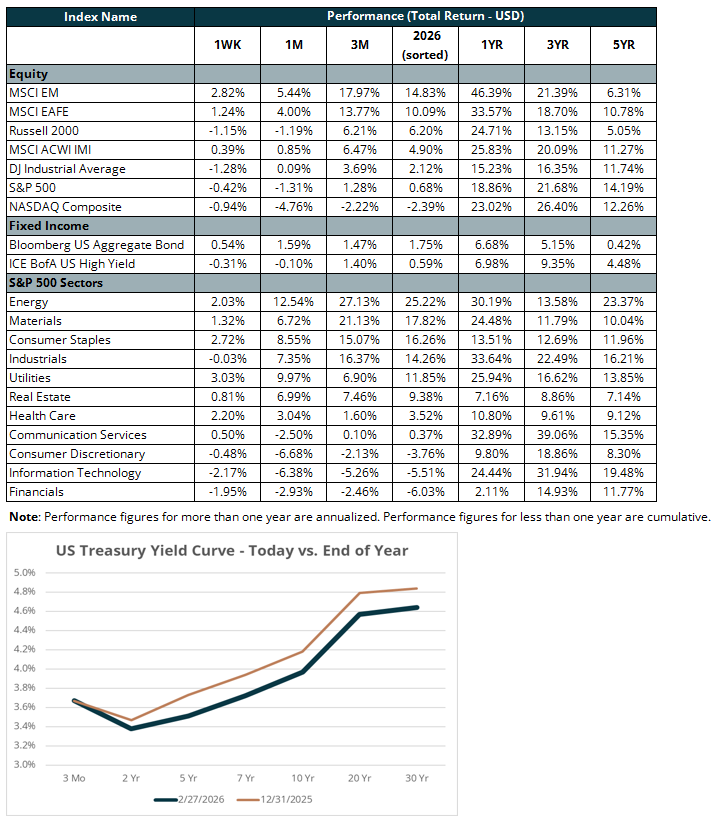

In contrast, the bond market has shown surprising strength. A hotter-than-expected inflation report would typically be seen as a negative for bonds, but growing concerns about employment, corporate earnings, and global conflicts have pushed bond yields lower and prices higher. The 10-year yield broke below four per cent on Friday for the first time this year. And for the year to date through February 28, the benchmark Bloomberg Aggregate Bond Index has returned 1.8 per cent.

Looking ahead, the US-Israel conflict with Iran is likely to push news on earnings and economic indicators to the sideline, at least temporarily. Indeed, this morning (Monday, March 3) oil prices spiked eight per cent, Dow Jones futures dropped more than 500 points, and gold prices moved higher. Global markets also felt the impact, with stocks lower across Asia and Europe. The President has indicated the conflict could take just a few weeks, and deescalation is possible. But until tensions show signs of cooling, developments in the Middle East will likely dominate headlines.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Broader Market Held Firm Despite a Crack in the AI Trade