Market Commentary

AI Disruption Fears Spread to Multiple Industries

by Sequoia Financial Group

by Sequoia Financial Group

All three major stock indices finished in the red last week as AI disruption fears continued to grow. The S&P 500, an index of large US companies, returned -1.3 percent for the week, making the index flat year to date. The Dow Jones Industrial Average, a value-leaning index, returned -1.2 per cent, and the NASDAQ Composite, an index of large cap growth stocks, returned -2.1 percent. Of these indices, only the Dow has generated a positive return so far this year of 3.1 per cent.

Software stocks have plummeted since late January as the market questioned whether Artificial Intelligence (AI) tools would make certain software products obsolete. The concept of “vibe-coding” has entered the lexicon of market pundits. Certain AI tools, including Anthropic’s Claude Code, allow laypeople to build applications that perform tasks similar to those of more expensive software platforms. As a result, the iShares Expanded Tech-Software Sector ETF (ticker: IGV) is down nearly 23 percent this year. Last week, those same fears radiated to multiple other industries, including Media, Real Estate brokers, and Wealth Advisory firms.

LPL Financial (ticker: LPLA) was one of the Wealth Advisory names affected, declining 13.7 percent last week. Goldman Sachs noted that AI fears in the industry were likely overblown. Despite news about new AI features in existing wealth platforms, Goldman believes AI will be additive to wealth advisory, not subtractive. Investors looking through short-term volatility might see a buying opportunity. LPL is still expected to grow earnings 18 percent over the next year, higher than the 14 per cent expected growth of the overall S&P 500. LPLA now trades at 13.7x forward earnings, which is lower than the stock’s 14.4x average over the past 10 years and the current 21.7x for the S&P 500.

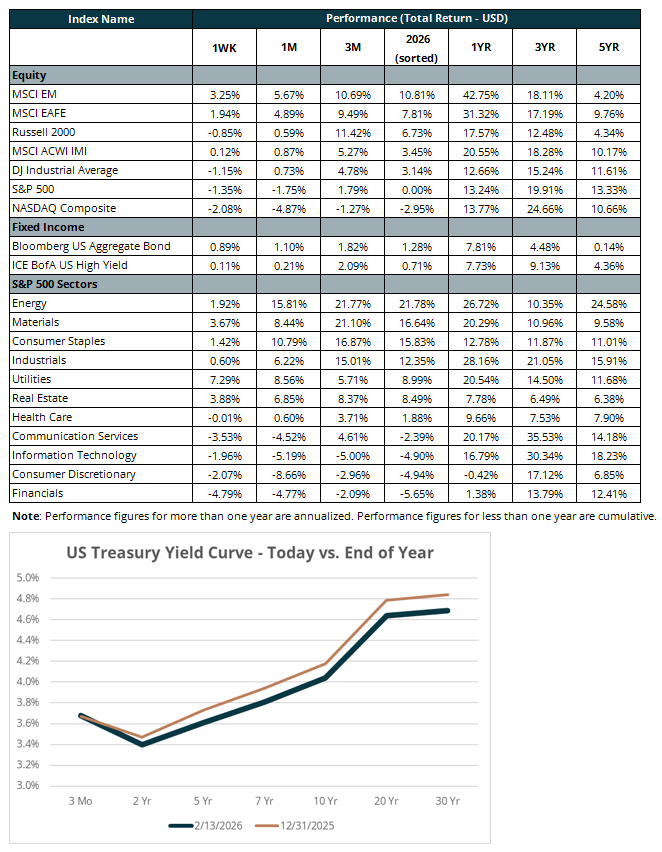

AI disruption fears led to defensive posturing elsewhere. Two notable defensive sectors, Utilities and Consumer Staples, returned 7.3 percent and 1.4 percent, respectively. The divergence in sector performance highlights the importance of diversification, even across asset classes. Public Real Estate Investment Trusts (REITs) and Investment-grade bonds were up, as the yield on 10-year Treasury declined to 4.05 per cent from 4.21 percent. The iShares Core US REIT ETF (ticker: USRT) and the iShares Core US Aggregate Bond ETF (ticker: AGG) were up 3.4 percent and one per cent, respectively.

Friday’s favorable Consumer Price Index (CPI) report strengthened the case for lower interest rates. Core CPI rose 2.5 percent over the 12 months ending January 2026, down from 3.3 percent a year ago. Signs of easing inflation were seen across multiple categories, including Shelter, in which prices increased three per cent year over year – well below last year’s 4.4 percent pace and the 8.2 percent peak in March 2023.

However, the Federal Reserve focuses more closely on the Personal Consumption Expenditures (PCE) index, and the next reading is due this week. Because Shelter carries a heavier weight in the CPI than in the PCE (35 percent vs. 17 percent), cooling CPI inflation may not translate immediately into the Fed’s preferred measure.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory