Market Commentary

Equity Performance Mixed as Market Leadership Shifts Beneath the Surface

by Sequoia Financial Group

by Sequoia Financial Group

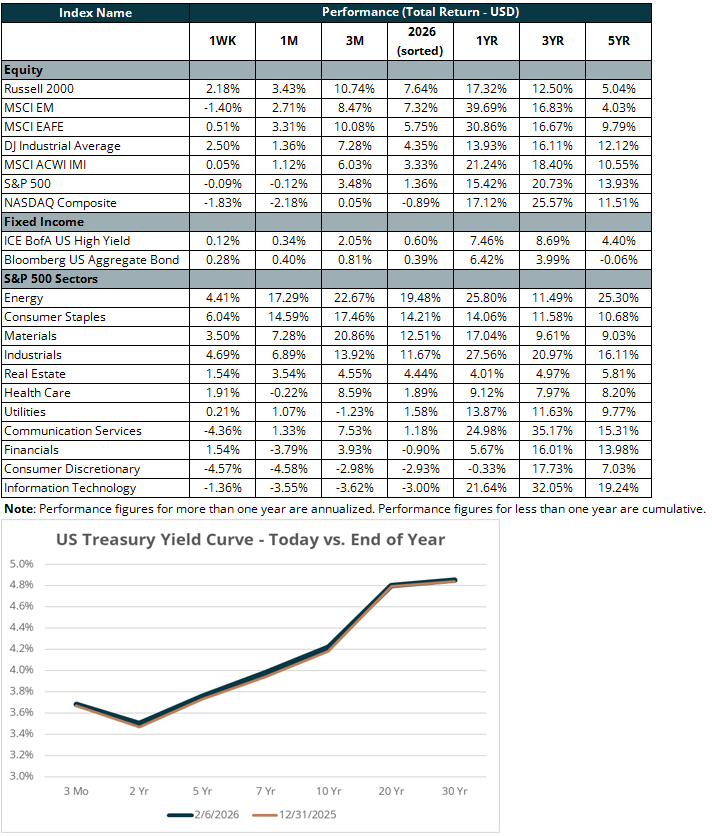

U.S. equity markets delivered mixed performance this week, underscoring elevated dispersion in returns and ongoing shifts in market leadership. The S&P 500 (-0.1%) was roughly flat, while the NASDAQ (-1.8%) underperformed and the Dow Jones Industrial Average (2.5%) and Russell 2000 (2.2%) both posted solid gains. So far in 2026, market leadership has rotated away from large-cap growth stocks toward more cyclical, small-cap, and value segments. Small caps are outperforming their large-cap peers by over six per cent year to date, while value has outperformed growth by nearly 10 per cent. Bitcoin briefly fell below $62,000 as investors rotated out of more speculative segments of the market.

Software was again a notable laggard, with the iShares Software ETF (ticker: IGV) declining 8.7 per cent this week. Software continues to trade poorly (-22% year to date), as fears of AI-related displacement within the sector further dampened investor sentiment. Weakness in software weighed on broader technology performance and contributed to the NASDAQ’s underperformance. The recent dispersion in returns highlights the importance of maintaining a diversified equity portfolio as leadership continues to shift across sectors and styles.

Fourth-quarter earnings season rolled along last week, with notable reports including Alphabet (ticker: GOOG) and Amazon (ticker: AMZN). Results from these large-cap technology companies were generally strong, though investor focus shifted quickly to spending plans for 2026. Both firms delivered operating results supported by continued strength in cloud demand and AI-related workloads. However, management commentary around elevated capital expenditures sparked market concerns, as both Amazon and Alphabet guided to significantly higher capex levels for 2026. While near-term fundamentals remain solid, concerns around free cash flow and returns on incremental investment tempered the market’s response. AMZN and GOOG ended the week down 12.1 per cent and 4.5 per cent, respectively. More broadly, fourth-quarter earnings season has been constructive at the index level. According to FactSet, the S&P 500 currently has a blended earnings growth rate of 12.9 per cent, notably higher than the 8 per cent growth expected at the start of the year. The blended earnings growth rate combines actual results with consensus estimates for firms that have yet to report.

Labor market data remained a focus during the week as investors continued to monitor signs of cooling. Initial jobless claims were above expectations, and Challenger, Gray & Christmas reported an elevated level of announced layoffs in January. ADP’s January employment report showed that private companies added 22,000 jobs during the month, well below expectations for 45,000, pointing to continued tepid private sector hiring. With recent labor data coming in weaker than expected, market participants will continue to monitor incoming indicators closely for signs of additional downside risk.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory