Market Commentary

Markets End Volatile Week Higher

by Sequoia Financial Group

by Sequoia Financial Group

Wall Street finished higher last week as investors weighed President Donald Trump’s latest comments on China and stronger-than-expected results from regional banks, which helped ease midweek concerns about credit risk. Trump acknowledged that a 100 per cent tariff on Chinese imports would be unsustainable but continued to fault Beijing for the breakdown in trade talks after Beijing tightened rare-earth export controls. His remarks came during a volatile week of trading shaped by tariff headlines and uncertainty around smaller lenders, which briefly pushed the Cboe Volatility Index to its highest level since April. By Friday, the S&P 500 had gained 1.7 per cent, the NASDAQ rose 2.1 per cent, and the Dow advanced 1.6 per cent, marking the strongest weekly performance for the S&P since early August as investors took encouragement from renewed signs of dialogue between Washington and Beijing.

Earnings optimism added to the market’s momentum. Major U.S. banks reported results that exceeded expectations, supported by solid investment banking activity and steady credit performance. According to FactSet, financial sector profits are now expected to rise about 18 per cent from a year earlier, more than twice the growth rate of the broader S&P 500. However, credit worries resurfaced midweek after Zions Bancorporation reported a $50 million loan loss and Western Alliance disclosed a fraud-related lawsuit, leading to a 6 per cent decline in the KBW Regional Banking Index. Jefferies also came under pressure due to its exposure to a bankrupt auto lender. Those developments prompted a temporary flight to safe-haven assets before markets stabilized as both regional and large banks recovered, helping U.S. equities close out a volatile yet constructive week.

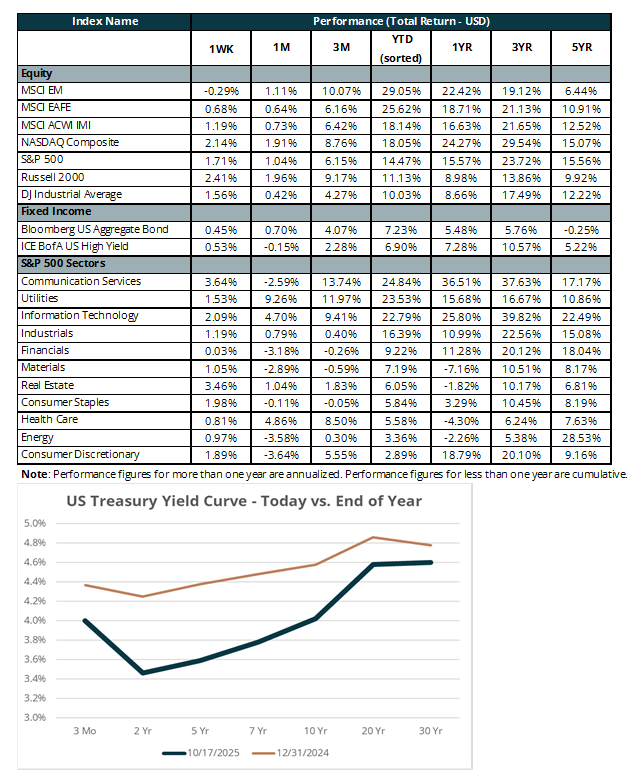

In the bond market, Treasury yields fell sharply on Thursday as investors sought safer assets amid trade tensions and uncertainty caused by the government shutdown. The 10-year Treasury yield briefly dipped below 4 per cent for the first time since April, while the 2-year note touched its lowest level in more than three years. By Friday, yields had steadied, with the 10-year near 4 per cent and the 2-year around 3.46 per cent, as concerns about a broader banking crisis eased following reassuring earnings from regional lenders such as Fifth Third Bancorp. The bond market is now anticipating at least two additional quarter-point Federal Reserve rate cuts by year end, and the yield curve has flattened as investors remain cautious about near-term economic growth and monetary policy.

Gold continued its record-breaking rally, climbing above $4,000/ounce for the first time as investors turned to safe-haven assets amid escalating geopolitical tensions, trade disputes, and financial market volatility. Spot prices in New York reached a record $4,326/ounce on Thursday, while futures briefly climbed as high as $4,392 before easing slightly on Friday. The metal has gained nearly 7 per cent over the past week and about 60 per cent since the start of the year, reflecting strong demand for stability amid the prolonged U.S. government shutdown, renewed tariff threats against China, and rising expectations for lower interest rates.

The federal government shutdown, now entering its second week, has delayed key economic data releases, including the September employment and inflation reports, adding uncertainty to the economic outlook. The Bureau of Labor Statistics plans to release a delayed Consumer Price Index update on October 24. In the meantime, policymakers and investors are relying on private-sector indicators such as the University of Michigan’s Consumer Sentiment Survey, which remains near record lows amid persistent inflation and weakening job prospects. The data blackout comes at a crucial time for the Federal Reserve, which is expected to move forward with another quarter-point rate cut as it balances slowing labor demand with ongoing inflation pressures. Broader uncertainties stemming from tariffs, trade policy shifts, and tighter immigration conditions continue to complicate the outlook, leaving the Fed inclined to maintain flexibility until official data reporting resumes.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

Broken Iran Ceasefire Can’t Hold Back Equities