Market Commentary

Q3 Market Commentary: Revised Realities

by Sequoia Financial Group

by Sequoia Financial Group

Labor Market Revisions, Stubborn Bond Yields, and Earnings Growth Surprises: Three Forces Reshaping Q3 2025 Market Dynamics

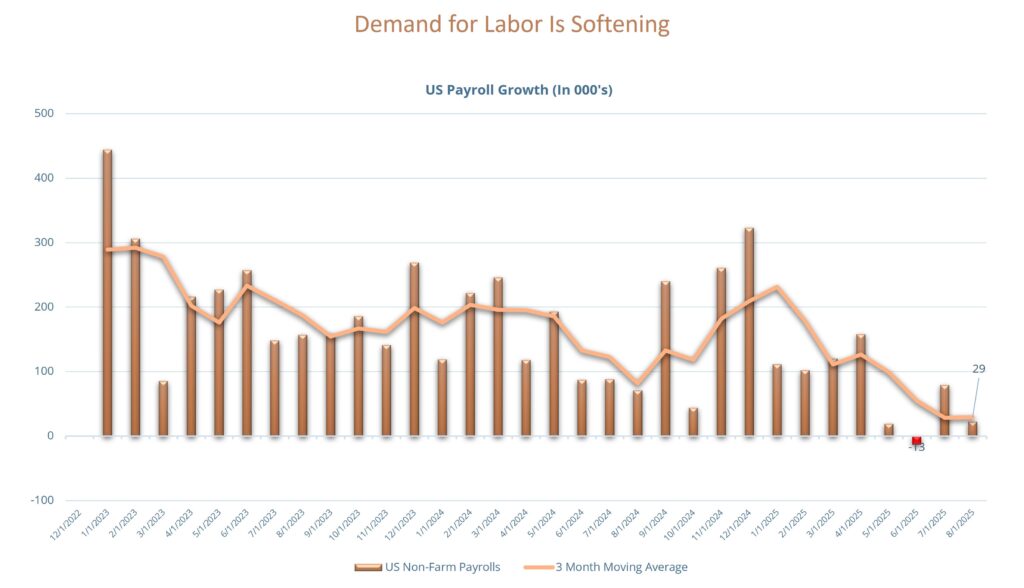

Throughout Q3 2025, ongoing downward revisions to monthly payroll data forced a significant reassessment of labor market conditions. The Bureau of Labor Statistics significantly revised recent monthly payroll gains—June’s initial hiring number fell from a modest increase to an outright net loss upon revision, marking the first negative print since 2020. Across the summer, average monthly job growth plummeted to just 29,000, below the pace needed to sustain steady employment. Even more striking, the annual benchmark revision showed that the U.S. added 911,000 fewer jobs in the twelve months ending March 2025 than previously reported, marking the largest such adjustment in over two decades.

These revisions confirmed a deteriorating picture for the labor market, raising new doubts about the momentum that had

previously underpinned consumer demand and economic resilience. The combination of weak hiring, rising unemployment rates, and reliability issues with headline jobs data prompted calls for immediate rate cuts from the Federal Reserve, as

Source: Bloomberg

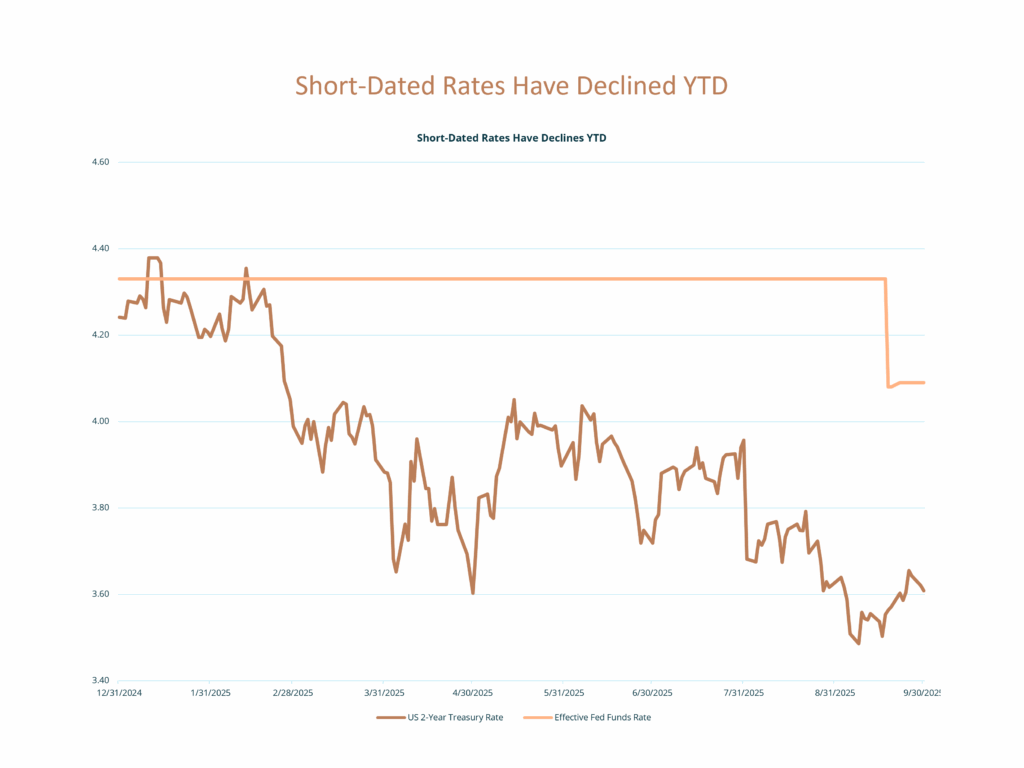

Recent developments in the labor market have meaningfully shifted expectations for Federal Reserve policy. As job growth has slowed and payroll revisions have pointed to softer employment trends over the summer, investors and policymakers alike are reassessing the risks to the economic outlook. In public remarks, several Fed officials have acknowledged that the balance of risks surrounding their dual mandate has become more evenly weighted, with concerns about labor market weakness now taking on greater importance relative to the fight against inflation.

Reflecting these shifting dynamics, interest rate expectations have moved lower. The two-year U.S. Treasury yield, often regarded as a reliable indicator of the expected path of policy rates, has declined significantly in recent weeks. This move illustrates growing conviction in markets that the cycle of restrictive monetary policy is nearing an end, and that Fed rate cuts may come sooner than previously anticipated.

Taken together, these developments underscore a significant shift in the policy and market narrative—from an exclusive focus on inflation risk to a more balanced consideration of growth, employment, and financial stability.

Source: Bloomberg

Policy Rate Cuts May Not Flow to the Long-End

Despite mounting evidence of labor market weakness and rising consensus for lower policy rates, longer-date Treasury yields remained range-bound or even edged higher following major data releases, as investors demanded greater clarity on the Fed’s tolerance for lagging inflation and fiscal risks—particularly in the wake of deficit expansion and heavy Treasury issuance expectations. This stubbornness reflected both lingering concerns about inflation and skepticism that employment revisions alone would drive a rapid return to ultra-loose monetary conditions.

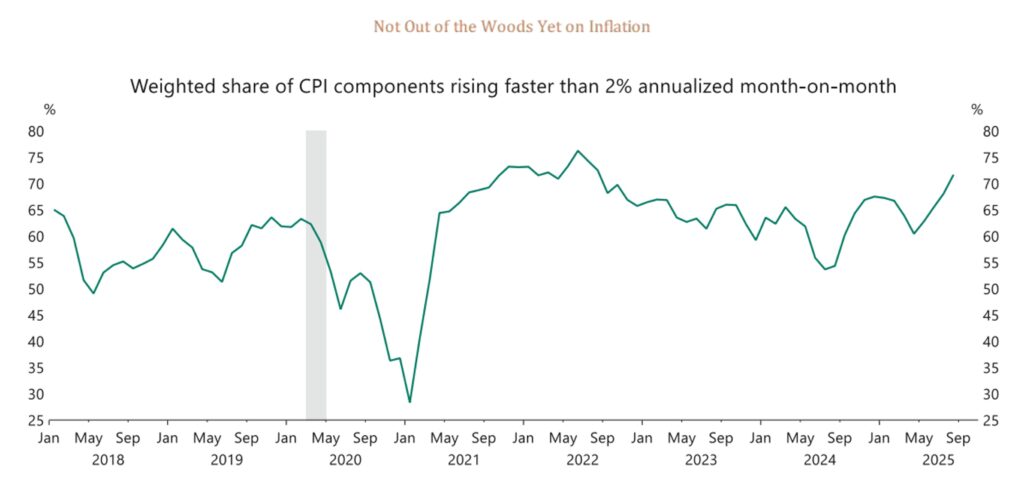

The bond market continues to signal caution, reminding investors that the inflation battle is not yet fully won. That concern may be well-founded. As the chart on the following page illustrates, more than 70% of the components within the Consumer Price Index are still trending above the Federal Reserve’s 2% inflation target. This breadth of underlying price pressures suggests that inflation risks remain embedded across the economy.

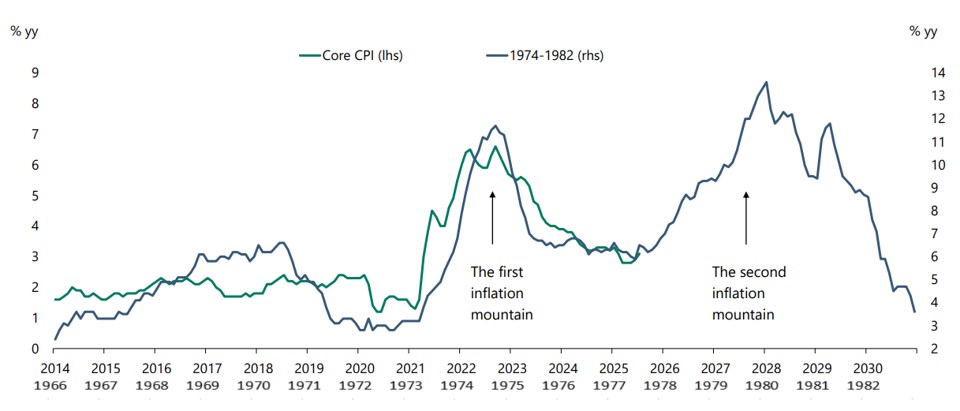

Gold buyers are echoing that message, with demand for the metal reflecting investor skepticism that policymakers can shift toward an accommodative stance without reigniting inflationary pressures. The core risk is that easing policy too soon could trigger a second wave of inflation—an outcome reminiscent of the 1970s, when premature easing prolonged the inflation cycle.

Source: Apollo

Amid an increasingly uncertain backdrop for government debt, demand for corporate bonds remains robust. AAA-rated corporate debt is trading at a spread of just 30 basis points over U.S. Treasuries—a slim premium for taking on additional credit risk. In fact, Microsoft Corporation’s bonds are trading at a negative spread to Treasuries, meaning investors are valuing them as if they carry less risk than U.S. government debt. Are they truly safer? Microsoft holds a coveted AAA rating, while all major credit-rating agencies have downgraded the U.S. The company sits on $95 billion in cash against only $40 billion in long-term debt, and it continues to generate exceptional profits. Perhaps, then, it isn’t so far-fetched. The market seems to agree—investors are voting with their wallets.

Investor sentiment toward the U.S. is highly divided. On one hand, many are optimistic about American corporations—especially large technology firms that are riding the wave of artificial intelligence. On the other hand, a number of foreign investors are skeptical about the broader U.S. outlook, citing concerns such as tariffs, lingering inflation pressures, rising public debt, the government shutdown, and questions over the Federal Reserve’s independence. The optimists are buying, while the skeptics are reducing exposure or shorting the dollar. Currently, overseas investors hold approximately $18.5 trillion in U.S. equities, accounting for around 20% of the market, and $8.5 trillion in Treasuries, which represents approximately 30% of the market.

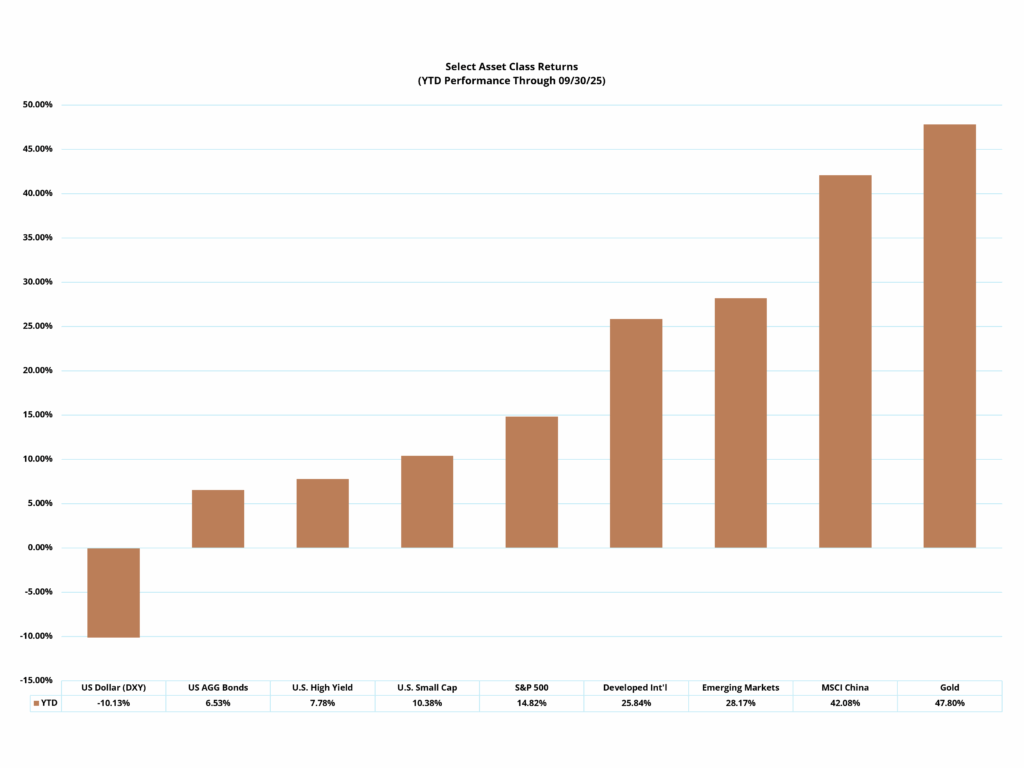

The U.S. dollar and domestic equity markets have been moving in opposite directions this year, creating a more favorable environment for international equities. A weaker dollar has amplified returns for U.S.-based investors in foreign markets, as currency translation boosts gains on overseas assets. This dynamic is particularly evident in year-to-date performance across major asset classes through the first nine months of 2025, where international equity benchmarks have outpaced U.S. counterparts.

At the same time, persistent dollar softness has reinforced demand for real assets such as gold. With the greenback losing ground and concerns lingering over U.S. fiscal sustainability and inflation, investors continue to view gold as both a store of value and a hedge against currency depreciation. Together, these trends highlight how currency movements continue to be a key driver of portfolio outcomes in the current environment.

Source: Bloomberg

Corporate Earnings Growth Underestimated

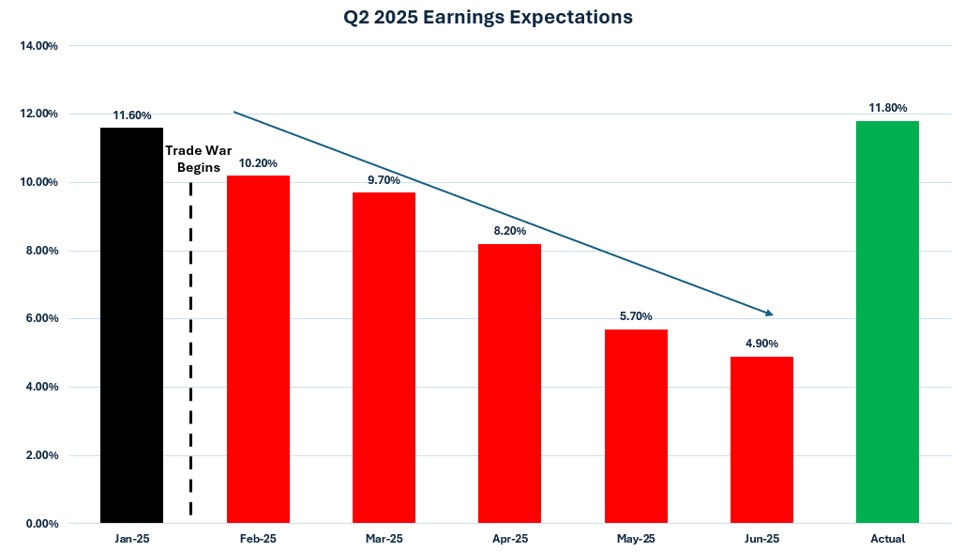

Amid labor market uncertainty, corporate earnings consistently outperformed consensus projections in Q2, providing a powerful counterweight to broader macroeconomic drag. Corporate profits held up better than many anticipated earlier in the year, despite widespread uncertainty. In response to heightened tariff rhetoric, many management teams trimmed or withdrew forward guidance, which drove consensus earnings expectations for Q2 sharply lower. That lowered bar set the stage for what ultimately proved to be a very strong earnings season. The resilience in corporate results supported equity valuations and helped counterbalance concerns from softer labor data, propelling U.S. stock indices to new record highs as investors looked ahead to potential rate cuts.

Source: Bloomberg

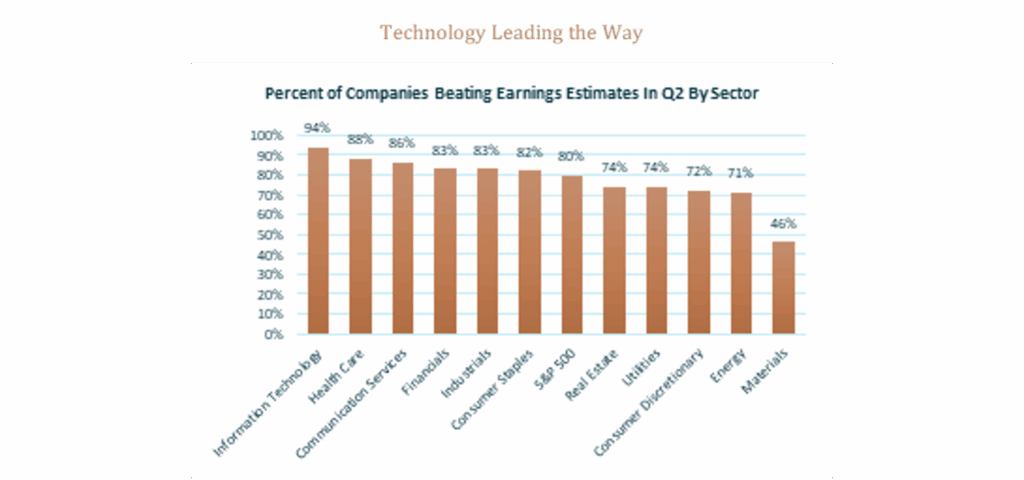

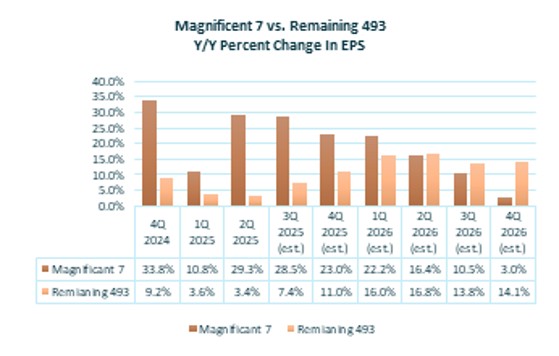

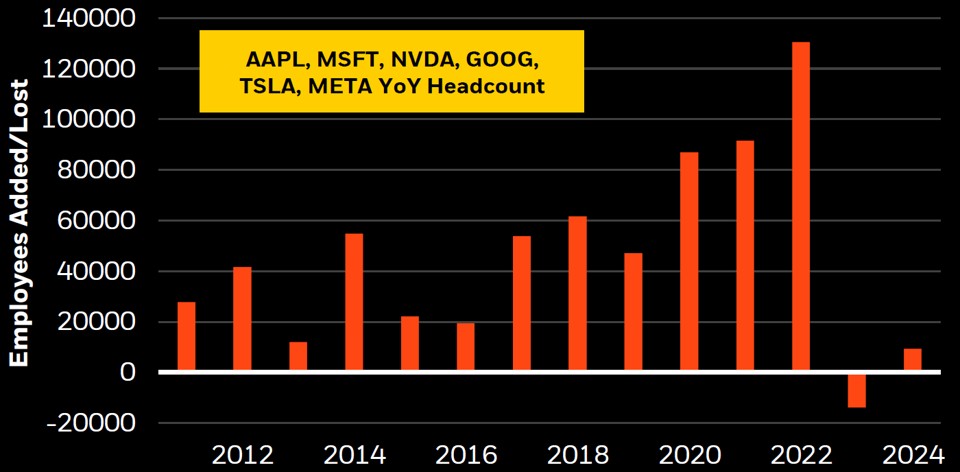

Earnings strength was most pronounced in large-cap growth and technology companies, which remain the primary engine of equity market performance. Q2 results were particularly impressive in the tech sector, where AI-driven spending and elevated capital investment are expected to support future growth. As the chart on the left highlights, 94% of Information Technology companies exceeded earnings expectations in Q2, the highest beat rate of any sector. The “Magnificent 7” stocks continue to account for the bulk of the S&P 500’s earnings growth, delivering nearly 30% earnings-per-share growth in Q2, compared to just 3.4% for the rest of the index (see chart on the right). Encouragingly, expectations suggest earnings growth should begin to broaden across sectors in the quarters ahead—a healthy development for the U.S. equity market.

Source: Bloomberg

AI Adoption Driving Productivity Gains & Economic Air Pockets

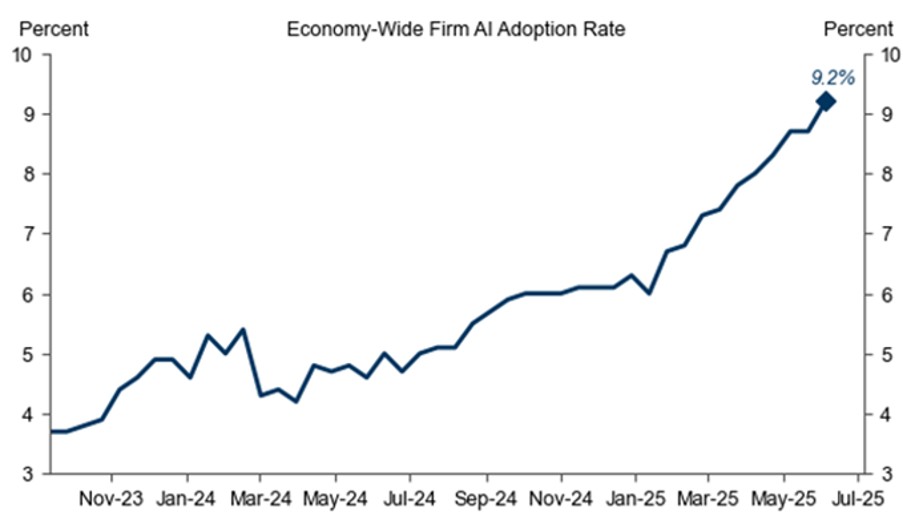

The integration of generative AI and automation into the global economy marks the beginning of what could be one of the most transformative technological revolutions in history. Unlike past cycles where innovation often brought uneven benefits, this wave is emerging as a driver of broad-based productivity gains and cost reduction. As automation and AI scale, they have the potential to expand output while simultaneously helping to contain costs, ultimately contributing to lower, not higher, inflation over the long term. This dynamic underpins our view that lower interest rates may not necessarily reignite inflationary pressures in the current environment. Instead, we expect that the adoption of these technologies will sustain economic growth while steadily improving efficiency.

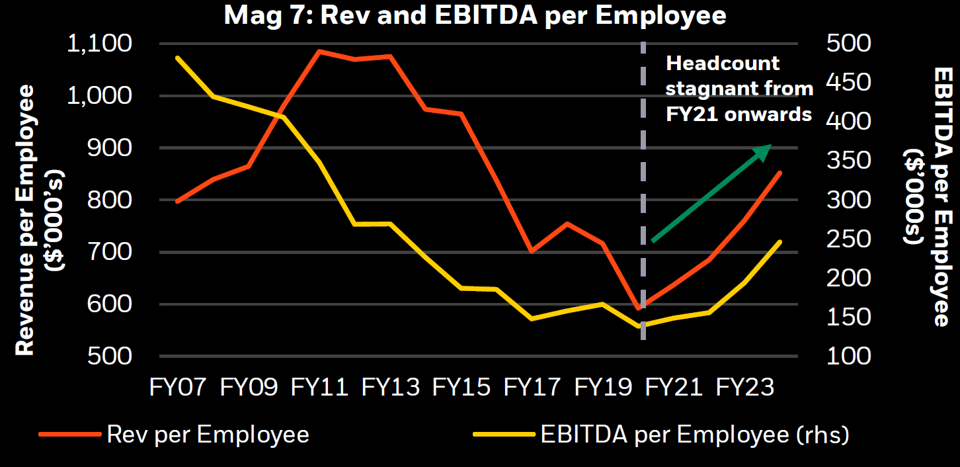

Generative AI is already reshaping industries by enhancing workflows, accelerating decision-making, and enabling firms to achieve more with a stable workforce. Early signs suggest significant improvements in corporate performance driven by efficiency gains rather than workforce expansion. This represents a substantial shift in labor dynamics: while output and productivity rise, private sector hiring is showing signs of slowing as companies prepare for further disruptions. Routine, administrative, and even analytical roles are most vulnerable to automation, yet opportunities remain abundant for those who adapt, reskill, and evolve to work alongside AI. In this sense, AI is not just a technology shift, but a workforce transformation—both a partner and, at times, a disruptor. The charts on the following page illustrate both the pressure on labor demand and the efficiency gains resulting from this transformative technology.

Source: BlackRock

For investors, the implications are particularly compelling. The transition will require significant capital expenditures as companies modernize their infrastructure and integrate new technologies into their operations. These investments, combined with efficiency-driven revenue growth and margin expansion, point to stronger free cash flow generation over time. In short, AI-driven productivity gains, efficiency improvements, and capital investment are aligned with long-term value creation, presenting a powerful and enduring investment theme.

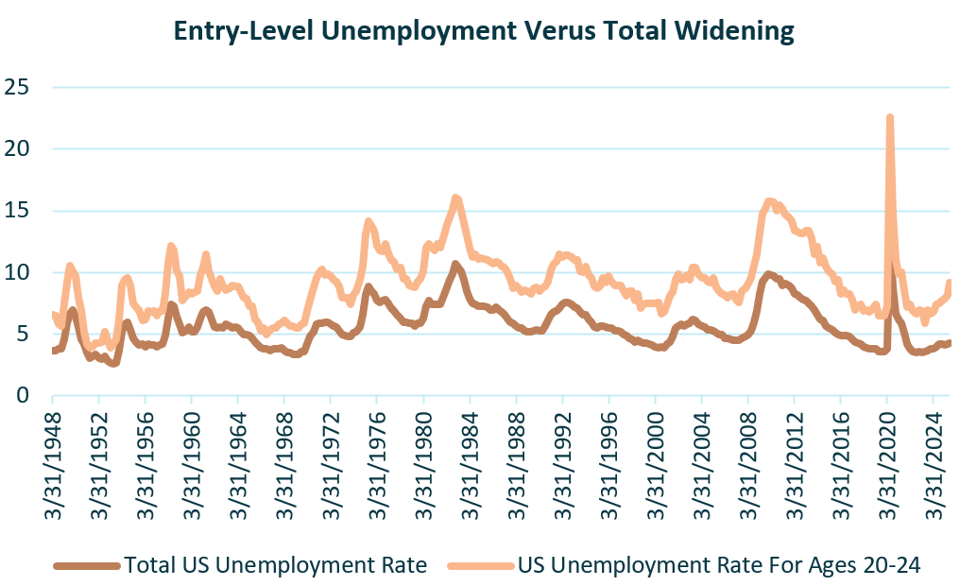

On the other hand, the adoption of artificial intelligence is poised to reshape the entry-level labor market in ways that could be deeply disruptive for new graduates and young workers. Historically, entry-level roles have provided a critical on-ramp for individuals to develop technical and soft skills, build professional networks, and gain experience that propels career growth. As AI tools increasingly automate tasks such as data entry, customer service, administrative support, and even junior-level financial or legal analysis, many of these traditional entry-level jobs risk being reduced, restructured, or eliminated. This acceleration of automation at the lower rungs of the career ladder could leave college graduates facing a more crowded and competitive market, where fewer accessible opportunities exist to gain a foothold.

The challenge for graduates is compounded by the fact that AI not only replaces jobs but also raises the bar for what employers expect, even in entry-level positions. Companies deploying generative AI or advanced process automation often seek candidates who can demonstrate complementary skills, such as critical thinking, adaptability, and the ability to leverage AI as a productivity tool. Without significant retraining and curricular adjustments in higher education, many graduates may find themselves mismatched to the evolving needs of employers. In turn, this can delay career progression, exacerbate underemployment, and widen the gap between those with in-demand, tech-adjacent skills and those whose degrees or experiences no longer map cleanly to the jobs available in an AI-driven economy. According to the graphs on the following page, the unemployment rate for recent college graduates has nearly doubled since the adoption of AI started taking hold in earnest.

Source: Bloomberg

Conclusion

The third quarter of 2025 marked significant shifts in the economy and financial markets. The labor market, long viewed as a pillar of resilience, is now showing signs of softening. Government revisions to earlier payroll data revealed that job growth was much weaker than initially reported, including the first monthly job loss since 2020. With unemployment edging higher and hiring momentum fading, the Federal Reserve has begun signaling a greater focus on supporting growth and employment rather than just fighting inflation. Investors have taken notice, as short-term interest rates have already started to decline in anticipation of potential Federal Reserve rate cuts.

At the same time, bond market dynamics continue to reflect uncertainty. While expectations for Fed easing have brought yields lower on the short end of the curve, longer-term yields remain relatively stubborn. Concerns around persistent inflation pressures, heavy government borrowing, and rising fiscal risks have kept investors cautious. This tension serves as a reminder that the inflation story is not yet behind us, even as labor market weakness raises the likelihood of easier monetary policy in the future.

Balancing these crosscurrents, corporate earnings delivered a positive surprise. Many companies reported stronger profits than expected during the quarter, particularly in the technology sector, where artificial intelligence continues to drive new investment and productivity gains. These results not only helped lift U.S. stock indices to record highs but also reinforced optimism that corporate America is better positioned to withstand slower economic growth than previously thought.

Looking ahead, the rise of AI stands out as both an opportunity and a challenge. While it enables companies to do more with less—boosting efficiency, cutting costs, and sustaining profits—it also reshapes the job market. Routine and entry-level positions are increasingly vulnerable to automation, making it more challenging for recent graduates to establish a foothold in the workforce. For investors, this mix of softer employment data, stubborn bond yields, and resilient earnings underscores an evolving market environment—one where technology adoption and productivity gains provide powerful support for companies even as traditional labor dynamics come under pressure.

As we enter the final quarter of the year, we are thankful for your continued trust as we work closely with you to help you achieve your financial goals and secure your financial future. We want to be the first to wish you happy holidays, and we look forward to talking soon!

All the best,

Your team at Sequoia Financial Group

This material is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Diversification cannot assure profit or guarantee against loss. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. Sequoia Financial Advisors, LLC makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third-parties. Certain assumptions may have been made by these sources in compiling such information, and changes to assumptions may have material impact on the information presented in these materials. Sequoia Financial Advisors, LLC does not provide tax or legal advice. Investment advisory services offered by Sequoia Financial Advisors, LLC., DBA Special Needs Financial Planning. Registration as an investment advisor does not imply a certain level of skill or training.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

2Q26 Strongest Quarter for Stocks Since Pandemic Rebound