Market Commentary

Markets Hit Record Highs but Slide on Inflation

by Sequoia Financial Group

by Sequoia Financial Group

Last Friday, the Bureau of Economic Analysis released its August 2025 Personal Consumption Expenditures (PCE) price index, which showed that core (excluding food and energy) prices rose in line with expectations. Core PCE, the Federal Reserve’s preferred inflation measure, rose 2.9 per cent year-over-year, ahead of the Fed’s two per cent target and a steady uptick from the 2.6 per cent increase in April 2025.

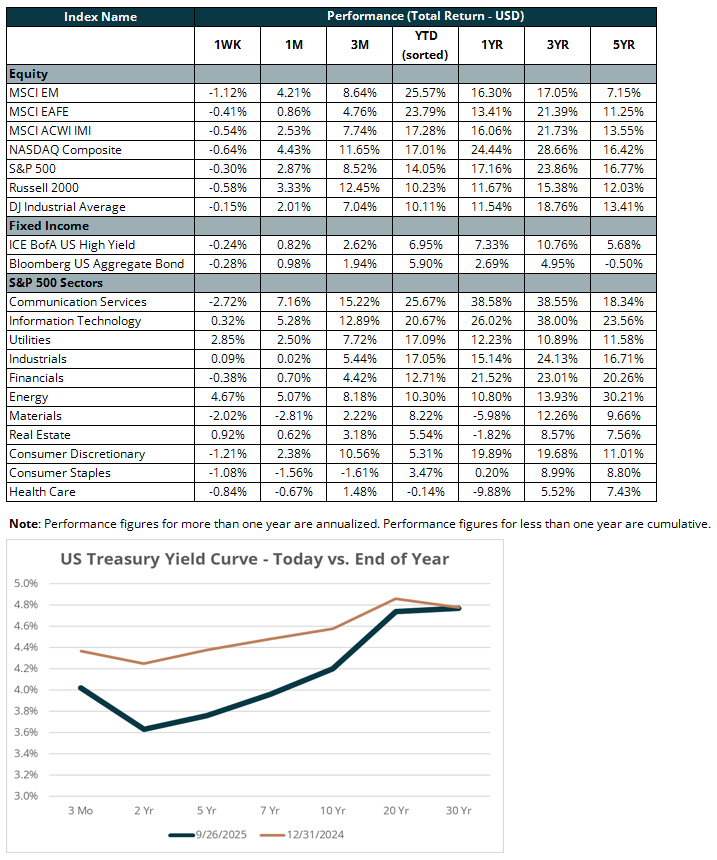

While core inflation was in line with expectations, interest rates rose moderately to end the week. Employment, the other pillar of the Fed’s dual mandate, exhibited strength. Initial weekly jobless claims have fallen by 46,000 in the last two weeks, marking the largest two-week drop in nearly four years. A stronger labor market means the Fed can be more patient in cutting rates. Indeed, the financial markets started pricing in lower rate-cut expectations through the end of 2025. The 10-year US Treasury rate increased 0.06 per cent to end the week at 4.2 per cent. As a result, the duration-sensitive benchmark, Bloomberg US Aggregate Bond Index (“Agg”) returned -0.3 per cent for the week. The 10-year is still lower than it was at the start the year. The Agg has returned +5.9 per cent year to date (YTD).

On Monday, all three major US equity markets closed at all-time highs, but their performance for the week was characterized by that of the S&P 500. The Index declined over the next three days and returned -0.3 per cent for the full week. The S&P 500 has returned +14.1 per cent YTD, owing primarily to Communication Services, Technology, and Industrials sector stocks. During the week, tech giant NVIDIA (ticker: NVDA), announced a $100 billion investment in OpenAI, the owner of ChatGPT. The chipmaker will supply at least 10 gigawatts of computing power for OpenAI to train its next generation of artificial intelligence (AI) models. For context, 10 gigawatts could power the simultaneous electricity consumption of 10 million US households. NVDA shares increased nearly four per cent on the day of the announcement but returned less than one per cent for the week. The stock has returned 32.7 per cent YTD.

The investment raises concerns about the intertwined nature of the AI capex boom. AI hyperscalers (companies that provide virtually unlimited computing, data base and storage capacity) such as Microsoft are spending hundreds of billions of dollars on NVIDIA’s chips to train AI models. Such capex spending can result in unsustainable increases in aggregate profits. When NVIDIA sells its chips, it can recognize 100 per cent of the revenue immediately. When hyperscalers buy chips, they can expense the cost over the chips’ useful lives (multiple years for NVIDIA’s AI chips). If companies do not end up adequately monetizing AI investments, capital expenditures could decline, followed by profits. Microsoft is also a significant investor in OpenAI, previously having committed $13 billion to the company. Despite concerns, NVIDIA’s recent investment shows the AI capex boom might not materially slow any time soon.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Iran Peace Deal Leads Equities Higher