Market Commentary

Fed Cut Boosts Equities to New Records

by Sequoia Financial Group

by Sequoia Financial Group

Last week, the Federal Reserve voted 11 to 1 to lower its benchmark interest rate by 25 basis points, marking its first cut since late 2024. The move was widely anticipated, with futures markets now assigning a 92 per cent probability of two additional quarter-point reductions by year’s end, according to CME FedWatch. Policymakers described the decision as a form of risk management, while stressing that further easing will depend on incoming data, particularly the balance between slowing job growth and persistent inflation pressures.

Equities rallied on the news, led once again by technology and AI-linked stocks. Nvidia’s investment in Intel and continued optimism around AI demand added fuel to the sector’s momentum. By Friday, Wall Street capped off a record-setting week as the S&P 500 gained 0.5 per cent, marking its sixth advance in the past seven weeks, while the Dow rose 172 points (0.4 per cent) and the NASDAQ added 0.7 per cent. All three indices ended at fresh record highs for the second consecutive day, closing at 6,664.36 for the S&P, 46,315.27 for the Dow, and 22,631.48 for the NASDAQ.

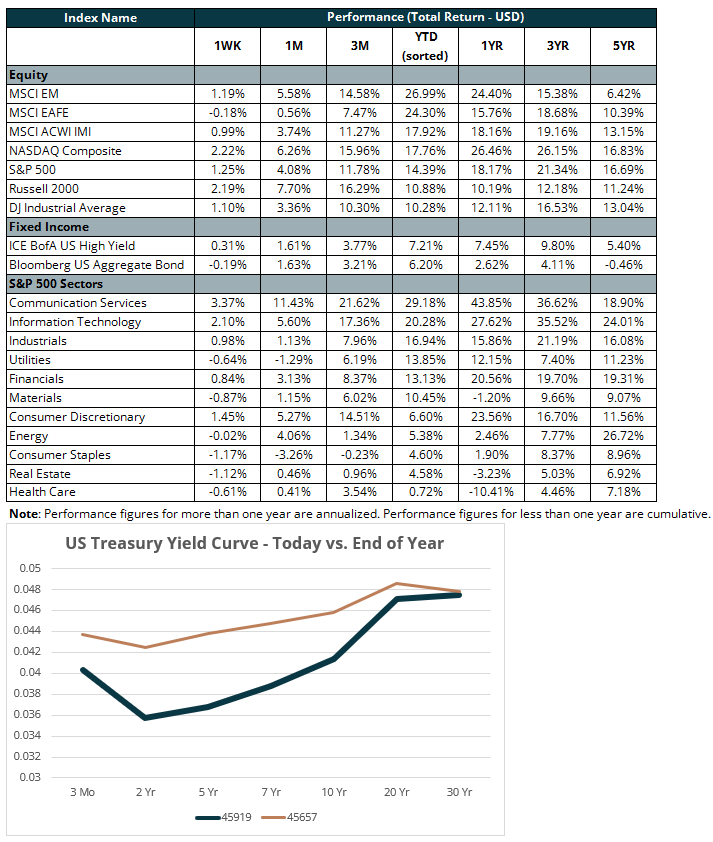

In fixed income, bond yields moved higher despite the Fed’s cut, mainly driven by long-dated maturities. The 10-year Treasury climbed to 4.13 per cent from 4.06 per cent the prior week, while the 30-year yield also advanced. The increases reflect lingering concerns about inflation and heavy government financing needs. Markets remain focused on whether the 10-year continues to rise, as sustained upward pressure could weigh on equities.

Corporate bond issuance was brisk, with more than 15 billion dollars in investment-grade deals priced as issuers moved quickly to capitalize on shifting rate expectations. Across the curve, the two-year yield rose about five basis points, while the 30-year slipped roughly eight, flattening the curve overall. Credit spreads tightened on strong demand, and preferred securities also delivered solid gains.

The Fed’s policy shift has already filtered into the housing market. The average 30-year fixed mortgage rate fell to 6.26 per cent for the week ending September 18, down from 6.35 per cent the week prior, according to Freddie Mac. This marked the fourth consecutive weekly decline, extending a downtrend that began as markets anticipated the Fed’s quarter-point cut. Mortgage rates are now well below their 7.04 per cent peak in January.

Consumer spending also showed resilience. Retail sales rose 0.6 per cent in August, matching July’s upwardly revised increase and far exceeding economists’ forecasts for a 0.2 per cent gain, according to Commerce Department data. The figures suggest households are continuing to spend even as the labor market cools and inflationary pressures linger.

Corporate activity was more cautious. S&P 500 companies repurchased about 235 billion dollars in stock during the second quarter, down 20 percent from the prior quarter’s record 294 billion dollars, according to S&P Dow Jones Indices. Executives pointed to growing uncertainty around tariffs and broader economic policy as reasons for the pullback.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

Broken Iran Ceasefire Can’t Hold Back Equities