Insights, Wealth Planning

The Power of Compound Interest: One of Your Allies in Building Long-Term Wealth

by Sequoia Financial Group

by Sequoia Financial Group

At Sequoia Financial Group, we’re honored to walk alongside individuals and families across the wealth continuum and inspire their loved ones to put compounding interest to work for their goals. In honor of National 401(k) Day on Friday, September 5, please consider sharing this content with an early investor just beginning their savings journey. Because compound interest is most effective over decades of time, it’s especially important to establish a savings discipline that includes compound interest at a young age.

Albert Einstein is often credited with calling compound interest the “eighth wonder of the world.” That might sound like an exaggeration until you understand how it works. Compound interest is the process of earning interest not only on your original investment (principal) but also on the interest you’ve already earned. Over time, this creates a snowball effect that can generate substantial wealth.

SOURCE: Google

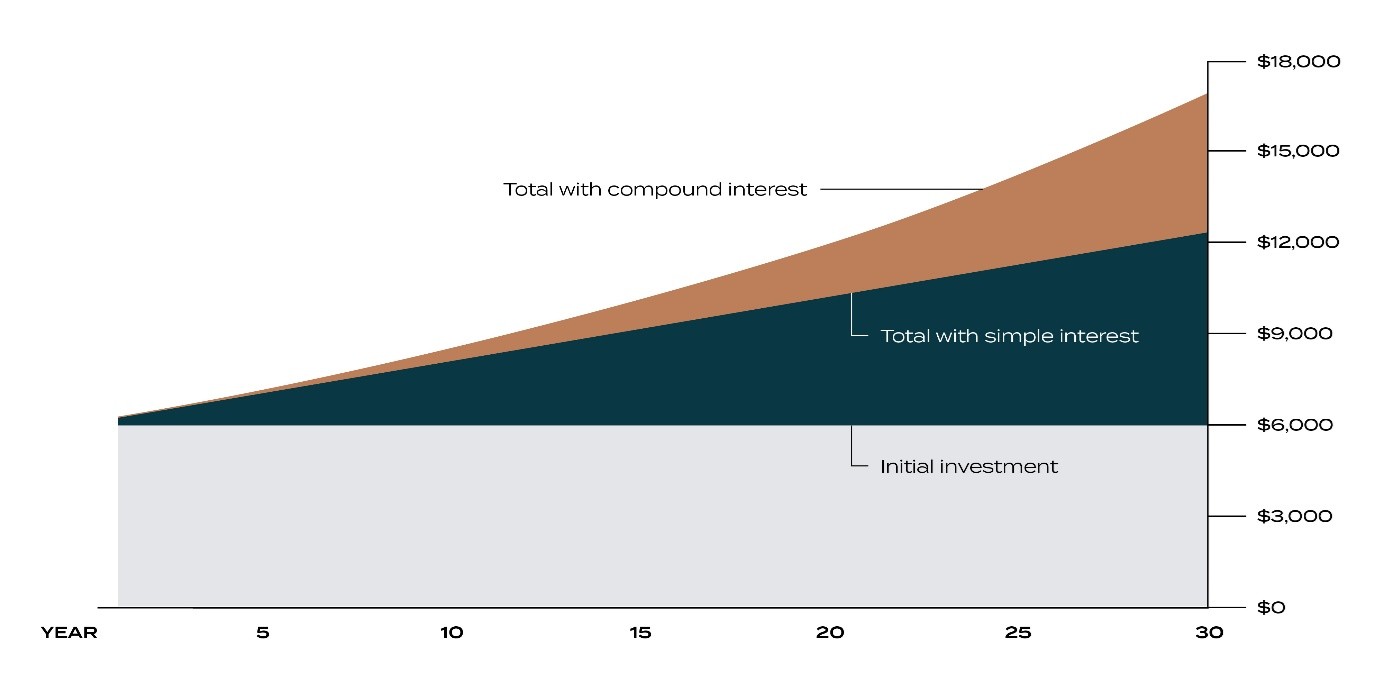

For example, imagine investing $6,000 and leaving it alone for 30 years. With no additional contributions, 3.5% compound interest could grow that sum to roughly $17,000. This is because you’re not just earning money; you’re earning money on the interest you’ve gained over the years.

Why Compound Interest Works Best Over Time

Time is the fuel that powers compound growth. The earlier an investor starts, the more exponential the gains. For example, if you invest $100,000 at a simple 5% interest rate, such as what is found when money is placed in a bank savings account or certificate of deposit (CD), you could earn $50,000 in 10 years. But with 5% compounded monthly, you could earn about $64,700 over the same period.

At first, the growth looks modest as your balance increases by small amounts. However, each new interest payment becomes part of the principal for the next calculation. Over decades, this leads to an accelerating curve, as shown in the chart above. The longer your money stays invested, the faster the growth.

Compound Interest in 401(k) and 403(b) Plans

Retirement accounts like 401(k)s and 403(b)s are built to take advantage of compounding, with two significant boosts: tax deferral and regular contributions.

Here’s how these accounts work:

- You (and possibly your employer) make regular contributions, often every paycheck, providing constant fuel for compounding.

- Your contributions are invested in assets like mutual funds, ETFs, or a mix of stocks and bonds, which generate earnings through interest, dividends, and capital gains.

- Instead of withdrawing those earnings, they stay in your account, where they can earn even more.

- Because the account is tax-advantaged, you don’t lose part of your yearly returns to taxes; 100% of your balance keeps working for you.

The earlier your contributions are made, the more compounding cycles they enjoy. For example, investing $5,000 a year in a 401(k) earning 7% annually can grow to about $472,000 after 30 years, despite you contributing only $150,000. Employer matches, often included in these plans, add “free money” that compounds right alongside your own.

Final Thoughts

Compound interest can be a powerful wealth-building ally when harnessed in your favor. You can turn steady discipline into long-term financial security by starting early, contributing regularly, and taking advantage of tax-advantaged accounts like 401(k)s and 403(b)s.

Investment advisory services offered by Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

This material is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Diversification cannot assure profit or guarantee against loss. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. Sequoia Financial Advisors, LLC makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third-parties. Certain assumptions may have been made by these sources in compiling such information, and changes to assumptions may have material impact on the information presented in these materials.

")

")

Earnings Season off to a Strong Start