Market Commentary

Tame Consumer Inflation Spurs S&P 500 to New Highs

by Sequoia Financial Group

by Sequoia Financial Group

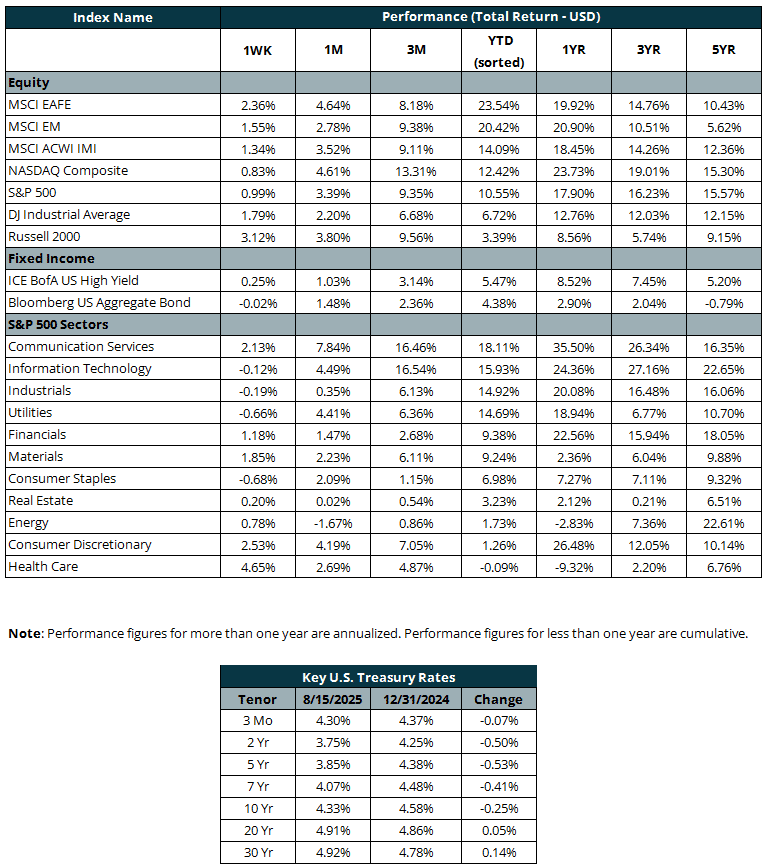

A critical inflation report released on Tuesday showed consumer prices climbed slightly less than expected in July. The consumer price index (CPI) pushed higher by 0.2% for the month and 2.7% for the year. The monthly increase was in line with expectations, but the 12-month increase was slightly better than the expected 2.8% increase, and lower than the 2.9% increase a year ago. The tame report provided support for a Federal Reserve rate cut at its meeting in September, and additional cuts in October and December. Weak job numbers had argued for the Fed to cut rates in an effort to support economic growth, but higher inflation numbers could have pressured it to stand pat, at least for another meeting or two. Stocks cheered the report, with the S&P 500 and NASDAQ both jumping more than 1% to notch new closing record highs.

The rally continued into Wednesday on both the tame inflation report and a largely successful second-quarter earnings season. With 90% of the S&P 500 companies having reported results, 81% reported a positive earnings surprise. The same percentage reported a positive revenue surprise. The quarter also marked the third consecutive quarter of double-digit earnings growth. Overall, the earnings season was seen as a huge success, but companies that posted disappointing numbers were punished for it. One company with a negative earnings surprise saw its stock decrease by 5.5%, more than double the five-year average price decrease for companies reporting negative surprises.

The S&P 500 pushed higher to a third straight record close on Thursday, despite a disappointing wholesale price inflation report. The Producer Price Index (PPI) jumped 0.9% in July, meaningfully higher than the expected 0.2% increase. The odds of a September rate cut held firm, though, sliding just slightly to 93%. The market seemed to look past the higher inflation print, given that much of the gain came from services rather than goods. Analysts also pointed out that the report could suggest businesses are absorbing more of the tariff costs than consumers.

Stocks enjoyed a strong week overall, but bonds didn’t fare as well. The producer price inflation report weighed on bond prices, while Chicago Fed President Austan Goolsbee spoke in an interview Friday about having some hesitation about lowering interest rates. He pointed to lingering concerns over possible tariff-driven inflation and wanting to see more data before the September 16 Fed meeting. He’ll get plenty of data over the next month, with one more look at CPI on September 11.

With earnings season largely in the rear-view mirror, markets will now turn their attention to the economy, with fresh readings due this week on housing and jobs. And to cap off the week, Fed Chairman Powell will speak at the 2025 Economic Policy Symposium, where he’s expected to offer more thoughts on the direction of interest rates and the overall economy.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

")

")

(1)")

Stocks Swing Wildly on Inflation Concerns and Earnings Surprises